http://www.zerohedge.com/news/visualizing-todays-last-second-60000-e-mini-contract-wipe-out

( someone with deep pockets isn't feeling groovy about Wednesday ... )

Submitted by Tyler Durden on 07/31/2012 18:14 -0400

Submitted by Tyler Durden on 07/31/2012 18:14 -0400

and.....

http://www.zerohedge.com/news/fomc-preview-rate-extension-no-new-qe

Submitted by Tyler Durden on 07/31/2012 15:56 -0400

and.....

http://wallstreetexaminer.com/2012/07/27/strong-july-withholding-taxes-suggest-huge-job-gains/

In real terms, the year to year gain in withholding taxes has been between 2.25% and 3.75% over the past two weeks, as

adjusted for the 2.2% increase in average weekly earnings reported in June by the BLS.

( someone with deep pockets isn't feeling groovy about Wednesday ... )

Visualizing Today's Deja Vu Last Second 60,000 E-Mini Contract Wipe Out

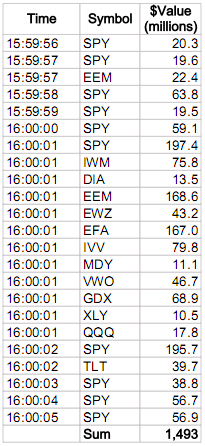

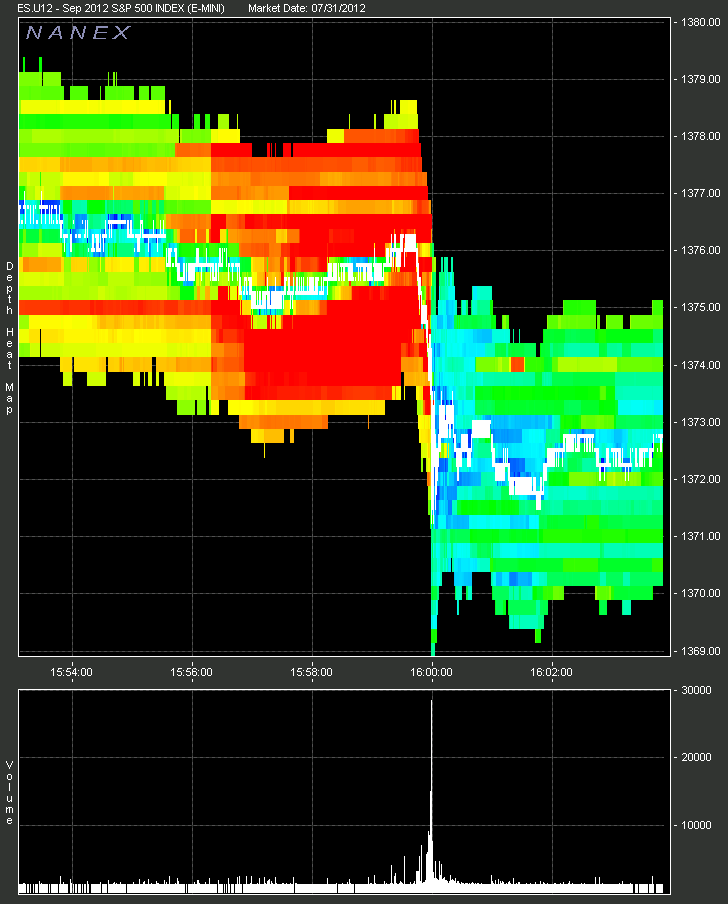

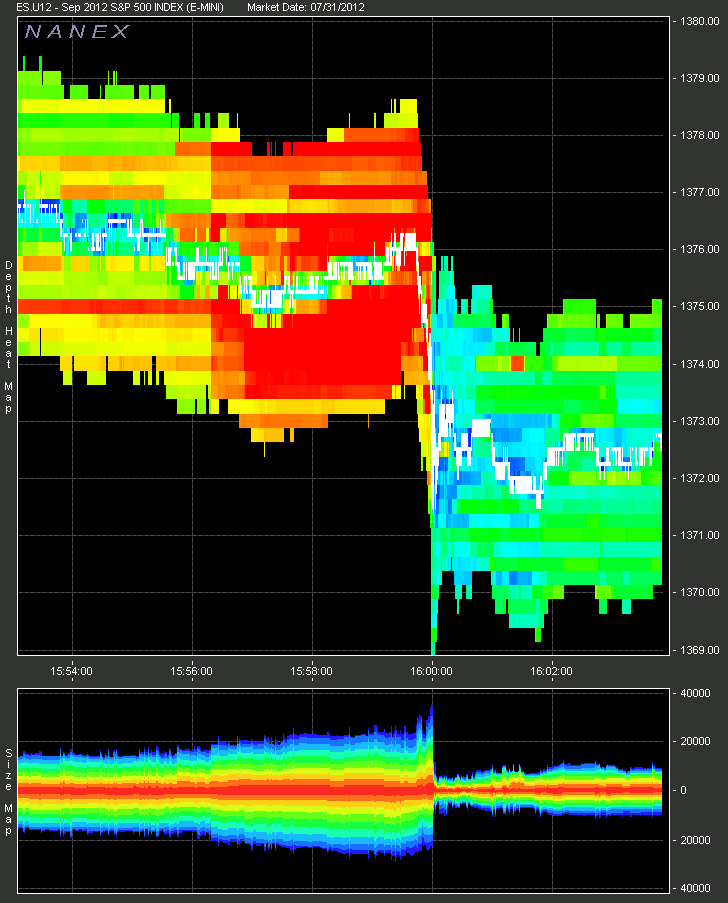

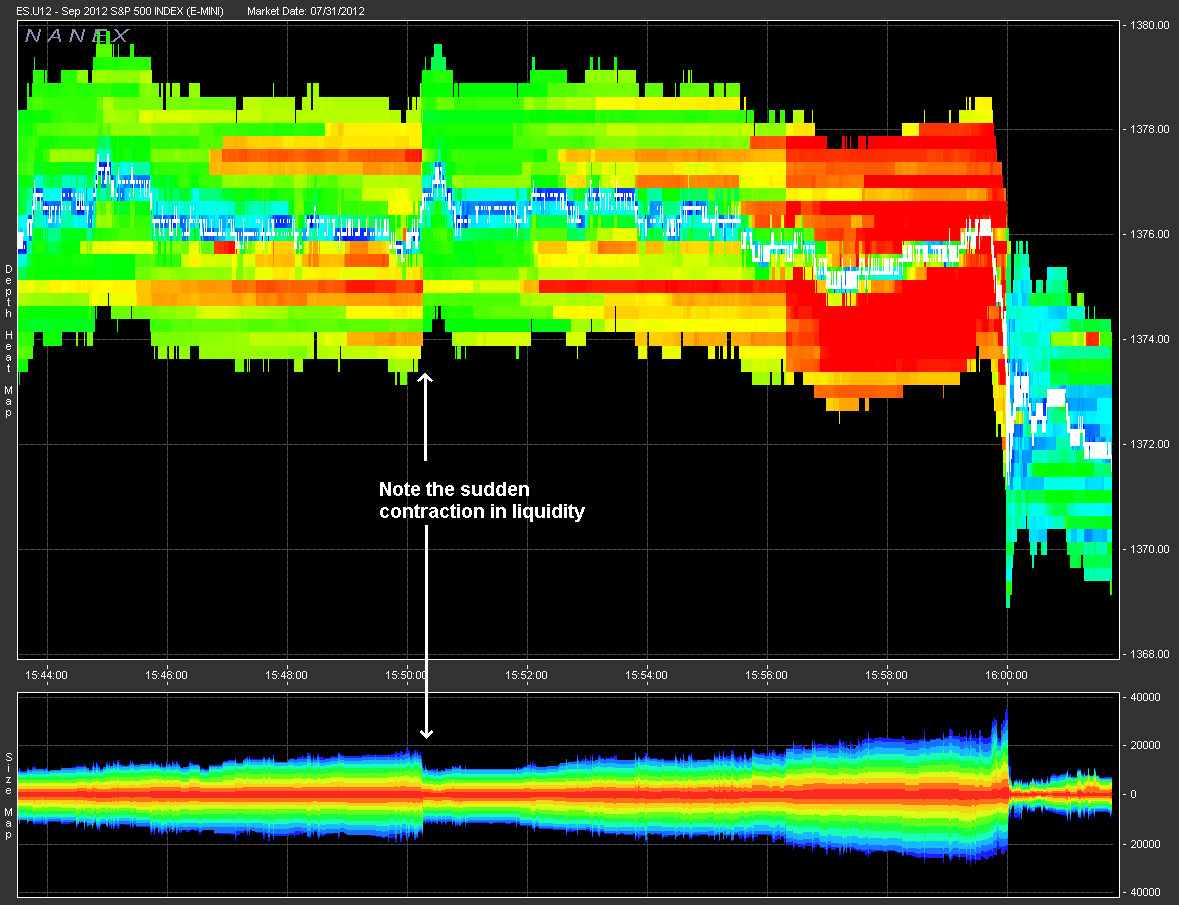

Today, three seconds before the close, someone was in a desperate hurry to dump 60,000 E-Mini contracts - the equivalent of $4.1 billion in underlying notional (ignoring the reflexive impact on various correlated assets and downstream synthetic instruments like ETFs and options). What happened next was a trade that was just shy of the size of the Waddell and Reed trade that the SEC said caused the flash crash. Luckily this time there was just 3 seconds of potential waterfall after-effects before the market closed. Had this happened at the May 6 blue light special time of 2:30 pm, the month end marks of US hedge funds and prop desks would have looked very different one day before the all too critical FOMC statement. The question remains: who waited to perform a reverse E-bay (inverse bid all in, in the last second of trading), and just what do/did they know? Below we present the complete 60,000 dump in its full visual glory courtesy of Nanex. But hold on. There is a twist...

From Nanex: eMini Wipe-out

On July 31, 2012, starting about 3 seconds before the close (15:59:57 EDT), our monitoring software alerted us to an unusually large trade of over 60,000 eMini (ES September 2012) contracts that were sold at once. At the same time, we also received an alert showing large and unusual trades in ETFs (note the last column is the value of the trade in millions of dollars):

|

and.....

http://www.zerohedge.com/news/fomc-preview-rate-extension-no-new-qe

FOMC Preview - Rate Extension But No NEW QE

The Hilsenrath-Haggle Federal Open Market Committee (FOMC) is likely to ease monetary policy at the July 31-August 1 meeting in response to the continued weakness of the economic data and the persistent downside risks from the crisis in Europe. While we expect nothing more exciting than an extension of the current “late 2014” interest rate guidance to "mid-2015", Goldman adds in their preview of the decision that although a new Fed asset purchase program is a possibility in the near term if the data continue to disappoint, their central expectation is for a return to QE in December or early 2013.

Golman Sachs: FOMC Preview

Q: Will the FOMC ease monetary policy?

A: Yes, we expect the Federal Open Market Committee (FOMC) to ease at the upcoming July 31-August 1 meeting. The FOMC decision will be announced at 2:15pm on Wednesday August 1, and there will be no post-statement press conference.

Q: Why?

A: We see three reasons.

- First, the economy has lost further momentum since the June 20 FOMC meeting. Real GDP growth printed at 1.5% (annualized) for the second quarter and the June CAI presently stands at only 1.3%. Information received so far for July (including surveys of regional manufacturing and consumer confidence) has generally remained weak and expectations for the main indicators to be released this week (including payrolls and ISM) are subdued.

- Second, a decision not to ease is tantamount to a tightening. The reason is that the impact of unconventional easing--unlike that of conventional short-term interest rate policy--"decays" over time. We estimate that this "decay" would push up the 10-year Treasury yield by about 30 basis points (bp) between now and the end of 2013 if no further easing is provided. Fed officials have expressed a similar view.

- Third, the FOMC expressed a clear easing bias in the June 20 FOMC statement, noting that "…[t]he Committee is prepared to take further action as appropriate to promote a stronger economic recovery and sustained improvement in labor market conditions in a context of price stability." Fed communication since then has generally reaffirmed openness to additional easing. Although Chairman Bernanke's prepared remarks at the semi-annual Humphrey-Hawkins testimony were noncommittal, he provided a list of easing options during Q&A and said that easing would depend on whether there is "a sustained recovery going on in the labor market or are we stuck in the mud". San Francisco Fed President John Williams, for example, said recently that "the pace of growth has been frustratingly slow" and that Fed officials "stand ready to do what is necessary to attain our goals of maximum employment and price stability." Recent press reports--including pieces by influential journalists at the Financial Times, Wall Street Journal and New York Times --have likewise suggested that additional easing is likely in the near term.

- Q: What are the options?A: Chairman Bernanke described a "logical range" of four monetary easing options at the Humphrey-Hawkins testimony, including 1) another round of asset purchases focused on Treasuries and/or agency mortgage-backed securities, 2) use of the Fed's discount window for lending purposes, 3) changes in communication regarding the likely path of interest rates or the Fed's balance sheet, and 4) a cut in the interest rate on excess reserves (IOER), currently 0.25%.Q: How will they ease this week?A: We expect an extension of the current “exceptionally low…at least through late 2014” interest rate guidance to "mid 2015."Such a shift would roughly restore the forward guidance to the same three-year horizon as at the January FOMC meeting, when the "late 2014" formulation was first adopted. We would, however, regard this rate extension as a relatively modest step. Specifically, our estimates suggest that this might be worth 5-10 basis points on the 10-year Treasury yield and at least some of this appears to be already priced in.Q: Why not do more now?A: We see three reasons.

- First, Bernanke noted at the last press conference that the extension of Operation Twist was a "substantive" easing step (our estimates suggest that it is roughly 3/4 as large as QE2 or the original "twist" in terms of the amount of fixed income duration that will be removed from the private sector) and that unconventional easing steps "by their nature…tend to be lumpy." This would suggest that renewed balance sheet action is more likely at a time when the prior program expires, namely at the end of 2012 rather than now or in September.

- Second, while the economic data suggest that additional easing is warranted, financial conditions send a different message. Our GSFCI has generally eased in recent weeks and now is back to the levels of early April before the most recent bout of Euro area turmoil. As a result, our statistical model of meeting-by-meeting Fed policy says that the probability of an easing step this week is only around one-third. We would not necessarily take the model as a literal guide--as we do expect a small easing step this week--but this does suggest that the recent easing in financial conditions is an argument against expecting a big step this week. (What complicates the use of mechanical models, at least in this case, is that the improvement in financial conditions is clearly due at least in part to the anticipation that the Fed will ease.)

- Third, we continue to expect some improvement in the dataflow towards our forecast of a 2% growth pace in the second half of this year. In addition to the easing in financial conditions, these include the end of temporary drags (including payback for the warm winter and possible seasonal adjustment distortions), continued housing recovery and a pickup in real disposable income growth.

Given these factors we expect Fed officials to announce additional asset purchases at the December meeting or in early 2013. But an earlier return to QE is certainly possible--especially at the September meeting if the data do not improve in line with our expectations.Q: How about the other options?A: We believe that Fed officials are unlikely to make use of the other tools on the Chairman's list any time soon.- First, we judge that the committee views the forward guidance as a better way of mitigating upward pressure on short-term rates than a cut in the IOER because it seems less likely to interfere with money market functioning.

- Second, we believe that a "credit easing" program would be relatively unattractive in practice given that (1) the cost of funding for US banks is already low, so the incentive for banks to increase lending would be reduced; and (2) given political and regulatory scrutiny, banks may be wary of participating in such a program.

and.....

http://wallstreetexaminer.com/2012/07/27/strong-july-withholding-taxes-suggest-huge-job-gains/

Strong July Withholding Taxes Suggest Huge Job Gains

The report is an excerpt from the Employment Charts permanent page, updated when new data is reported. Bookmark it for future reference.

As of July 25, Federal withholding tax collections for the prior 10 business days were 3.2% greater than last year. The 10 day total is extremely volatile however, so for that reason I also look at the 4 week moving average. It is up by 6% year over year in nominal terms. This number must be adjusted for compensation inflation to derive a real rate of change.

This chart compares current withholding tax collections with last year on the same date. It shows this year running well ahead of last year in nominal terms. The gap has been widening all year from zero at the beginning of the year. The April bulge was related to non compensation withholding such as mutual fund withholding for capital gains distributions.

In real terms, the year to year gain in withholding taxes has been between 2.25% and 3.75% over the past two weeks, as

adjusted for the 2.2% increase in average weekly earnings reported in June by the BLS.

Real Federal Withholding Taxes – Click to enlarge

The BLS jobs data is based on payrolls for the week including the 12th day of the month. During that week, the real year to year increase in withholding taxes was 1.5%. To estimate the July headline payrolls number, multiplying July 2011 non farm payrolls of 131.407 million x 101.5% = 133.378 million. That would be an increase of 290,000 jobs versus the June number.

With everyone talking about how weak the economy is, that would be a big positive surprise. Will the number actually come in that strong? Given the vagaries of the jobs surveys, including the fact that the rate of change in weekly average earnings could be substantially different from last month’s 2.2%, it’s doubtful. I suspect a “beat” of some magnitude. The data will be released Friday, August 3.

No comments:

Post a Comment