http://www.guardian.co.uk/business/2012/may/17/eurozone-crisis-cameron-greece-euro-exit

http://www.testosteronepit.com/home/2012/5/16/the-greek-extortion-racket-in-its-final-spasm.html

Photo: Teacher Dude, with permission

Photo: Teacher Dude, with permission

Fitch's downgrade of Greece came as I was digesting two opinion polls from Athens.

The latest MARC/Alpha survey, which was conducted between Tuesday and today, put New Democracy (which broadly supports the terms of Greece's financial programme) back in the lead, closely followed by Syriza (which has vowed to reshape it).

New Democracy: 26.1% of the vote

Syriza: 23.7%

Pasok: 13.2%

New Democracy: 26.1% of the vote

Syriza: 23.7%

Pasok: 13.2%

That, according to Bloomberg, would give New Democracy 123 seats (including the 50-seat bonus for coming first), followed by 66 for Syriza and 41 for Pasok. So the two "mainstream" parties could then form a majority in the 300-seat parliament.

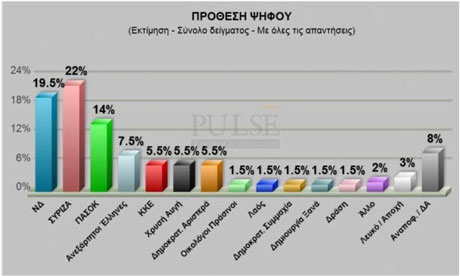

However, a different poll carried out by the Pulse polling group (see bar chart) found that Syriza was the most popular:

Photograph: Pulse

Syriza: 22%

New Democracy: 19.5%,

PASOK: 14%,

KKE Communist Party: 5.5%

Democratic Left: 5.5%

Golden Dawn: 5.5%

New Democracy: 19.5%,

PASOK: 14%,

KKE Communist Party: 5.5%

Democratic Left: 5.5%

Golden Dawn: 5.5%

and....

http://www.testosteronepit.com/home/2012/5/16/the-greek-extortion-racket-in-its-final-spasm.html

WEDNESDAY, MAY 16, 2012 AT 7:31PM

A sad incident got picked up by the German national media, made even sadder by the very fact that it got picked up: in the tourist town Monemvasia at the southern tip of the Peloponnese in Greece, some local guys accosted a 78-year old Dutchman who has lived there since the 1990s. They thought he was German. So he corrected them. “German or Dutch, it’s the same thing,” they told him and broke his jaw and nose.

Two guys in their forties were arrested and charged. Police chiefs visited the victim in the hospital. And German tourists had one more reason not to vacation in Greece—though aggressions occur in all countries, including Germany, often with deadly outcomes. Nevertheless, fears of these kinds of incidents, mediatized strikes and tumults, and images of German Chancellor Angela Merkel as a Hitler figure have coagulated into a toxic mix. And Germans decided to vacation elsewhere. It’s going to be a tough season for the Greek tourism industry, the only industry that actually grew last year.

Photo: Teacher Dude, with permission

The Greek economy has shriveled for four years—in the last two years by nearly 15%. Small businesses cratered, unemployment is spreading like wildfire, and those who still have jobs watch their pay and benefits dwindle. The government, up to the gills in debt, is cut off from the capital markets and defaulted on part of its debt. The country depends on being spoon-fed by the bailout Troika—the ECB, IMF, and European Union. One spoon at a time. With periods of desperation in between.

The Troika has used this process as a carrot and stick, rewarding Greek politicians and bureaucrats for good behavior (promising and implementing reforms) and punishing them for bad behavior (reneging on reforms). And so the bailout fund EFSF transferred €4.2 billion in scheduled aid a few days ago, the first tranche of the second bailout package. But it was €1 billion short—the stick that all political parties should heed.

And the Greek political elite have used this process to extort billions from donor countries. Early November, Giorgios Papandreou, Prime Minister at the time, said a single sentence about a referendum on staying in the Eurozone, and it knocked worldwide financial markets into a vertigo-inducing tailspin. For that debacle, read... Greece’s Extortion Racket Jumps To The Next Level.

In early January, the new Prime Minister Lucas Papademos turned extortion against his own people to get labor unions to agree to Troika-imposed wage cuts. “Without an agreement with the troika and the ensuing funding, Greece faces the threat of a disorderly default in March.” Read.... Greece’s Extortion Racket Maxed Out.

“Disorderly default” has been the ultimate threat ever since. President Karolos Papoulias added to the pressure by announcing that the new out-of-money-date would be June 10. And now comes the charismatic 37-year-old Alexis Tsipras, leader of the left-wing SYRIZA, which, according to the latest poll, has surged to number one in the June 17 elections. Under him, Greece would stay in the Eurozone, he promised, but without adhering to the reforms. He wants the Troika to open the money spigot without conditions. Let the good times roll—at the expense of taxpayers elsewhere. And he ratcheted up the extortion racket one more notch when he proclaimed, “If the disease of austerity destroys Greece, it will spread to the rest of Europe.”

In a broad counterattack, top officials from across Europe have started to openly discuss Greece’s exit from the Eurozone, sometimes in an encouraging manner. There was EU Commission President Jose Manuel Barroso with the dual message that “we” wanted Greece to remain in the Eurozone, “but the ultimate resolve” to do so would have to come “from Greece itself.” A number of ECB council members have also voiced that possibility, including President Mario Draghi. IMF Managing Director Christine Lagarde suggested that the other option for Greece, if it didn’t honor the budgetary commitments, would be its “orderly exit.” And today, German Banking Association President Andreas Schmitz jumped into the fray, wondering “if the country with its own currency, supported by a sort of ‘Marshall Plan’ from the European Union, wouldn’t be better able to solve its problems.”

And the noose tightened. About €800 million had been yanked out of Greek banks in a single day, caused by “great fear that could develop into panic,” President Karolos Papoulias warned political leaders. More than €5 billion had apparently evaporated since May 6. And the ECB, which is supposed to conduct refinancing operations only with solvent banks, cut off Greek banks from Emergency Liquidity Assistance because they haven’t been recapitalized after the haircut of Greek bonds on their books had wiped out all traces of equity capital.

There isn’t much room for optimism. Pushed into a dead-end like this, a country would normally print money to fund its deficits, and it would devalue its currency to become more competitive, however much pain that would spread around. But Greece can’t “solve” its problems that way. Not yet. And its caretaker government is helpless. So words fly about wildly from all directions to influence the Greek people who’ll get another whack at deciding their future on June 17. But the Greek people have been driven to the limit. Read.... The Endgame: “Greeks feel hopeless”

and....

http://www.guardian.co.uk/world/2012/may/17/austerity-will-send-greece-to-hell-alexis-tsipras

Austerity will send Greece to hell, warns Alexis Tsipras

Syriza leader's claims countered by Antonis Samaras, who says Greek government must not abandon reforms or quit euro

Alexis Tsipras, the leader of Syriza, continues to reject the Greek government's EU-mandated austerity deal. Photograph: Martin Godwin for the Guardian

The two main figures in what promises to be Greece's most electric election in living memory were on a collision course on Thursday, with one predicting "hell" if Athens adheres to EU-mandated austerity and the other forecasting a "nightmare" if the nation abandons reforms and gives up the euro.

Emboldened by yet another poll showing his party's wide appeal, the leftwing Syriza leader, Alexis Tsipras, said the international accord that Greece had signed up to in return for rescue loans was catastrophic for the country. Instead of a rescue, the debt-stricken nation has been thrown into its worst recession since the second world war.

"With this policy [bailout agreement] we are going directly to hell," he told CNN. "To save Europe we need to change direction," insisted the politician who has pledged to "tear up" the €130bn (£104bn) "memorandum of understanding" that Athens reached with the EU and IMF earlier this year.

The 38-year-old, who has sent shockwaves through EU capitals with his fiery anti-austerity rhetoric, made the remarks as Syriza announced that he would be visiting Berlin and Paris next week for talks. It was unclear whom Tsipras would be meeting, although aides said the German chancellor, Angela Merkel, would not be among those lined up.

Within hours, the leading credit agency Fitch had downgraded Greece's sovereign rating to CCC from B-, citing "the risk of a Greek exit fromEuropean Monetary Union … in the near term".

Earlier in the day, Antonis Samaras, who heads the conservative New Democracy party, painted a very different picture in a speech that conjured images of a living hell if Athens quit the EU.

In the event of the debt-stricken country reneging on the pledges it had made, the road ahead would be a "nightmarish" one, he said.

Reversion to the drachma would mean wages, deposits and property values all being "cut in half", and the price of imported commodities, such as food and fuel, skyrocketing, he predicted. "This is the nightmare that those who speak of a unilateral condemnation [of the loan agreement] will bring," he told his parliamentary group at its last meeting before the 300-seat house is dissolved and the election campaign officially announced .

"The battle that begins the day after tomorrow for the new elections is not about any single party or its electoral influence," said the 61-year-old politician, ashen-faced as he delivered the speech. "It's about whether Greece will remain in Europe, a Europe which is itself changing. Or if Greece will be found to leave Europe, losing much and risking even more."

New Democracy, he said, would form the core of the "front of resistance against catastrophe".

After handing over to his successor, Panagiotis Pikramenos, a high court judge whose caretaker government will lead Greece to elections on 17 June, the outgoing prime minister, Lucas Papademos, also stepped into the fray.

The former central banker, who headed an emergency left-right "salvation government" that secured the EU-IMF sponsored deal, said he feared that sacrifices Greeks had made in the form of tax increases and pay and pension cuts would be lost if voters decided to back anti-austerity parties at the ballot box next month.

Greeks had endured the punitive cutbacks to put the economy back on track through fiscal consolidation, he said.

"The Greek people's sacrifices were not an 'empty shirt'," said Papademos in an open letter to the nation, his last act before leaving office.

"Unilaterally renouncing the country's loan agreement would be disastrous for Greece, as it would inevitably lead the country out of the euro, and possibly out of the European Union," he wrote. "There are those who are waiting to benefit from the chaos that will follow the humbling exit of the country from the common currency."

Next month's poll follows an inconclusive election on 6 May which ushered in the rise of "anti-bailout" groups such as Syriza – the vote's surprise runner-up – and decimated "pro-bailout" parties such as New Democracy and the socialist Pasok.

Speaking to the Guardian, senior Syriza officials insisted that the party, which polls suggest is poised to emerge as the biggest political force, had "no intention" of unilaterally revoking the accord.

"Austerity is over in this country and it's the end of the memorandum of understanding," said Takis Pavlopoulos, one of Tsipras's top aides, referring to the accord. "You have to be a neo-liberal fanatic not to see that it [austerity] has failed," he added, pointing out the record levels of unemployment and deepening poverty engulfing Greece. "But we will not proceed with any unilateral action that might question Greece's membership of the eurozone."

Greece, he said, had been among the original member states to sign up to the then EEC. As such, Athens was also a "co-owner" of the project and could not be ejected from a union it had participated in for over 30 years.

"Destructive austerity was not part of the deal for any member state to enter the eurozone. No one has the right to say 'either you accept austerity or leave'," added the US-trained economist.

Policymakers have claimed that renouncing the loan agreement will lead not only to a disorderly default – with ensuing chaos taking hold of a country whose economy is already on its knees – but possibly to the breakup of the 17-nation bloc.

Syriza argues that such claims are a high-stakes bluff aimed at safeguarding the status quo. Euro–exit fears were not reverberating around the corridors of the European parliament, insisted Nikolaos Chountis, the party's sole Euro-MP.

"There are other voices that you hear that are very ambivalent about the policies being pursued in the name of resolving this crisis," the MEP said. "And there are other countries that are in a very difficult position like Portugal and Ireland. All this scaremongering that is peddled here about Greece facing a living hell just doesn't exist in Brussels."

Fears that Greece would not have enough money to even pay public sector pay and pensions in the event of loans drying up were simply not true, said Panaghiotis Lafazanis, another Syriza MP. "The loans basically cover interest payments," he said.

"They [the Europeans] can't kick us out. The memorandum is not part of the eurozone institutional framework. It is a political choice that has been delegitimised by popular vote."

and....

http://ransquawk.com/headlines/223435

Greek SYRIZA party leader Tsipras says ready to stop debt payments if Europe cuts financing

- says Greece should remain part of Euro-zone

- says Euro-zone faces break-up if Greece fails

- says Euro-zone faces break-up if Greece fails

and....

ATEbank sued over party loans

Yiannis Siatras, who is representing an association called Greek Taxpayers, refers in his suit to press reports about loans by ATEbank to the two parties. Up to 2010, ATEbank is alleged to have lent PASOK 98 million euros of the 114 million total that the Socialists borrowed from banks. The bank, formerly known as Agricultural Bank of Greece, is also reported to have lent New Democracy 105 million euros of the 120 million borrowed by the conservatives. ATEbank reported losses of 481 million euros in 2009 and 395 million in 2010, while it is expected to declare a loss of more than 2 billion for last year. In his suit, Siatras adds that share capital increases to cover these losses led to the state paying almost 2 billion euros. ATEbank was also given 3.2 billion euros in government guarantees between 2009 and 2011.

and....

|

No comments:

Post a Comment