USDJPY Takes Out Stops, Plunges Under 101: Drags Stocks To New Lows

It's just getting worse for global interconnected, correlated markets where every expression of risk is the USDJPY, and of course for the Nikkei and for Japan's PM Abe, who is now on strictImodium watch. Should the USDJPY tumble to double digit range, we are officially in "global central banker intervention is imminent" territory. And yes, for those asking, there isnothing quite as efficient as the "fair value" of stocks being determined by currency stop losses at even, round numbers.

Monday, February 03, 2014 11:25 AM

Loan Rates in Argentina Reach 65% Annually; Is 65% a Good Rate?

Emerging markets continue to crumble, and the spillover on major economies is obvious. Problems always start somewhere, usually at the periphery.

Via translation from Lanacion, please consider Credit Is More Expensive.

Via translation from Lanacion, please consider Credit Is More Expensive.

Following the peso devaluation and sharp hike in interest rates by the central bank, interest rates on loans increased as much as 11 percentage points.Is 65% a Good Rate?

For a personal loan, private banks now charging at least 44% per year. Factoring in fees and other administrative expenses (up to 11 percentage points), the total financial cost exceeds 65% annually.

Public banks have with nominal rates for personal loans in pesos that range from 32% to 44%, with a total financial cost up to 55% annually.

Banks also shortened their terms and revised installments on credit cards

If Argentina is in the midst of full-blown hyperinflation, then any loan rate is a good rate, because the peso will soon become worthless.

If banks believe that is likely, they may publish rates, but credit will completely dry up.

Mike "Mish" Shedlock

Latin American Currencies Plunge To 2003 Lows, Argentine BONARs Shrink

With today's plunge, Latin American currencies have collapsed by over 5% in th elast 2 weeks - the fastest drop in almost two years. Year-over-year this is a 15.75% drop, the largest such drop since Lehman. This drop breaks the 2009 lows and presses the currencies to theirweakest since 2003... Bond markets are being crushed as short-dated Argentine BONARs have collapsed to 14 month lows.

LatAm FX at 11 year lows...

Argentina BONAR have seen firmer days.

Chart: Bloomberg

30Y Treasury Yield Tumbles To 7-Month Lows As Nasdaq Loses 4,000

US equities are pressing fresh lows of the day as USDJPY tests 101. The Nasdaq just broke 4,000 - its worst drop in 8 months; The Dow trading back under its 200DMA; and now every major index is in negative territory from the December Taper. Most notably though, Treasury yields are tumbling as weak data and safe-haven flows have pressed 30-year yields to their lowest sicen July 5th 2013. VIX is trading 20.7% - its highest in 4 months.

All major indices now red from the December Taper...

As Nasdaq loses 4000 and drops by the most since June..

as Bond yields collapse to 7 month lows...

Charts: Bloomberg

Bonus Chart - WTF in financials...

Welcome Janet: Worst February Start For Stocks In 32 Years

The Nasdaq plunged by the most in over 8 months today and broke all the way back to unchanged from the December taper decision of the Fed. All major US equity indices are now negative from the time the Fed decided to slow its flow of free money. The Dow closed below its 200DMA for the first time since December 2012. The S&P 500 closed the furthest below its 100DMA since QE3 started.USDJPY was in charge and everything was higher or lower beta off of that as it broke 102 early then 101 later in the day (with the Nikkei -700 points from the day's highs). Treasuries rallied around 5bps to fresh 7-month low yields for 30Y. Gold and Silver surged, adding 1% on the day as the USD lost 0.25% on the day (led by the 1% strength in the JPY). VIX smashed to 14 month highs over 21%. Credit deteriorated but stocks are catching down.

Just 8 hours into her reign, QEeen Janet has some work to do...

"Not off the lows"

Summing up the JPY carry trade unwind... (h/t @StalingradandPoor)

This is the worst start to a month since 1982 for the Dow and S&P and the worst since records started on the Nasdaq.

The Dow Industrials slammed back under the 200DMA - lowest in over 3 months; down 3% since the taper and down over 7% in 2014

The Nasdaq is down 2.6% - its biggest drop in 8 months - its worst start to a month on record; testing the 100DMA and unchanged to Taper

The S&P dropped 2.2% - its biggest drop since June; lowest in over 3 months and well below its 100DMA - furthest below its 100DMA sicne Nov 2012.

Since the taper, major indices are all negative now...

And since the new year, they are in trouble...

USDJPY was in charge...

VIX has risen 64% on the last 2 weeks - its fastest rise since the US debt downgrade debacle in summer 2011...and the highest close since December 2012

It seems, once again, that credit investors smelled something long before the exuberant marginal stock buyer...

The USD weakened led by JPY and EUR strength...

Treasuries were well bid all day after the weak ISM data... 2s10s pushed to 228bps - its lowest in over 3 months

And commodities were very mixed with growthy oil and copper down and safe haven gold and silver up...

Charts: Bloomberg

Bonus Chart: The Nikkei is down 2300 points year to date (from 16,450 to 14,160) and the Dow is down over 1200 points year-to-date (from 16,540 at the close of 2013 to 15,316 lows today)

Bonus Bonus Chart: HerbaLOL...

Japanese Stocks Tumble - Down 10% In 2014 Following Record Low China Services PMI

USDJPY opened the evening under 102 with JPY holding its losses until around 1700ET when it broke back above the crucial level. S&P futures and USDJPY recoupled for a few hours but are now decoupling faster than the Seahawks and Broncos (S&P -1pt, USDJPY +30 pips). The catalyst for the disconnect (which Japan's Nikkei is also following) was weakness in Chinese data. Following Aussie PMI's lowest print in 5 months,China's Services PMI printed at its lowest on record and it sbiggest 3 month slide in 16 months. Japan's Nikkei 225 is now down 10% in 2014 and 7 of the last 8 days and 20Y JGB yields are testing 9-month lows.

China Services PMI at its lowest on record...

with the biggest 3-month slide in 16 months...

Which triggered a disconnect between stocks and carry...in US futures...

and the Japanese stocks are now down 10% on the year....

and 20Y yields are testing 9 month lows...

Charts: Bloomberg

http://www.theguardian.com/business/blog/2014/feb/03/nikkei-falls-into-correction-territory-as-emerging-market-fears-hit-shares-business-live

ECB: Stress tests will be very rigorous

Over in Frankfurt, the European Central Bank is outlining more details of this year's asset-quality review.

ECB vide-president Vítor Constâncio has pledged that the stress tests will be rigorous:

We will uphold the reputation of the ECB ... we will not put it at risk. Everything will be disclosed.

Constâncio also scotched the idea that the ECB might go soft on eurozone banks because of fears that Europe doesn't have strong enough backstops to help banks who fail the tests.

He pledged:

We will conduct an exercise that is very demanding and very rigorous.

The ECB has also said that it expects to have finalised the "bank-by-bank" portfolio selection for the AQR by the middle of this month.

Banks' who fail the ECB's baseline test will have to raise fresh capital in the 'nearer term', while those who are only fail against the "adverse scenario" will have more time to strengthen their balance sheets.

Updated

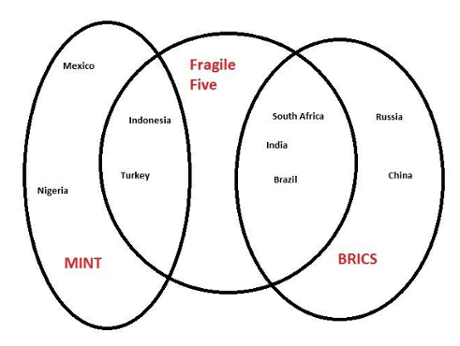

Has all this talk of emerging market problems left you struggling to remember which country is a fast-growing MINT, a reliable BRIC or a fractious member of the Fragile Five?

Well, panic not - here's a handy chart from the TUC's Duncan Weldon, showing the main players in the emerging markets.

Keen-eyed readers will have spotted the overlap -- which rather fuels the idea that you can't put countries into neat little boxes...

— Paweł Morski (@Pawelmorski) February 3, 2014

@DuncanWeldon you'd almost think these were terms coined by a charlatan— Paweł Morski (@Pawelmorski) February 3, 2014

Germany: No new Greek haircut

The German finance ministry has firmly denied reports that a third aid package for Greece could include a further debt haircut.

Reuters' Berlin bureau has the details:

"There is no new situation regarding Greece," said spokesman Marco Semmelmann.Asked about the possibility of a debt writedown, he said: "I can deny that categorically".Weekly Der Spiegel reported this weekend that Berlin was preparing the ground for a third aid package for Greece of 10-20 billion euros which could include a further haircut affecting public creditors or a "limited additional programme" involving fresh funds from the European rescue fund.

As Helena wrote last night, Germany appears to be inching towards agreeing a third loan for Greece, of perhaps €10bn to €20bn.

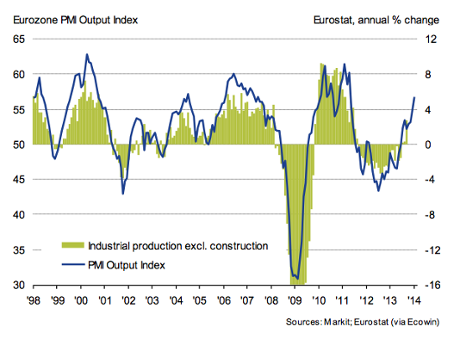

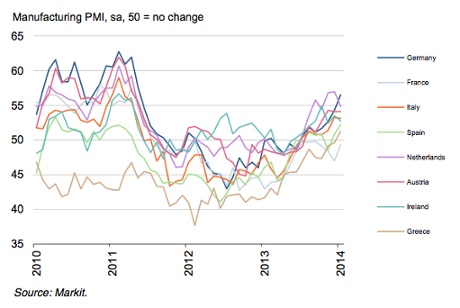

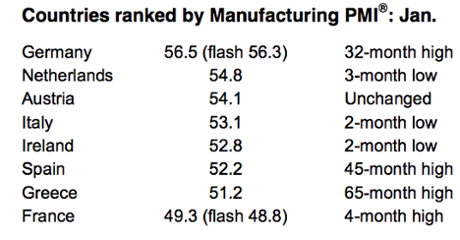

Eurozone factory recovery picks up in January - growth at 32-month high

Europe's manufacturing sector continued to recovery in January, data firm Markit has reported, with the strongest rise in activity since May 2011.

The overall eurozone manufacturing PMI (based on interviews with thousands of firms across the region) rose to 54.0 -- the highest reading in over two and half-years -- showing the recovery picking up pace, from December's 52.7.

Any reading over 50 shows the sector expanded.

Markit reported that factories saw an increase in new orders, leading to an higher backlog of work and an inc increased in job creation across the sector.

Germany saw strong growth again (see here), while at the other end of the spectrum there was encouragement for Greece which reported the first rise in output for 55 months (see here)

Greek manufacturing grew in January for the first time since August 2009. Generally eurozone factories had strongest Jan since mid-2011.— Gavin Hewitt (@BBCGavinHewitt) February 3, 2014

But France remained a laggard, with its factory output falling again, although at a slower pace (see here).

Chris Williamson, chief economist at Markit, said the eurozone manufacturing recovery gained "significant further momentum" in January. All the figures were higher than the 'flash' readings published two weeks ago.

“The survey data indicate that manufacturing output across the eurozone is growing at a quarterly rate in excess of 1%, led by Germany, where the rate of increase is perhaps as strong as 3%. Encouragingly, France is also showing signs of stabilising, enjoying a welcome return to export growth, though manufacturing in the eurozone’s second-largest member state remains in overall decline and a drag on the region.“However, perhaps the most important development in the report is the further revival of manufacturing in the region’s periphery. Both Italy and Spain are seeing robust growth of output and order books, and the Greek PMI’s rise above 50 for the first time since August 2009 is an important signal of how even the most troubled member states are returning to growth.“The improving economic picture painted by the PMI, which is running at a level consistent with euro area GDP growth of 0.4-0.5% for the first quarter, takes the pressure off ECB policymakers to add more stimulus. Price pressures, and the threat of deflation, will no doubt remain a key concern for the ECB, especially as growth of both input costs and selling prices eased in January.”

Updated

No comments:

Post a Comment