Commentary on the economic , geopolitical and simply fascinating things going on. Served occasionally with a side of snark.

Thursday, February 13, 2014

Europe falling apart again -- Greek Unemployment Hits New Record; People Employed Drops To Record Low; 61.4% Of Youth Without A Job ..... Italian PM Enrico Letta's government in danger of collapse Embattled leader challenges rivals including Matteo Renzi to 'lay their cards on the table' ...... Meanwhile both the Bank of England and the EU are studying Bail -ins and deposit mobility schemes aka confiscation of savings and assets !

Something funny happened on the Grecovery: the Grecession.... Actually, make that the Gepression. In a nutshell - according to Elstat, Greek unemployment in November rose to a record high on both a seasonally adjusted and unadjusted basis with 28% of the labor force without a job, the number of people unemployed rose to a record high 1.382 million, even as the number of labor inactive people keeps rising, hitting 3.377 million and on its way to catch up with the rapidly declining 3.55 million people employed, which incidentally in November also posted a new record low. And tying it all together was the Greek youth unemployment rate which posted a record high for November at 61.4%, and after a few months of declines which gave some hope that things are indeed improving is back to its old, soaring ways.

Greek employment table:

Record low number employed:

Record high number unemployed:

Record high unemployment:

Greek youth unemployment: the latest trend is no longer your friend.

ECB's Coeure sees new talks on Greek debts in mid-2014

A new restructuring of Greece's debt is not being discussed by its international lenders though fresh discussions on the sustainability of Athens' debts are likely later this year, a European Central Bank board member said.

Greece has been shut out from the debt markets since 2010, kept afloat solely by a multi-billion bailout package from the European Union and International Monetary Fund.

Under its latest bailout programme, Athens will be financed until the second half of 2014 and Greece says it hopes to return to bond markets after getting the budget into primary surplus - a measure that excludes debt costs - this year.

"Is a new restructuring being discussed? No, it is not being discussed because the agreement in the Eurogroup and with the IMF is that the discussion on debt sustainability will come later in 2014," ECB Executive Board member Benoit Coeure said.

"At some point in 2014, most likely in mid-2014, that discussion on debt sustainability will come again but it is too early to tell," Coeure added in a hearing at the European Parliament.

The ECB, together with the European Commission and IMF, is part of the "troika" of international lenders.

[Reuters]

Finance Ministry to obtain all electronic data on taxpayers’ transactions

By Prokopis Hatzinikolaou

Tax authorities will soon have a complete picture of taxpayers’ transactions as they will be able to check interest paid on bank deposits, credit card payments and most day-to-day spending ranging from electricity bills to private school tuition fees.

The aim is to ascertain the actual incomes of taxpayers that will be cross-checked with their declared incomes. According to a senior Finance Ministry official, authorities have identified taxpayers who spend more than twice as much as they earn on an annual basis according to their income tax declarations without that money having come from deposit withdrawals.

The decision signed by the general secretary for public revenues, Haris Theoharis, forces banks, investment and insurance companies, private clinics, private schools, universities and other tertiary education institutions, fixed and mobile networks, as well as electricity and water utilities to submit to the General Secretariat of Information Systems full details and data on their customers with a full record of their spending in 2013.

The decision calls on credit institutions to submit to the ministry all data relating to deposit interest, bank account transactions above a certain limit, loans, checks, credit card payments, money sent abroad, as well as a full record of transactions by the self-employed and enterprises that are deemed most likely to dodge tax payments.

Water companies will only forward data concerning annual consumption of over 1,000 euros, while private clinics must forward their data with the medical details attached, with the exception of mental health clinics and diagnostic centers.

All data will have to be forwarded to the ministry’s general secretariat by the end of March, and will be retained for six years.

In a report seen by analysts as supporting Greek proposals, Deutsche Bank on Wednesday branded the criterion used to assess the sustainability of the Greek debt – the ratio of debt to GDP – as narrow-minded, and estimated that a new debt restructuring by extending bilateral loans to 50 years could reduce the country’s burden by up to 26 billion euros in net present value terms.

In doing so, Germany’s biggest lender has launched a debate about changing the way debt sustainability is determined, placing more significance on whether it is manageable rather than on its size. It added that Greece will easily secure a primary surplus for the 2013 financial year, which will lead to talks for the measures to ease the country’s debt further “in the coming weeks.”

Separately, Bloomberg said yesterday that Europe will have to learn from its mistakes and should not allow Greece to drown in its debt.

Greek truckers show plight as groceries show up frozen

By Jonathan Stearns

Alexander Paraskevas is on the front lines of Greece's effort to transform itself into an economy that can compete in the 21st century.

Paraskevas, in charge of ensuring goods get from point A to point B for the country's biggest chain of wholesale stores, Metro SA, has hundreds of complaints about truck services that show how far Greece still has to go.

Trucking, like more than 300 other Greek professions, was ordered deregulated as part of the deal for 240 billion euros ($327 billion) in international aid. The whole revamp has yet to produce the promised benefits because of a combination of Greek political procrastination and a recession that has shrunk the domestic economy by about a quarter since 2008.

"Because Greek authorities dithered over deregulation for three years, demand for services and the market dried up and now it will take longer to show positive results," said Michael Mitsopoulos, senior advisor for infrastructure and the business environment at the Hellenic Federation of Enterprises in Athens. "The risk is the public will say: 'look, we liberalized and nothing happened, so let's go back.' This whole initiative could get discredited."

With Europe’s leaders having declared victory in the four-year-old battle to keep the euro area intact and Greek Prime Minister Antonis Samaras asserting the worst is over for his country, the next step of rebuilding Greece's shattered economy remains in abeyance. Euro area policy makers' doubts about the pace of reform are holding up the country's next aid payment.

Protected Market

In the case of Athens-based Metro, that means continuing to rely on its own trucking fleet, which the company created to avoid having to rely on a long-protected public market for road transport in the country.

Most Greek businesses handle their logistics in-house because for decades they didn't want to risk their cash flow at the hands of a strike-prone trucking cartel.

"The problem was and remains the level of professionalism" in Greek public road haulage, Aristotelis Panteliadis, Metro’s managing director, said in an interview in Athens. "This hasn’t improved because, as a result of the crisis, nobody can make investments."

Greece has fully deregulated 285, or 83 percent, of 345 professions slated for market opening under the nation’s rescue program financed by the euro area and the International Monetary Fund, according to the Greek Finance Ministry. Deregulation is in the works for all the rest, says the ministry.

Regulated Professions

These "regulated" professions represent a third of private employment in Greece, according to the Organization for Economic Cooperation and Development. Shuttle buses are another example.

"To date, the benefits from these regulatory adjustments have been modest," the Paris-based OECD said in a survey of Greece published in November. "The benefits of liberalization in road haulage and the occasional passenger transport have yet to make themselves felt."

This threatens to cost the government, clinging to a three-seat majority in parliament, popular support as Samaras fends off attacks from the main opposition SYRIZA party opposed to the aid conditions.

"You need direct investment first to create liquidity in the market and get out of the recessionary spiral," said Theodore Krintas, managing director of Athens-based Attica Wealth Management, which oversees 100 million euros. "Then changes such as the opening of closed professions will reinforce the upward momentum. These are important decisions for the Greek economy and I do believe the benefits will come."

Restricted Rights

Greece has about 33,000 trucks with public licenses to transport goods on behalf of customers and about 1 million vehicles, including vans, with more restricted delivery rights as companies’ private fleets.

Metro, which began business in 1976, has a 38-vehicle fleet of Mercedes-Benz, Iveco and DAF trucks handling 70 percent of its deliveries. These deliveries go to 45 "Cash & Carry" wholesale outlets and 58 "My Market" retail stores located across the country, from northeastern Greece near the border with Turkey to the southern island of Crete.

The Greek logistics market, including trucking, symbolizes how out of step the country's economy is with the rest of Europe. European companies on average outsource 80 percent of their logistics needs, while Greek businesses outsource a mere 20 percent, according to Kostas Theofanides, who worked as transportation manager for the Greek units of US oil producer Exxon Mobil Corp. and Britain’s BP Plc for about a decade.

No Light

"The public trucking market in Greece has a huge chance to expand," said Theofanides, who is now a business-development consultant at Projectyou.gr. "But there’s a 52 percent drop in demand. People are depressed. They don’t see light at the end of the tunnel."

Beyond the collapse of demand, the obstacles are a lingering lack of private trust in the public market because it used to stage strikes twice a year; internal resistance within companies that have private fleets to giving those up; and a lack of big organizations in the public-trucking fleet, which is owned by more than 29,000 truckers, he says.

George Stergiou, secretary general of consumer affairs at the Greek Development Ministry, said the deregulation drive has been "very painful and time consuming" and will yield tangible results once credit returns to the market.

"We have to stress the interests of the Greek public," Stergiou said. "Gradually, a majority is emerging for these changes. There’s enormous growth potential."

63 Permits

Greece's previous Socialist government deregulated public trucking four years ago over protests by drivers, abolishing a limit on licenses for outsourced deliveries. Since then, only 63 new public truck permits have been issued, according to the Greek Transport Ministry.

"Nothing has changed since liberalization," said Apostolos Kenanidis, president of the Hellenic Federation of International Road Transport, which opposed deregulation. "It’ll be difficult for anyone else to enter the market as long as we keep our costs low."

For Metro, a move to extra outsourcing depends on more than competitive prices in the public market.

"We have no complaint with pricing, but we too often have a problem with quality of services," said Panteliadis. "That needs investment."

Service Complaints

Paraskevas, Metro’s logistics manager, has evidence at his fingertips of subpar service provided by public truckers on whom the company relies for 30 percent of its deliveries.

In his office at a logistics park an hour north of Athens, he pulled up a spread sheet showing 255 complaints by Metro about its outsourced deliveries over the past three years, including 108 in 2013. Averaging one every three to four days, these "claims" relate to such troubles as broken-down trucks, late vehicle arrivals and wrong storage temperatures.

"Sometimes you get frozen groceries," Paraskevas said as several public-market trucks were docked alongside blue-painted Metro vehicles at the company’s warehouse next door. The warehouse, with 56 docks and a 24-hour loading service, is the main structure on a site that employs about 340 of Metro's 4,200 workers and that costs the company 16 million euros a year to operate.

Before showing off an area where Metro cleans its trucks every two days and carries out maintenance on the vehicles, Paraskevas said another common complaint by the company related to inappropriate dress or behavior by public truckers. He pointed out three Metro claims that drivers of outsourced deliveries had urinated in public near the docks.

Market Opportunities

Nonetheless, Panteliadis said "there is a trend toward the public market" in Greek trucking and Metro might boost reliance on these operators to 50 percent of its road shipments in three to five years from the current 30 percent.

That represents an opportunity for Greek trucking companies such as Med Frigo SA.

Med Frigo, which delivers Greek fresh fish to markets outside Greece including Germany, Italy, Spain, Switzerland and the UK, is considering expanding its services to destinations inside the country, according to Sotiris Marinakis, the company's logistics manager.

He said that Med Frigo, whose motto is "Always on Time," is examining options for serving areas around Athens and northwestern Greece and that Metro could be an attractive and interested customer.

Asked whether Med Frigo had contacted Metro about a possible business relationship, Marinakis said that step would take more time.

Marinakis made the remark as Panteliadis walked past on his way out of a logistics conference in Athens. While Greece is desperate for economic change, the country's road transporters are taking time to alter their ways.

Matteo Renzi's Democratic Party has voted to back his proposal fore a new government... and Prime Minister Letta has resigned.

*DEMOCRATIC PARTY VOTES IN FAVOR OF RENZI PROPOSAL FOR NEW GOVT

*ITALY PREMIER LETTA SAYS HE WILL RESIGN

This will bring the 65th government in Italy since World War II and the 3rd consecutive government that would not have been elected (the last elected Prime Minister was Berlusconi in 2008).

Renzi's speech in preparation for the vote was farcical and confused:

*RENZI SAYS ITALY CANNOT CONTINUE TO LIVE IN UNCERTAINTY

*RENZI SAYS ITALY NEEDS TO EXIT SWAMP, NEEDS CHANGE (but same coalition parties)

*RENZI SAYS NEW ELECTIONS WOULDN'T GUARANTEE CLEAR MAJORITY

*RENZI SAYS THIS IS TIME TO BE RESPONSIBLE, TAKE RISKS

While Letta had his "57-page plan" of reforms, Renzi does not differ greatly (and thus there will be no change) as the confrontation hinges on who is better placed to implement them.Markets are rallying on the news.

Mr. Renzi's own proposals don't contrast with those of Mr. Letta. The confrontation hinges on which of the two are better placed to implement their plans.

...

Ten months ago [Letta] gave his government—Italy's first left-right coalition since the late 1940s—18 months to carry out an ambitious program including constitutional reform, a new electoral law and measures aimed at bolstering what has been the euro zone's weakest economy since 2000. Progress has been slow and, as Mr. Letta lamented on Wednesday, many laws have been passed but their enactment decrees never promulgated.

...

"We would regard a Renzi premiership as a positive development for Italy, possibly imparting a new drive to the reform agenda," Citigroup C -0.90% analysts said in a note.

On the other hand, he risks having to operate within the current parliament without a clear electoral mandate, which could compromise both his influence and his image as a novelty in Italian politics, said J.P. Morgan analyst Alex White.

...

Italy's last elected prime minister was Silvio Berlusconi, who won an ample majority in the 2008 elections.

Matteo Renzi, the charismatic young mayor of Florence, was elected last December as leader of Italy's most powerful political organisation, the centre-left Democratic Party (PD) - the dominant faction in the current coalition government.

Matteo Renzi is just 39 years old and has never been a member of parliament. Now he has called publicly for a new government, directly challenging Prime Minister and party rival Enrico Letta.

The young party leader is sometimes called Il Rottamatore ("The Scrapper"). The nickname refers to his call to scrap the entire Italian political establishment, which is widely regarded as discredited, tainted by corruption, and as having failed the nation decade after decade.

His rise has been seen as a sign of much-needed generational change, and he enjoys by far the highest approval rating of any politician in the country. He is in his own words "hugely ambitious".

Mr Renzi presents himself as a break with the past in every way, BBC Rome correspondent Alan Johnston reports.

He exudes a restless energy. He likes to pace the stage in black jeans and attends meetings in shirt sleeves. He travels around either in a small car or on a bicycle.

He is relaxed and easy - fast and fluent as he speaks without notes, ranging across Italy's many problems, and offering broad-brush solutions.

He always seeks to instil a belief that politics can be done differently, that change is possible.

He once finished a televised debate by saying he would offer something very rare in Italy: "Hope."

"People are weary and disillusioned," he said. "They don't believe anymore. I believe, and that's why I do politics - because I still believe."

Italian Stocks & Bonds Fall As Government Collapse Looms

Submitted by Tyler Durden on 02/13/2014 09:28 -0500

Having rallied yesterday and totally ignored the fact that Letta's 10-month-old government was about to collapse, Italian equity and sovereign bond markets are falling this morning by their most in two weeks. The main bone of contention for Renzi-Letta fight is jobs and growth - there is none of either - and while Prime Minister Letta assures that the Italian economy grew in Q4 (GDP data to be released tomorrow) for the first time in 10 quarters, as Bloomberg's Niraj Shah notes, real GDP is still smaller than it was in 2000. Letta has just canceled his UK visit (planned for 2/24) and did not take part in the Democratic Party meeting with a Renzi friend saying "[Letta] will resign."

Via Ansa

Premier Enrico Letta said Thursday that he would not attend a meeting of his centre-left Democratic Party (PD) that has been called to decide whether it should continue backing his coalition government. New PD leader Matteo Renzi may call on the party to pull its support for Letta so he can take over as premier. Letta said he would not go to the meeting so that his party could "decide with serenity".

However, with unemployment at record levels, we suspect few will care about some manufactured, goodwill-enhanced GDP print. Italians are, of course, used to the farce that is politics - there have been 64 government since 1945.

Source: Bloomberg

Italian PM Enrico Letta's government in danger of collapse

Embattled leader challenges rivals including Matteo Renzi to 'lay their cards on the table'

Italian Prime Minister Enrico Letta faces an increasingly formidable threat to his premiership. Photograph: Riccardo De Luca/AP

The government of embattled Italian prime minister, Enrico Letta, looked close to collapse as he dug in his heels in the face of an increasingly formidable threat to his premiership from the leader of his centre-left party.

Letta said it was "not in [his] DNA" to break with the agenda of his government and challenged Italy's political players – chiefly Matteo Renzi, his ambitious young rival – to "lay their cards on the table".

Less than 10 months after it was born from the inconclusive mess of last February's general elections, long-running criticisms of the coalition government's lacklustre record gathered force, putting Renzi, the 39-year-old mayor of Florence, in a leading position to take over as prime minister in an election-free process branded by the media as la staffetta– the relay.

The situation was opaque and the likely outcome of the power struggle unclear . The large national committee of the Democratic party (PD) was due to meet on Thursday to deal with the issue, possibly even putting it to a vote. Giorgio Napolitano, the 88-year-old president whose role it is to appoint prime ministers, has made it clear that the party must give a clear sign of what it wants.

In a message posted on Twitter, Renzi said he would "say what I have to say" before the PD, "live-streamed, in the open". Earlier, the sharp-talking politician had arrived at the doors of Palazzo Chigi in a small blue Smart car for a meeting with Letta which the premier said was "as you [journalists] say, 'frank'".

Speaking of the PD meeting, the prime minister added: "I am simply asking for clarity ... Resignations aren't handed in because of gossip or ruses… I think everyone should express themselves explicitly. Everyone should say what their intentions are." Especially, he added, if that person was looking to fill his shoes.

Ever since he won the primary elections for the PD leadership by a landslide in December, Renzi – a politician viewed as refreshingly energetic by his supporters and insufferably brash by his critics – has kept up regular attacks on Letta's government from the sidelines, pointing out its failings and urging it to do more, particularly focusing his energies on pushing through a new electoral law.

But, until recently, the idea of taking over from his colleague without first going to the polls is not understood to have been considered a viable option. Were he to take over the reins in a staffetta, he would become Italy's third unelected prime minister in under three years, after Mario Monti was brought in to head a technocratic government at the end of 2011 and Letta was put in charge of his awkward coalition with Silvio Berlusconi's centre-right party last April.

According to opinion polls, it is not a move many Italians support, despite their approval of Renzi himself, with an unofficial survey on the television station SkyTG24 showing 74% against a possible takeover and 26% in favour. But Napolitano, who has the final say, is understood to want to avoid snap elections under the old, dysfunctional electoral law, at all costs.

A source in Renzi's circle, who did not want to be named, said:"For Matteo, it's a big risk. A very big risk. But I think it's the only real chance we have of reforms." The PD leader would manage it, the source added, "but it's a real tug of war."

A pro-Renzi MP in the PD agreed it was a high-stakes strategy on the leader's part, but added: "It would also be a big risk to wait a year and then go to an election without having concrete results to show for it."

After a day of feverish speculation, and a face-to-face meeting with his challenger that apparently served only to entrench both men in their opposing positions, Letta went ahead with a press conference evening to unveil what he said was a new coalition pact for a revamped government in 2014. How long it went on for, he said, was entirely linked with how long it would take to carry out the institutional and economic reforms that Italy needed.

He was still working with "determination", he said, defending his record and insisting that, if time had been wasted over the past nine-and-a-half months, "it is not my fault".

Until the autumn, the PD's major coalition partner was Berlusconi's then centre-right party, the Freedom People (PdL), a combination that did not make for easy-going and focused reform. The former prime minister and media mogul later withdrew his support from the coalition and reformed his Forza Italia party in opposition.

Recalling the "crisis situation" in which his government was formed last year, Letta said he had always considered it to be "a government of service" and appeared at pains to stress how unusually difficult his period as prime minister had been, repeatedly declaring he had been living "each day as if it was the last".

"It would be absolutely paradoxical and contradictory and absolutely is not part of my DNA to break with the continuation of a spirit which I consider, even now, deeply linked to the service of the country and not linked to my personal prospects," he said. "My personal prospects do not enter into this affair at all."

But, despite his assurances, Letta, a 47-year-old former minister and MEP, appeared increasingly isolated. A PD MP who did not back Renzi in the primaries said that even the mayor's internal opponents had come round to the idea of him taking over. "By now this is quite a widely held position," he said, speaking on condition of anonymity. "Let's say that [Renzi] has been very good at dealing with many of our proposals, for example on the electoral law, and obviously we are all embarrassed by the slowness of the Letta government in recent weeks. So unfortunately we too are quite critical."

It has been claimed, however, that, rather than finally coming round to him as the leader they need, Renzi's foes may be seeking to tarnish his golden boy image by getting him to take a poisoned chalice which could damage his promising career for a long while to come.

Bill Emmott, the former editor of the Economist and co-writer of a recent documentary on Italy, remarked that, rather than a relay, the mooted move could be more of a hospital pass.

Political rivals

Matteo Renzi, aka The Scrapper

Age: 39

From: Florence

Current role: Leader of Democratic Party; mayor of Florence

Previous experience: President of Florence province

Enrico Letta

Age: 47

From: Pisa

Current role: Prime minister of Italy

Previous experience: Ex-industry minister and european affairs minister; ex-MP and MEP; former deputy leader of Democratic Party

Enrico Letta will not be attending the Democratic Party meeting that might seal his fate as PM -- he’ll be dealing with matters of state in his office, according to Reuters:

Today’s AM fix was USD 1,286.50, EUR 942.84 and GBP 778.47 per ounce.

Yesterday’s AM fix was USD 1,282.75, EUR 938.09 and GBP 780.83 per ounce.

Gold climbed $15.30 or 1.2% yesterday to $1,289.90/oz. Silver rose $0.15 or 0.75% to $20.20/oz.

Are Your Savings Safe From Bail-In? (GoldCore)

Gold is marginally lower today in all currencies after eking out more gains yesterday after Yellen confirmed in her testimony that ultra loose monetary policies and zero percent interest rate policies will continue.

Citi Futures are looking for gold to increase by a further 8.5% by the end of March after gold closed above its 50 DMA every day for the last two weeks and closed above its 100 DMA for two straight days. RBC are less bullish but expect gold prices to increase another 10% and surpass $1,400/oz in 2014.

Gold touched resistance at $1,294/oz yesterday. A close above the $1,294/oz to $1,300/oz level should see gold quickly rally to test the next level of resistance at $1,360/oz. Support is now at $1,240/oz and $1,180/oz.

Yellen confirmed that the U.S. recovery is fragile and said more work is needed to restore the labor market. She signalled the Fed’s ultra loose monetary policies will continue and the Fed will continue printing $65 billion every month in order to buy U.S. government debt.

The dovish take from Yellen's testimony yesterday should support gold prices. Continuing QE makes gold attractive from a diversification perspective.

Market focus shifts from the U.S. to the UK today and the Bank of England’s quarterly inflation report.

The U.K. has already almost breached the unemployment level that was a target for considering tightening policy, and Governor Mark Carney is widely expected to update the market on interest rate guidance.

Possibly of more importance is the fact that the Bank of England is to test whether UK banks and building societies would go bust if house prices crash. A ‘stress test’ will examine whether banks will need bailing out, or bailing in as seems more likely now, if house prices materially correct again.

Preparations have been or are being put in place by the international monetary and financial authorities, including the Bank of England for bail-ins. The majority of the public are unaware of these developments, the risks and the ramifications.

The test is being drawn up by the Bank’s Financial Policy Committee, whose members include Governor Mark Carney.

A Nationwide Building Society survey just out showed house prices had risen by 8.8% in January over the same month last year. London house prices have all the symptoms of a classic bubble.

Many UK banks are already over extended and the real risk is that many banks would not be able to withstand house price falls. This heightens the risk of bail-ins.

At first we thought Reuters had been punk'd in its article titled "EU executive sees personal savings used to plug long-term financing gap" which disclosed the latest leaked proposal by the European Commission, but after several hours without a retraction, we realized that the story is sadly true. Sadly, because everything that we warned about in "There May Be Only Painful Ways Out Of The Crisis" back in September of 2011, and everything that the depositors and citizens of Cyprus had to live through, seems on the verge of going continental. In a nutshell, and in Reuters' own words, "the savings of the European Union's 500 million citizens could be used to fund long-term investments to boost the economy and help plug the gap left by banks since the financial crisis, an EU document says." What is left unsaid is that the "usage" will be on a purely involuntary basis, at the discretion of the "union", and can thus best be described as confiscation.

The source of this stunner is a document seen be Reuters, which describes how the EU is looking for ways to "wean" the 28-country bloc from its heavy reliance on bank financing and find other means of funding small companies, infrastructure projects and other investment. So as Europe finally admits that the ECB has failed to unclog its broken monetary pipelines for the past five years - something we highlight every month (most recently in No Waking From Draghi's Monetary Nightmare: Eurozone Credit Creation Tumbles To New All Time Low), the commissions report finally admits that "the economic and financial crisis has impaired the ability of the financial sector to channel funds to the real economy, in particular long-term investment."

The solution? "The Commission will ask the bloc's insurance watchdog in the second half of this year for advice on a possible draft law "to mobilize more personal pension savings for long-term financing", the document said."

Mobilize, once again, is a more palatable word than, say, confiscate.

And yet this is precisely what Europe is contemplating:

Banks have complained they are hindered from lending to the economy by post-crisis rules forcing them to hold much larger safety cushions of capital and liquidity.

The document said the "appropriateness" of the EU capital and liquidity rules for long-term financing will be reviewed over the next two years, a process likely to be scrutinized in the United States and elsewhere to head off any risk of EU banks gaining an unfair advantage.

But wait: there's more!

Inspired by the recently introduced "no risk, guaranteed return" collectivized savings instrument in the US better known as MyRA, Europe will also complete a study by the end of this year on the feasibility of introducing an EU savings account, open to individuals whose funds could be pooled and invested in small companies.

Because when corporations refuse to invest money in Capex, who will invest? Why you, dear Europeans. Whether you like it or not.

But wait, there is still more!

Additionally, Europe is seeking to restore the primary reason why Europe's banks are as insolvent as they are: securitizations, which the persuasive salesmen and sexy saleswomen of Goldman et al sold to idiot European bankers, who in turn invested the money or widows and orphans only to see all of it disappear.

It is also seeking to revive the securitization market, which pools loans like mortgages into bonds that banks can sell to raise funding for themselves or companies. The market was tarnished by the financial crisis when bonds linked to U.S. home loans began defaulting in 2007, sparking the broader global markets meltdown over the ensuing two years.

The document says the Commission will "take into account possible future increases in the liquidity of a number of securitization products" when it comes to finalizing a new rule on what assets banks can place in their new liquidity buffers. This signals a possible loosening of the definition of eligible assets from the bloc's banking watchdog.

Because there is nothing quite like securitizing feta cheese-backed securities and selling it to a whole new batch of widows and orphans.

And topping it all off is a proposal to address a global change in accounting principles that will make sure that an accurate representation of any bank's balance sheet becomes a distant memory:

More controversially, the Commission will consider whether the use of fair value or pricing assets at the going rate in a new globally agreed accounting rule "is appropriate, in particular regarding long-term investing business models".

To summarize: forced savings "mobilization", the introduction of a collective and involuntary CapEx funding "savings" account, the return and expansion of securitization, and finally, tying it all together, is a change to accounting rules that will make the entire inevitable catastrophe smells like roses until it all comes crashing down.

So, aside from all this, Europe is "fixed."

The only remaining question is: why leak this now? Perhaps it's simply because the reallocation of "cash on the savings account sidelines" in the aftermath of the Cyprus deposit confiscation, into risk assets was not foreceful enough? What better way to give it a much needed boost than to leak that everyone's cash savings are suddenly fair game in Europe's next great wealth redistribution strategy.

A Brussels/Frankfurt EC document seen by Reuters proposes to use the savings of the European Union’s 500 million citizens to fund long-term investments, boost the economy, and help plug the increasingly large gap left by eurobanks since 2009.

The Slog exclusively revealed in April 2013 that Greek negotiators with the Troika had leaked the fact that the country’s lenders had tabled a pension/savings grab. Clearly, the idea hasn’t gone away…either in Athens or at the ECB. Three days later, these columns revealed wide awareness among the european markets and the euroélite of a massive outflow of investment funds from the eurozone area. At one point last year, Mario Draghi quietly suppressed capital flight data for four months.

Now the situation is desperate, and desperate measures are very much back on the table.

“The economic and financial crisis has impaired the ability of the financial sector to channel funds to the real economy, in particular long-term investment,” said the document, seen by Reuters. The European Commission will soon ask the bloc’s insurance watchdog for advice on a possible draft law “to mobilize more personal pension savings for long-term financing”, the document said. After the May euroelections, naturally.

But the best bit of Orwellian doublespeak in the leaked file is this one: ‘the Commission will consider whether the use of fair value, or pricing assets at the going rate, in a new globally agreed accounting rule, is appropriate, in particular regarding long-term investing business models’.

Yes fellow citizens, reality and market valuations are no longer appropriate…we’re bust, so we need a new globally agreed accounting rule.

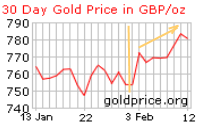

Like, for instance, the value of gold in central bank balance sheets? Look at the price of gold – £27 up in ten days:

Is this another Draghi/CEntral bankers’ directionalising exercise before the next revaluation of gold? Get the punters in, sell off, watch them panic, buy again at £650?

Submitted by Tyler Durden on 02/13/2014 08:08 -0500

Submitted by Tyler Durden on 02/13/2014 08:08 -0500

A Brussels/Frankfurt EC document seen by Reuters proposes to use the savings of the European Union’s 500 million citizens to fund long-term investments, boost the economy, and help plug the increasingly large gap left by eurobanks since 2009.

A Brussels/Frankfurt EC document seen by Reuters proposes to use the savings of the European Union’s 500 million citizens to fund long-term investments, boost the economy, and help plug the increasingly large gap left by eurobanks since 2009.

Is this another Draghi/CEntral bankers’ directionalising exercise before the next revaluation of gold? Get the punters in, sell off, watch them panic, buy again at £650?

Is this another Draghi/CEntral bankers’ directionalising exercise before the next revaluation of gold? Get the punters in, sell off, watch them panic, buy again at £650?

A Brussels/Frankfurt EC document seen by Reuters proposes to use the savings of the European Union’s 500 million citizens to fund long-term investments, boost the economy, and help plug the increasingly large gap left by eurobanks since 2009.

A Brussels/Frankfurt EC document seen by Reuters proposes to use the savings of the European Union’s 500 million citizens to fund long-term investments, boost the economy, and help plug the increasingly large gap left by eurobanks since 2009. Is this another Draghi/CEntral bankers’ directionalising exercise before the next revaluation of gold? Get the punters in, sell off, watch them panic, buy again at £650?

Is this another Draghi/CEntral bankers’ directionalising exercise before the next revaluation of gold? Get the punters in, sell off, watch them panic, buy again at £650?

No comments:

Post a Comment