Commentary on the economic , geopolitical and simply fascinating things going on. Served occasionally with a side of snark.

Thursday, May 2, 2013

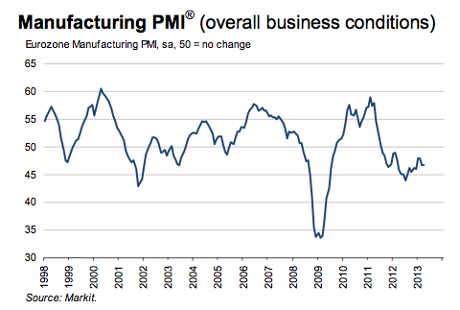

European update - May 2 , 2013 ..... Waiting for Draghi and the ECB rate decision ........ Eurozone Manufacturing PMI data released for April - Germany down to 48.1 ( from 49 ) , France , Spain , Italy and Greece still well into contraction ( ranging from Spain - 44.7 , France - 44.4 , Greece - 45 and Italy - 45.5 ) .....Italy GDP forecast to fall -1.5 percent for 2013 ... Did Monti " unwittingly " stab new PM Letta in the back ?

Bilderberg 2012 participant and newly appointed Italian Prime Minister Enrico Letta apparently wrote a letter to departing PM Mario Monti, who in turn unwittingly showed it to the press.

Letta’s signature on his recent appointment as Prime Minister of Italy hardly dried or a photograph catches Monti unwittingly presented a letter pointing to bartering in respects to who will be given what position in Letta’s new cabinet, both officially and privately.

The letter, appearing to contain words written by Letta directed at the former prime minster Mario Monti, was obviously shown to the press by the departing PM by accident. Although the letter was presented upside-down, a simple rotation revealed the text, reading as follows:

“Mario, when can you tell me the forms and ways that I can be useful, both officially (Bersani asks me e.g. to interact on the question of vice) and privately. For now it seems to me a miracle! And then miracles exist!”

The Bersani mentioned in the letter refers to Pier Luigi Bersani, who was responsible for the formation of the current cabinet. This letter begs the question, to whom or whose cause Letta (as Prime-Minister) wants to be useful both in official and unofficial capacity. Could it be an echo of his pledge to Bilderberg, which he visited in 2012?

This is less farfetched than one might think. In November of 2012, the Bilderberg steering committeeconvened a special dinner in Rome, inviting Monti to the dinner table, suggesting prearrangement not only of the preferred menu, but also Italy’s political future in the global context. Letta was present at the last Bilderberg conference at the Chantilly Hotel in Virginia, thereby guaranteeing himself a position of power in the near future.

Italy’s former premier, Mario Monti, earlier hailed Letta, trusting he “will be able to consolidate Italy’s international credibility”.

Monti has a last laugh at the expense of new Prime Minister Letta ......

Let us forgive those shoving Hellenic heads down the toilet, for they know not what they’re doing

The Troika and other Centres of Incompetence within Brussels-am-Berlin have been making predictions in one form or another about Greece since early 2010. The inaccuracy of these prévisions make the British Met Office seem a model of 99.9% accuracy by comparison.

Yesterday having been May Day, Athens was replete with protests organised by public and private sector unions and opposition parties. As a result (and to make life difficult for the sake of it) the Samaras shambles government closed four metro stations in central Athens from 9 am. Obviously, the Athenian population was protesting about a pointless austerity that has ripped the heart from the City’s economy without anaesthetic. But in truth, they should be demonstrating about this being brought upon their heads by people who clearly have no idea WTF they’re about.

One can begin illustrating the Troikanaut level of braindeath using the medium of their forecasts since 2010.

Lawyer, no economics degree

Starting with GDP forecasts, according to The Plan, GDP was supposed to bottom out in 2011 at ~8% below its 2008 level. By 2012, the Greek economy was supposed to be growing at 1.1%. Instead, GDP is 20% below its 2008 level and continuing to contract. In Troikaland, growth only ever occurs Next Year.

Moving onto the country’s debt, the initial forecast saw Greece’s debt/GDP ratio peaking at 149% of GDP in 2011 and 2012. But this assumed a starting point of 115% of GDP in 2009. Instead, debt in 2009 was 130% of GDP and the peak came in 2011 at 171% before a restructuring brought it down to 157% of GDP in 2012.

Poet, no economics degree

As to inflation, the forecast in 2010 expected that prices in 2012 would be a mere 4% higher than in 2008. Instead, prices in 2012 were 10% higher than in 2008—a miss of some 160%. As the IMF explained later, it underestimated the “monopolistic and quasi-monopolistic structures of the Greek marketplace” that would prevent prices from falling. Actually, the main thing Lagarde grossly underestimated was her personal ignorance, despite the fact that simply reading her own hopeless forecasts about the French deficit (when she was in charge there) could’ve provided here with a very clear steer about it.

Spook, no economics degree

And last but not least, unemployment. The 2010 forecast predicted that unemployment would peak at 14.8% in 2012 before declining to 14.3% in 2013. Instead, unemployment in 2012 averaged 24.2% and reached 26% in Q4 2012. The Troika was one year, 60% and 500,000 people adrift in that area.

All up, the Greek economy has contracted by more than twice the amount forecast in May 2010, prices have risen 1.6 times faster than anticipated, and unemployment has been 60% higher than predicted.

First degree idiot

As for the use of tax increases, the recent shale-fracking debate clearly had a major influence on the BamB Gauleiters, in that it led them to believe they could extract blood from stone. But this too proved a false hope. Massive tax hikes in Greece continue to backfired, the Greek Finance Ministry this week recording a huge leap in overdue payments from citizens by €800m in March, bringing the total outstanding to more than €2.17bn. I suppose if someone doubles the electricity tax on a bill you couldn’t pay last time, this is not that unexpected an outcome. The fresh arrears brought the total amount of debts to the state from all sectors to €57.2bn.

And the latest diagnosis? Greek finance minister Stournaras and Troikanaut Thomsen two weeks ago forecast a gradual return to growth for Greece ‘from’ 2014. Greece was, said the latter, “on track”. I’m at a loss to know what track he was referring to, but it certainly wasn’t anything to do with the forecasts tracked above. I’m thinking of changing my personal noun for Greece’s creditors to Troikanoughts.

Meanwhile, having rogered Greece anally with a yard-brush since 2009, German carpetbaggers continue to try and steal the country’s remaining gold. A second man traveling with 15.7 kilos of unregistered gold destined for the Fatherland was detected by customs officials at Athens International Airport on April 26. Two weeks earlier, customs officials at the same airport arrested a 32-year-old German national in possession of 470 kilos of silver, 7 kilos of gold and 293,000 euros in cash. It seems that every Greek cloud has a German silver lining; but when it comes to Troika expertise, all that glistens is not gold. To be precise here, none of it is.

By Jan Strupczewski

Throughout Europe's debt crisis, northern European leaders have often said they will not stand for taxpayers having to fork out for other countries' problems, and the notion of "taxpayer-funded bailouts" has taken root.

Yet despite three-and-a-half years of debt and banking turmoil, with bailouts totaling more than 400 billion euros, northern euro zone taxpayers have not actually lost a cent.

What is more, governments in Germany, Finland, Austria, the Netherlands and France have saved billions of euros thanks to a sharp fall in how much they pay to raise money in financial markets since their borrowing costs have dropped steeply.

But that has not prevented the image taking root in voters' minds of hard working northern Europeans putting money on the line to rescue profligate, work-shy southerners, fueling resentment and undermining Europe's unity.

In the run up to German elections in September, that resentment is only likely to grow, and Chancellor Angela Merkel, bidding for a third term in office, will have to reaffirm her commitment to protect voters from potential losses.

But the truth remains that German taxpayers, as well as those in Finland, the Netherlands and elsewhere, are no worse off at all, and their finance ministries have racked up savings.

"As an unintentional consequence of the crisis, Finland has benefited enormously," said Martti Salmi, the head of international and EU affairs at Finland's ministry of finance.

"We have not lost a cent so far," he told Reuters. "The same as for Germany very much holds for Finland."

In fact, German officials are well aware of their stronger financing position, the result of a more than two percentage point fall in borrowing costs, even as politicians continue to lament the risks being piled on German taxpayers.

When giving presentations in Germany, Klaus Regling, the German who heads the euro zone's permanent bailout fund, often cites two studies that show that Berlin has reaped substantial savings as an unintended consequence of the crisis.

One study, by German insurance giant Allianz, has calculated that Berlin saved 10.2 billion euros in 2010-2012 because of lower borrowing costs, as yields on its 10-year bonds fell from 3.39 percent to 1.18 percent now.

The other study, by Jens Boysen-Hogrefe of the IfW economic institute, suggests that the German federal budget saved 8.6 billion euros in 2011 due to low ECB interest rates and the safe-haven impact of investors putting money into Germany.

Those savings rose to 9.6 billion in 2012 and the safe-haven effect will alone be worth 2 billion in 2013, IfW said.

"If we add up the interest rate advantages gained in the period 2010 to 2012 and those that Germany will benefit from in the years to come, we arrive at cumulative interest relief for the German budget of an estimated 67 billion euros," Allianz said in a paper published last September.

"(That is) enough to slash around 3 percentage points off Germany's government debt ratio," which reaps further saving.

Finland, the Netherlands, Austria and France may not have gained as much as Germany, but have also seen a substantial decline in borrowing costs over the crisis period.

"Northern European countries are making a considerable profit out of these operations and they are not even redistributing these direct and indirect benefits," said a senior official in Brussels.

The heart of the misconception about taxpayers losses is the fact that in public discourse, the difference between lending and giving has ceased to exist.

And with anti-bailout sentiment so strong in much of northern Europe, there has been no willingness on the part of politicians to correct that misconception. The anti-EU True Finns party in Finland, for example, draws support from the belief that Finns are spending money on southern Europeans.

The situation is quite different. While Finland may be providing lots of guarantees to the eurozone's bailout funds and has lent money to bailed out countries, the Finnish finance ministry has earned extra money from the crisis.

Last year, the Finnish central bank contributed 227 million euros to the Finnish budget as a result of profits made on the Greek, Spanish and Portuguese government bonds it holds, 40 million euros more than it made in 2011.

This year, the profit should rise to 360 million.

For any euro zone country that has provide bailout assistance to lose money, Greece, Ireland, Portugal, Spain or Cyprus would have to default on the loans they have received.

But rather than being close to default, Portugal and Ireland are near to exiting their bailout programs and pose little risk, while the chance of default Spain has always been minimal and is closely managed in Cyprus.

Greece, which has received 166 billion euros in bailout loans, poses the biggest risk, but even that is changing.

"With every day, the risk that Greece would cost taxpayers anything decreases," a second EU official said. "It is not doing badly at the moment and there is a possibility it may do better than assumed."

Apart from the initial bilateral loans to Greece in 2010 which totaled 52.9 billion euros, no euro zone taxpayer money was sent to Greece, or any other country. All the later bailouts were financed on markets via the eurozone bailout fund.

Officials said that even if any of the bailed-out countries were to not pay back some of the money borrowed from euro zone governments, the alternative -- a euro zone break-up -- would have been a much costlier affair than any bailout losses.

A study commissioned by the German Bertelsmann Foundation showed this week that if Germany were to return to its old Deutschmark, its annual GDP would be 0.5 points lower between 2013 and 2025, resulting in a loss of 1.2 trillion euros over the 13 years - half the size of the German economy in 2012.

"It is possible that we will get out of it without getting our feet wet, or with getting our feet wet only a little bit," Finland's Salmi said about the likelihood of a default on any of the bailout loans extended to rescued countries.

"But if we end up forgiving a loan of 1 billion euros to Greece sometime in the next 10 years, that's nothing compared to what we would have faced if we had a meltdown of the euro zone. It would be completely insignificant compared to that," he said. [Reuters]

Emma Delta lands controlling stake in gaming monopoly after upping its bid by 30 million euros

By Vangelis Mandravelis

The Hellenic Republic Asset Development Fund (TAIPED) announced on Wednesday the sale of the state’s 33 percent controlling stake in OPAP to the Emma Delta consortium after receiving an improved offer totaling 712 million euros, marking the completion of Greece’s first major privatization project.

The price agreed is 30 million euros higher than the Czech-Greek consortium’s original offer, although it is 18 million short of what TAIPED had hoped to make from the sell-off.

A total of 622 million euros – the original offer – will be paid in a lump sum upon the signing of the agreement, while another 60 million represents the state’s dividend for 2012, which will be paid to TAIPED by the new owner, and the additional 30 million euros will be paid over the next decade, probably in 10 installments of 3 million euros per annum.

Finance Minister Yannis Stournaras spoke of success in the country’s first big sell-off. He said there are multiple benefits for the state because “investment funds’ confidence in the Greek economy is being proved.” He also stressed his belief that the privatizations program will move ahead with determination in an effort to accelerate the country’s pace as it emerges from the crisis.

TAIPED stated that Emma Delta’s offer amounts to 18.6 times the estimated profits in 2013. “If OPAP wasn’t privatized, the state would collect a dividend for the 2013 financial year of just 13 million euros, and over the next decade it would get no more than 360 million euros, which is about 50 percent of the amount it is getting through the privatization,” the fund said in a statement issued last night.

Meanwhile TAIPED is said to have decided to extend the deadline for the submission of bids for gas companies DEPA and DESFA by another 10 days, to May 20, upon the request of Russian energy giant Gazprom, on the grounds that the Easter holidays bring every corporate move in Russia to a standstill.

While the ECB's refinancing rate cut of 25 bps was very much expected, and just took place pushing the main refi rate to a record low 0.50% (because more liquidity is just what Europe's collapsing economy needs), what was unanticipated was that the Marginal Lending Facility (which last time we checked was used by pretty much nobody) was also cut, from 1.5% to 1.0%. The deposit rate, at 0.00%, was obviously left unchanged.

At today’s meeting, which was held in Bratislava, the Governing Council of the ECB took the following monetary policy decisions:

The interest rate on the main refinancing operations of the Eurosystem will be decreased by 25 basis points to 0.50%, starting from the operation to be settled on 8 May 2013.

The interest rate on the marginal lending facility will be decreased by 50 basis points to 1.00%, with effect from 8 May 2013.

The interest rate on the deposit facility will remain unchanged at 0.00%.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 2.30 p.m. CET today.

Now the question is whether Draghi will engage in non-standard measures to facilitate lending for SMEs. For this, tune in to the press conference in 45 minutes.

The Fed may or may not be able to afford schizophrenia regarding the future of its monetary decisions (for now), but the ECB, in charge of a continent mired deep in depression, does not have that luxury. While consensus overwhelmingly expects a 25 bps cut in the main refinancing rate, some have warned that should the ECB not engage in such a cut, the EUR will tumble as the short covering squeeze ends with a thud. What exactly are the individual banks expecting? The following bulletin from Bloomberg summarizes it all.

Deutsche Bank:

Potential ECB refi rate cut today doesn’t matter much; currency market more sensitive to short-end money market rates and without a deposit-rate cut, today’s decision won’t have a big impact, George Saravelos, strategist at Deutsche Bank, writes in note

Refi rate cut is relevant for European long-end as it encourages carry trades, discourages LTRO pre-payments, caps potential Eonia rise

Morgan Stanley:

If ECB only delivers the expected 25bps cut with no further non-standard measures, it will leave EUR vulnerable, Hans Redeker, strategist at Morgan Stanley, writes in note

Yday’s reaction to Fed statement suggests that delivering within expectations is insufficient to keep asset markets supported

Move below 1.3090 will signal renewed negative trend, suggesting that recent EUR/USD rebound is complete and broader downtrend is resuming

Citigroup:

EUR’s response to ECB decision will depend on type and aggressiveness of measures announced, Valentin Marinov, strategist at Citigroup, writes in note

Easing plans that are too aggressive, or signals of further aggressive easing without detailed SME lending plan, may weigh on EUR; EUR could be supported if ECB cuts rates and unveils concrete proposals to stimulate the lending channel

ECB would have to sound very dovish or deliver a 50bps cut for front-end to rally; look for better entry points than 1% in 3Y1Y receivers, probably in week after ECB

Standard Bank:

Not recommending any new positions today; wise to wait for ECB decision before committing to any new trades, Steven Barrow, strategist at Standard Bank, writes in note

Barclays:

Rate-cut expectations should be fully priced into EUR by now; risks are skewed to EUR strength due to possibility of new non-standard measures and short EUR positioning, Raghav Subbarao, strategist at Barclays, writes in note

Reaction in rates markets likely limited; rates already low and already incorporated expectations of 25bps cut; no rate cut and absence of hints on June reduction will disappoint and fuel volatility at front-end, Giuseppe Maraffino, strategist at Barclays, writes in note

UniCredit:

EUR/USD will benefit if ECB remains on hold (which UniCredit expects), Luca Cazzulani, strategist at UniCredit, writes in note

BNP Paribas:

25bps refi rate cut is fully priced in now and EUR/USD can gain further ground if this scenario is confirmed, Steven Saywell, strategist at BNP, writes in note

Additional measures to boost credit for SMEs may support EUR due to improved risk appetite; a change in inflation language without rate cut should on balance be EUR-supportive

Eonia curve shows 1-mo. OIS already 6bps to Sept.; thus a 25bps refi rate cut is almost fully priced in; little value in bunds at 1.2% and recommend staying short

ING:

House view is ECB will prefer June cut, but Draghi may not want to disappoint market given already fragile sentiment, Chris Turner, strategist at ING, writes in note

Net effect of ECB refi-rate cut may be EUR-supportive; money-market rates already near zero and bigger impact will be on euro-zone banking stocks which will enjoy lower borrowing costs

Lloyds:

Market has shifted away from expecting EUR weakness on ECB refi rate cut; EUR may slump if ECB doesn’t cut refi rate as credit markets will be disappointed

EUR may dip initially on rate cut -- a buying opportunity; strongest positive reaction will likely be EUR/CHF

Too early to expect non-standard measures; Draghi may maintain update commentary

BOTM-UFJ:

Impact of ECB rate cut is likely to be limited with short rates already close to the deposit rate

Negative impact on EUR from rate cut is likely modest as market is already fully expecting a 25bps refi rate cut

RBC:

Expectations for ECB easing have built up significantly; market pricing of policy action today looks somewhat overdone, Norbert Aul, strategist at RBC, writes in client note

Reiterate April 25 recommendation that investors pay 1Y, 2Y-forward Eonia with target of 45bps and stop at 30bps: Aul

Commerzbank:

Risks in ECB policy decision today are balanced toward disappointment, as rate cut is already priced in and new easing measures need to be unveiled to boost markets; enter tactical bund-future shorts

Good morning, and welcome to our rolling coverage of the latest events in the eurozone financial crisis and across the world economy.

Mario Draghi, president of the European Central Bank, takes centre-stage again today as the ECB gathers for its monthly meeting.

With the eurozone economy shrinking, inflation dropping and unemployment at record highs, there's a strong expectation that the ECB will heed the danger signs and cut eurozone interest rates - trimming the main refinancing rate from 0.75% to 0.5%.

But some economists are hoping for more decisive action from Draghi -- such as new measures to stimulate bank lending to Europe's small businesses.

The ECB has decamped to Slovakia, Bratislava for today's meeting. We get the decision at 12.45 BST, but followed by the closely-watched press conference at 1.30pm BST.

We shouldn't pretend that a small cut in interest rates will cure the patient, though.

As Jennifer McKeown of Capital Economics points out:

The possible announcement of policies to stimulate bank lending, particularly to SMEs and in the region’s periphery, might be more helpful.

But even this would leave the ECB lagging behind other central banks.

So, we'll see. I'll be watching the events in Bratislata, along with other developments around the eurozone and beyond....

While Marc Ostwald of Monument Securities reckons the ECB will leave rates unchanged, as it hasn't finished preparing the unconventional measures it wants to deploy alongside it:

The rationale is simple...a rate cut will do nothing to help the distressed peripheral economies (or indeed Germany), given the monetary transmission mechanism remains severely impaired...as such the ECB needs to find some further 'unconventional measures' to try and enhance the efficacy of a refi rate cut, and comments from various ECB officials (above all Constancio and Asmussen) last week made it clear that the process of coming up with such measures is by no means complete.

German manufacturing output stumbles...

Photograph: Markit

Europe's economic downturn has worsened, with manufacturing output sliding to a four-month low in April.

The decline was mainly due to shrinking activity in Germany. But while Europe's biggest economy had a worryingly weak month, there were encouraging signs in Greece (more to follow).

Markit's final manufacturing PMI survey for the eurozone came in at 46.7, which is a slightly more painful contraction than March's 46.8.

Here are the key numbers:

Germany: 48.1, down from March's 49 [anything below 50=shrinking output]

France: 44.4, up from March's 44.0

Italy: 45.5, up from 44.5

Spain: 44.7, up from 44.2

Greece: 45.0, up from 42.1

OECD takes red pen to Italian forecasts

The OECD has given Italian prime minister Enrico Letta a reminder of the challenge he faces, by slashing its economic projections for Italy.

It cut its forecast for Italy 2013 GDP to -1.5% from 1.0% (in line with the IMF's latest projection).

The OECD also hiked Italy 2013 Debt/GDP Forecast To 131.5% from 130.4%, and its 2014 prediction to 134.2% From 132.2%.

Reminder: Greece's austerity package is designed to drag its debt/GDP ratio down to 120% by 2020 -- seen by the IMF as a key measure of debt sustainability.

“Mario, when can you tell me the forms and ways that I can be useful, both officially (Bersani asks me e.g. to interact on the question of vice) and privately. For now it seems to me a miracle! And then miracles exist!”

“Mario, when can you tell me the forms and ways that I can be useful, both officially (Bersani asks me e.g. to interact on the question of vice) and privately. For now it seems to me a miracle! And then miracles exist!”

Lawyer, no economics degree

Lawyer, no economics degree

Poet, no economics degree

Poet, no economics degree

Spook, no economics degree

Spook, no economics degree

Submitted by Tyler Durden on 05/02/2013 07:10 -0400

Submitted by Tyler Durden on 05/02/2013 07:10 -0400

Lawyer, no economics degree

Lawyer, no economics degree Poet, no economics degree

Poet, no economics degree Spook, no economics degree

Spook, no economics degree

No comments:

Post a Comment