The more you try to shut them up, the more they have to say...

Just out from Egan-Jones

4/17/2013: Federal Republic Of Germany: EJR lowered A+ to A (Neg.) (S&P: AAA) (3413Z GR)

Although Germany's credit metrics are respectable, the country has exposure to its banks and the weaker EU members. Deutche Bank has adjusted shareholders' equity to asset near 2% and might need EUR 100B of support. Via the ECB's Target 2, Germany is owed EUR700B of which perhaps 50% is collectible and then there is the banks' southern EMU exposures. Germany's debt to GDP was 80.6% as of 2011. However, increasing Germany's debt by EUR500B raises the adjusted debt to GDP to 100%. The deficit to GDP of .8% is reasonably strong. Unemployment is 6.9% but will probably rise as global economies continue to show weakness. The positive (EUR16.8B) balance of trade (per GFSO) and the positive EUR5.59B current account (per the OECD) help. Inflation has been moderate at 1.4% (per GFSO).

Chancellor Merkel continues to resist calls for EU bonds (shared liabs.) and money printing and is pushing for fiscal controls and the seniority of bailout funding. Germany is likely to be outvoted by other ECB members and therefore will have greater prospective exposure. Watch for the EFSF and the ESM morphing into banks (thereby depressing eventual recoveries) and a rise in the number of euros. Watch progress on the EU banking union. We used the IMF's data for Germany's debt which is greater than Eurostat's data. Downgrading.

While most of the US was in deep REM sleep, the Germany stock index, the DAX, had a flashback to May 2010: starting at 3:44 am EDT, in the span of 6 minutes or much faster than the gradual drop that led to the US flash crash from three years ago, the DAX went from well and solidly-bid to having zero liquidity... and dumping nearly 200 points in the process. Whether it was rumors of a (subsequently validated) rating agency downgrade, or just an algo testing its quote stuffing ability, the moves showed vividly that when the current rosy paradigm shifts abruptly and violently, all those hoping to be the first out of the door and hit the sell button, simply won't be able to do so. Because sadly there is no such thing as a free "4 year long zero volume levitation" - one must always pay the piper in the end.

"Years ago, Mrs Thatcher recognized the truth behind the European Project," UKIP's Nigel Farage reminds his European Parliament 'colleagues', "she saw that it was about taking away democracy from nation states and handing that power to largely unaccountable people." In one of his most wonderfully vitriolic remonstrations, the fiery Farage blasts Europe's leadership, "this European Union is the new communism." Slamming Olli Rehn and his Troika cohorts for "resorting to the level of common criminals and stealing people's money", Farage warns, rather chillingly, that, "it is power without limits. It is creating a tide of human misery and the sooner it is swept away the better." Simply put, he concludes, the European Parliament is living out a federal fantasy which is no longer sustainable.

Full Transcript:

Years ago, Mrs Thatcher recognised the truth behind the European Project. She saw that it was about taking away democracy from nation states and handing that power to largely unaccountable people.

Knowing as she did that the euro would not work she saw that this was a very dangerous design. Now we in UKIP take that same view and I tried over the years in this parliament to predict what the next moves would be as the euro disaster unfolded.

But not even me, in my most pessimistic of speeches would have imagined, Mr Rehn, that you and others in the Troika would resort to the level of common criminals and steal money from peoples' bank accounts in order to keep propped up this total failure that is the euro.

You even tried to take money away from the small investors in direct breach of the promise you made back in 2008.

Well the precedent has been set, and if we look at countries like Spain where business bankruptcies are up 45% year on year, we can see what your plan is to deal with the other bailouts as they come.

I must say, the message this sends out to investors is very loud and clear: Get your money out of the Eurozone before they come for you.

What you have done in Cyprus is you actually sounded the death knell of the euro. Nobody in the international community will have confidence in leaving their money there.

And how ironic to see the Russian prime minister Dmitry Medvedev compare your actions and say, ' I can only compare it to some of the decisions taken by the Soviet authorities.'

And then we have a new German proposal that says that actually what we ought to do is confiscate some of the value of peoples' properties in the southern Mediterranean eurozone states.

This European Union is the new communism. It is power without limits. It is creating a tide of human misery and the sooner it is swept away the better.

But what of this place, what of the parliament? This parliament has the ability to hold the Commission to account. I have put down a motion of censure debate on the table. I wonder whether any of you have the courage to recognise it and to support it. I very much doubt that.

And I am minded that there is a new Mrs Thatcher in Europe and he is called Frits Bolkenstein. And he has said of this parliament - remember he is a former Commissioner: 'It is not representative anymore for the Dutch or European citizen. The European Parliament is living out a federal fantasy which is no longer sustainable.'

That escalated quickly. Germany's DAX is now negative year-to-date (at 5-month lows), Copper is at 18-month lows, the bid for safety has driven 2Y Swiss rates under -10bps, their lowest in 3 months, and US equity markets are crumbling after yesterday's dead-cat-bounce.There was little to no pre-open ramp this morning, no EUR-levered pump, and VIX is not playing ball with the manipulators. Something changed; the denial is beginning to unwind.Gold and silver are modestly bid as we suspect physical demand bleeds back into paper. Maybe stocks are catching down to the 'WTF' reality (as we discussed here and here).

First it was former ECB executive board member Lorenzo Bini-Smaghi saying that "policy makers led by President Mario Draghi will act to weaken the euro" which led to the first shock in the European currency this morning, and now it is Bundesbank head Weidmann, reminding the world that in a monetarist currency war world, he who crushes their currency last, loses. As a result moments ago he said that the ECB may cut rates if new info warrants, something that was actually quite obvious two weeks ago and some 300 pips lower, yet the relentless purchases of Italian bonds by Japanese financials drove the EUR ever higher to its highest level since February yesterday. Net result: time to reacquaint the EUR with gravity.

When the final "bailout" structure of the Cypriot deposit-confiscatory bail-in was revealed in late March, the implied victory for the Troika (which has since notched up its demands for the insolvent country to now sell its 14 tons of gold) was that instead of the deposit haircut passing as a tax, and thus needing a parliament ratification, it would come in the form of a bank resolution, with Laiki bank liquidating and being subsumed by the remaining Bank of Cyprus, and with uninsured depositors in both banks ending up crushed. However, as previously reported, in the interim period deposit outflows have continued and accelerated despite the assorted ineffective "capital controls" which has led to additional underfunding for the local banks, and to a second bailout of Cyprus, this one rising to €23 billion or a 35% increase from the original, as part of which the Troika has demanded that Cyprus sell their gold in the open market. Now, a month later, it appears that the Troika's initial victory may have been a Pyrrhic one, as yesterday the Cypriot attorney general announced, and today the government's spokesman confirmed, that the parliament will have to ratify the €23 billion bailout of the tiny island nation after all, thereby refocusing the popular anger from some ephemeral technocrat in Europe to the country's own elected representatives, thereby changing the calculus of the Cypriot decision by 180 degrees.

Cyprus‘ parliament must ratify a 23-billion-euro (30.3 billion dollar) international bailout deal in order for it to become valid, government spokesman Christos Stylianides said on Wednesday.

"It is not possible that Cyprus‘ bailout deal needs to secure the approval by other parliaments in the eurozone, while at the same time it is not voted on by our parliament," Stylianides told state radio RIK.

"It looks like the parliaments of the other eurozone countries will pass it and we will now see what ours will do. I hope that the legislators will vote with wisdom and responsibility - I have this expectation," he added.

Naturally, since the fate of the country's freedom from the European neo-feudal regime, and potentially the future of the Eurozone itself, is suddenly once again where it never should be: in the democratic hands of the majority of the "great unwashed", the threats of fire and brimstone have started already. Here is Stylianides with his best rendition of Hank Paulson:

"Anyone who is ready to vote against the loan agreement should at the same time be prepared to come up with 10 billion euros needed to continue to pay salaries and pensions."

One word here: Iceland. But we are confident that by now even Cyprus' population, which has stoically absorbed everything from deposit haircuts to the upcoming forced gold sales, is familiar with what the only success story in Europe to date has been, and why.

So what exactly will be voted:

The new vote will cover additional austerity measures drawn up by international creditors - the European Commission, the European Central Bank and the International Monetary Fund (IMF). The measures aim at downsizing the public sector.

EU Economy Commissioner Olli Rehn admitted that "mistakes" had been made "under enormous time pressure" in the initial decision to bail in small depositors, which prompted outrage and was rejected by Cypriot lawmakers.

On the other hand, mistakes were not made when as part of the European Commission's DSA, the following explanation of what is without doubt the immediate future for Cyprus:

In accordance with the Cypriot authorities policy plans, major financial institution will be downsized combined with extensive bail-in of uninsured depositors, and a set of wide-ranging temporary capital controls and administrative measures. The programme is envisaged to build the foundation for sustainable growth over the long run.Nevertheless, in the short run, the economic outlook remains challenging. Real GDP is projected to contract by 12½% cumulatively in 2013-14. Short-run economic activity will be negatively affected by the immediate restructuring of the banking sector, which will impact on net credit growth and by additional fiscal consolidation measures. Temporary restrictions required to safeguard financial stability will hamper international capital flows and reduce business volumes in both domestic and internationally oriented companies. The bail-in of uninsured depositors will cause a loss of wealth, which will reduce private consumption and business investment. This, compounded by the impact of fiscal consolidation already undertaken and new measures agreed, will result in a sharp fall in domestic demand. Little reprieve can be expected from exports amid uncertain external conditions and a shrinking financial service sector.

Cyprus had a choice to say no. It still does: probably its last one. If it once again opts to vote for a fate of Brussels-dominated serfdom, we can wish them is all the best on their uphill climb to a bleak, non-existent, hopeless future.

The vote is expected to take place early next week, unless delayed again. Choose wisely Cyprus.

The levitation that takes place in the early morning hours in the Euro, the incorrect counting of both assets and liabilities, massive losses hidden in securitizations at many central banks including the ECB and the riskiest of assets lined up and labeled "Risk Free" and the bells of St. Rimney's begin to chime. Unemployment at record levels, countries such as Greece, Portugal, and Cyprus that can't pay their bills without Divine interventionand economies that are rapidly shrinking even with the help of Europe's falsified accounting practices.

Ireland is no better, France, Belgium and the Netherlands are in decline and the money created by the ECB is all that separates the Continent from Depression. The problem is, the glue is cracking, stitches are coming apart at the seams and the fantasy that has been created is now day-after-day being shown to be what it actually is; a tragedy of the first order. Every reasonable game that could be played is now an historical footnote. The new games, such as seizing depositors' money in Cyprus, aren't much fun to play.

Spain is an example here; more than 95% of their pension funds are invested in Spanish sovereign debt but 100% is encroaching and the end is nigh. Ireland is running out of cash again. Portugal is out of cash. Cyprus needs about twice as much in loans as admitted. Greece has run up a bill where every new loan pays back the European banks, pays the interest on their debt while the country sinks slowly into the Mediterranean.

The IMF, once thought to be a stalwart institution, has helped to create the fantasy and they have lied and perjured themselves in a shameless fashion. Not one, not one projection for Europe has been anywhere close to the truth and yet they continue to minimize the damage. The IMF has partnered with the Europe and not only turns a blind eye but admits none of their own deceit and so is an accessory to the larceny both before and after the fact.

The investment of money in Europe is now a risk far greater than present yields can justify. Senior debt, subordinated debt, deposits; anything can now be taxed, confiscated or impounded at the direction of Brussels/Berlin. Nothing is safe!

Every scheme in Europe than can be rigged has been or is being rigged and, in the end, it will only be the fools that are left in this game. It is not the greater fools either but the mandated fools who take directions from Brussels who takes their directions from Berlin.

I cannot emphasize enough the great risk that anyone takes now by investing in anything in Europe. You can ignore liabilities, you can play pretend and not count liabilities but in the end they are still there and the losses must be finally acknowledged.

Gold gave you a head's up. The margin calls in gold quickly infected the equity markets and the margin calls in stocks gave you a second head's up. The playing field is shifting and the days of wine and roses are giving way to the days of vinegar and poison ivy.

You got the warning now please try to retain your head before the guillotine of Europe removes it from your neck.

and...

Before asking others to pay, Germany should honour its own debts

By Avraam HadjiGiovannisPublished on April 17, 2013

THE DISPUTE originated in the 1920’s when Germany issued series of bearer bonds in the USA for revitalisation of its economy following the devastating effects of WWI. Acting as trustees, financial institutions such as JP Morgan and Lee Higgins & Co. produced and sold bonds in America raising funds that would be invested in Germany.

These bonds corresponded to Agricultural Loans signed by 14 German banks and guaranteed by the German government. Of these 14 banks four are still active and are part of the troika mechanism.

From 1933, Germany defaulted on interest repayments to Bondholders, as the new Nazi leadership considered the debt that Germany faced following WWI as illegal and issued a moratorium on bonds owed to foreign investors.

In 1952 following years of German debt crisis, the London Debt Agreement restructured Germany’s debt to be sustainable by the agreement of its creditors.

The way this deal would function was to provide the option to the bondholders of German debt, to either accept the repayment terms of the LDA, or to forego attempts to claim their debt until 1993. The rationale being, that you can cash in today from a weak Germany, or wait for a full settlement after 40 years of German growth and development.

Assenting Bondholders: For bondholders who wanted to cash in their bonds immediately, they could receive partial payment, and new bonds, with a discount on the value of their bonds (depending on the issue, between 20% - 60%). For this to be implemented correctly, a procedure of Validation was set up to ensure that anyone presenting bonds for payment, could prove that they were indeed the beneficial owner. This would guarantee that all of the disbursements paid went directly to Germany’s creditors in the correct manor.

Non Assenting Bondholders: For bondholders who chose to wait for full settlement by their next generation in the future, their course of action was to maintain the debt instruments (the bonds) safely, and not request a settlement until the 40-year grace period had expired.

Validation boards were established in the three US states (where the bonds were initially sold) to carry out the compliance requirements for the bondholders who chose to accept the option presented in the LDA. Having performed their role, these boards were subsequently closed a few years later.

By 1993 the German government had succeeded in revitalising its economy and began to respond to requests for payment. Unfortunately, they chose not to honour their debt. To the surprise of many bondholders, Germany would receive payment applications with the physical bonds attached, perforate the bonds, and stamp them as invalid.

The reasons given by the German Government and its subsidiary bodies are: Germany has compiled a list of Bond serial numbers that Germany considers stolen, and hence invalid. The procedure of validation must be complied with.

The German government claims that during WWII Russian soldiers looted the Reichsbank vault, where many bonds were kept, and that these bonds were reintroduced into the market for payment. The simple problem with this claim is that the only bonds that were in the German vault, had already been paid off or pledged, for which there is a public record, and no active bondholders had their bonds physically in Germany. Furthermore, the building which housed the Reichsbank had been completely destroyed, the contents of which had been removed by Germany before the arrival of Russian soldiers to Berlin.

The bonds were “bearer” instruments, and bondholders would cut off the coupons from the papers for their interest repayments. This claim however, was acceptable in the few years immediately following the war, as it was obvious bondholders would not be able to recover their principal or interest at the time, and was the reasons for the Validation Procedure outlined in the London Debt Agreements.

The so-called ‘Validation Procedure’ which was intended to apply to bonds that would be submitted for payment in 1952 added additional security requirements for the bondholder to comply with. Not only was it clear in the legislation that this only applied to Assenting Bondholders in 1952, subsequently indicated by the closure of the Validation boards, but it would be simply impossible for any bondholder to comply with them 40 years later.

When bondholders and creditors have asked to see this list, the German government categorically denied access, stating that it is not in their national interest, and has classified this list as a “national secret”.

What followed was a series of lawsuits in the US where German legal defence has never denied the liability for its debt, but has systematically used technical issues and delayed court cases, to the point that many bondholders have paid millions more in legal expenses. Many of these claims continue today, by some of the surviving bondholders, and the acquirers of that debt, and will be making appeals to the European Courts in the near future.

There is no question in the minds of the many experts in banking and law, with substantial knowledge of international financial instruments, that these bonds represent unpaid debt of the German government and its subsidiary bodies.

We, as a Cypriot company, have spent much time and resources acquiring, not only the bonds, but the wall of evidence surrounding the sovereign and national debt of Germany and the impressive ability of a great state to escape its obligations. For over three generations the same sovereign debt has been postponed and avoided. The inheritors and purchasers of this debt have been obliged to adopt expensive and cumbersome avenues, to force the German government's hand to respect and honour its obligations, a fundamental of our modern European society.

German economic historian Albrecht Ritschl argued in an interview with Spiegel in 2011 that Germany was ‘the biggest debt transgressor of the 20th century’. “During the 20th century, Germany was responsible for what were the biggest national bankruptcies in recent history. It is only thanks to the United States, which sacrificed vast amounts of money after both World War I and World War II, that Germany is financially stable today and holds the status of Europe's headmaster. That fact, unfortunately, often seems to be forgotten,” he said.

The undeniable truth is that authenticated bank bearer bonds worth $9,750,000,000, that’s nine billion seven hundred and fifty million US dollars according to the gold price of today, owned by a Cypriot company, issued on the back of German sovereign debt that remains unsettled.

THE PRESIDENT of the European Central Bank Mario Draghi was quick to come to the defence of Cyprus’ Central Bank Governor Panicos Demetriades. In a letter sent to President Nicos Anastasiades, Draghi warned that the Governor could only be dismissed on the grounds specified by EU law and even then the action would have to be reviewed by the EU’s court of justice.

Anastasiades responded with a six-page letter, denying that any proceedings for the sacking of Demetriades had been undertaken but also listing some of the dubious policies implemented by him since he was appointed by the Christofias government last May. Demetriades’ has been responsible for many ill-conceived decisions that caused harm to the country, but his decision to carry on providing emergency liquidity assistance to the insolvent Laiki Bank was catastrophic and could be described as criminally negligent.

Should a Governor whose appallingly poor judgment has cost us billions, be kept in his position to cause more harm to the country because he has the support of the ECB president? And was Draghi not concerned that Cyprus has a Governor who was taking billions of ELA for an insolvent bank, without receiving adequate security from it, building up a debt in excess of €9.2 billion? Obviously not, as the ECB has arbitrarily passed on this debt to the Bank of Cyprus and demanded additional collateral from it to cover Demetriades’ blunders. We would have thought the ECB would have wanted him out, instead of standing by him and issuing warnings to the government.

Demetriades has also tried to turn opinion abroad against the government telling Bloomberg that the Governor’s independence was under attack. He told the news agency that there had been “constant interference in relation to the management of the banks under resolution,” which was a bit rich, considering how Demetriades had obeyed all the diktats of Christofias government without ever complaining that the Governor’s independence was being undermined. He publicly admitted that he carried on sanctioning ELA for Laiki because the previous government wanted any decision on the bank to wait until after the elections.

The Anastasiades government has been absolutely right to interfere for the very simple reason that the Governor has shown he cannot be trusted to take decisions that are in the best interest of the country. Was it not Demetriades who wanted to re-open the banks on the Tuesday after the first Eurogroup meeting? If the government had not prevented him from doing so there would have been a bank run that would have made things even worse.

Of course it should be said that he was merely following the instructions of the ECB, which, as Demetriades pointed out a couple of weeks ago, has full confidence in the Governor. President Anastasiades has every right to have no trust or confidence in a man who acts as the ECB’s loyal agent, because as events have shown the last thing the ECB is interested in is the good of the Cyprus economy.

Eight in 10 Greeks want government to pursue Germany over WWII reparation claims

Eight in 10 Greeks believe the government should pursue Germany over the outstanding issue of Second World War reparations, according to a new opinion poll.

The survey carried out by Marc for Alpha TV found that almost 90 percent of respondents felt that Greece should seek damages from Germany.

The German government has played down the issue but the Greek Foreign Ministry insisted last week that Athens does not consider the matter to have been settled.

A Finance Ministry committee has been investigating whether Greece has a rightful claim to receive money from Germany but the results of its prove have been kept secret.

A recent report in To Vima suggested that Greece’s claim amounted to as much as 162 billion euros after interest had been added. This relates to reparations for infrastructure and personal damage as well as the repayment of a loan Greece was forced to provide to the Nazi regime.

The March poll also found that more than 40 percent of Greeks think that Greece should leave the euro if it cannot improve the terms of its bailout agreement.

In terms of political ratings, the survey put SYRIZA narrowly ahead of New Democracy. The leftists garnered 22.3 percent, the conservatives 22.1 percent.

Golden Dawn was third with 9.7 percent, followed by Independent Greeks with 5.9 and PASOK with 5.4. Democratic Left gathered 4.4 percent.

Final bids for 33pct stake in Greek gambling monopoly OPAP due by Wednesday afternoon

The period during which investors can express an interest in acquiring a 33 percent stake in Greek state gambling monopoly OPAP expires on Wednesday afternoon.

It is thought that at least three investors will submit final bids after eight suitors initially expressed interest.

The government is looking to raise more than 650 million euros from the sale as part of its plan to raise 11 billion euros from privatizations by 2016.

It is the first major sell-off undertaken by the coalition since it was formed after the June elections last year.

Two of the eight initial suitors for the 33 percent stake wrote last month to OPAP and the Greek privatisation agency HRADF complaining the process is not being run in a transparent and objective way.

In what may be a first in at least 3-4 months, instead of the usual levitating grind higher on no news and merely ongoing USD carry, tonight for the first time in a long time, futures have drifted downward, pushed partially by declining funding carry pairs EURUSD and USDJPY without a clear catalyst. There was no explicit macro news to prompt the overnight weakness, although a German 10 year auction pricing at a record low yield of 1.28% about an hour ago did not help. Perhaps the catalyst was a statement by the Chinese sovereign wealth fund's Jin who said that the "CIC is worried about US, EU and Japan quantitative easing" - although despite this and despite the reported default of yet another corporate bond by LDK Solar, the second such default after Suntech Power which means the Chinese corporate bond bubble is set to burst, the SHCOMP was down only 1 point. The Nikkei rebounded after strong losses on Monday but that was only in sympathy with the US price action even as the USDJPY declined throughout the session.

Regarding China, the FT reports that a senior Chinese auditor and vice-chairman of China’s accounting association has described the local government debt situation in the country as “out of control”. The comment comes after the recent warnings from Fitch and Moody’s about the risks of China’s local government debt. The auditor says his firm has stopped signing off on bond sales by local governments as “most don’t have very strong debt servicing abilities”. Keep a close eye on China which for the bast 4 years has been abnormally quiet. Once this region too blows up, all bets are off, as China will be the true black swan, which everyone sees, but nobody expects the local communist government can ever lose control of the situation. That may not be the case for much longer.

Curiously, gold has outperformed equities for the first time in day, with the spot price trading above $1380 at last check on news of frantic physical buying in India, Australia, the US mint (which sold a massive 33,000 oz of gold on April 16) and across precious metal vendors in the US, which shows demand for physical gold and silver has hardly popped.

Somewhat facilitating this increase was the Shanghai Gold Exchange which once again lowered margin requirements for gold and silver to 10% and 13% respectively after Monday's hike.

In other news, we learned from the Cypriot finance minister that the country's gold sale was a Troika mandated decision, as most had known by now, and that the local central bank must and will ratify the decision in the next few months. How this disposition of gold will happen without a parliamentary vote is not exactly clear.

Finally, it is worth noting that just like in 2011, Goldman's Jan Hatzius, so bullish entering 2013, is finally starting to throw in the towel. We will report on that in a later post.

SocGen provides a quick and dirty recap on the recent inverse correlation between the surge in gold vol and equities, which appear to have been forcibly broken compared to previous instances:

A sense of calm returned to metals markets yesterday as investors grappled with the brutal jump in volatility and subsequent (marginal) pullback in an attempt to establish whether the liquidation has run its course or has further to run. After jumping from 14.47 on Friday to a 35.39 high on Monday, 30-day volatility of CBOE gold ETF fell back to 30.44. A similar run-up in volatility occurred in the summer of 2011, but took place over several weeks compared to the massive lurch of the last three days. It then took over four months for it to normalise. Whether we are in the throes of something similar today is impossible to tell as we still try to establish why the stampede occurred in the first place. Talk of gold selling by Cyprus as a means to raise bailout funds is said to have initiated the move, but what followed had nothing to do with what's happening in Nicosia. Nor is the price action justified by radical change in inflation expectations, or covering up of long equity trades that went sour. US core CPI was reported to have slowed to 1.9% in March and the Fed's 5y forward breakeven inflation rate has been hovering at just above 2.70%. The S&P snapped a two-day losing run yesterday and trades within 2% of last Friday's close. This pales with the corrective price action of 2011 and even with that of summer 2012.

The full overnight recap from DB's Jim Reid

Gold rebounded (+1.4%) a bit yesterday and the wider commodity complex recouped some of the losses of the previous sessions. Copper, natural gas and silver rallied 1%, 0.6% and 2.8% respectively, but Brent remained under some pressure (-0.72%) as it hovered near 9 month lows. The S&P500 (+1.4%) managed to recover most of its Monday losses buoyed by Goldman Sachs, Coca-cola and Johnson & Johnson who all reported better than expected results on both the top and bottom line. More broadly yesterday saw nine out of 12 companies report EPS ahead of consensus, although only half managed to beat revenue estimates. We’ll provide a more comprehensive earnings season tracker later this week as more companies report. Yesterday’s gains were broadbased with all but 39 stocks in the S&P500 finishing higher on the day and all ten industry sectors trading firmer. A number of security scares at Boston’s Logan airport, various New York airports and New York City itself failed to significantly dampen the trading pattern in equities. In credit markets, the CDX IG index finished 4bp firmer, essentially erasing the widening seen on Monday. The European Crossover and IG indices were basically unchanged, outperforming the weakness seen in European equities that saw the Stoxx600 close 0.8% lower. The Euro continued to gain on the USD, adding 1.1% yesterday in its strongest one day gain in a month.

Yesterday also saw some decent data out of the US, headlined by the strong housing starts (+1036k vs +930k expected) in March, after a 51k upward revision to the prior month. Housing starts managed to print at the highest annualised rate since mid-2008. Industrial production for March also surprised to the upside (+0.4% vs +0.2%) though mostly driven by an increase in utilities production from the unseasonably cold weather last month. On a less positive note, building permits were marginally below expectations at 902k (vs 942k expected). On the inflation side, headline CPI dropped to -0.2% (vs 0% expected) in March off the back of the recent volatility in energy prices which fell -2.6% in the month. As a result, the year-on-year rate of change in the headline dipped to +1.5% from +2.0% in the previous month. Core CPI rose +0.1% (vs. +0.2% previous and expected). DB’s US economists have upgraded their Q1 GDP growth estimate to +3.4% following yesterday’s data which suggested higher inflation-adjusted output last quarter than expected.

Aside from the data there was a fair amount of Fedspeak yesterday which on balance was tilted to the more dovish side. Fed Vice Chair Janet Yellen said she favours holding rates “lower for longer”. She also said that there was no “pervasive evidence of rapid credit growth” but that there are signs that some parties are reaching for yield which the Fed is monitoring carefully.

Interestingly, Yellen said the Fed “has not taken off the table” that it might have to react to an asset bubble. Elsewhere, the NY Fed’s Bill Dudley suggested that the labour market had yet to show substantial improvement – a view which was shared by the Minneapolis Fed’s Kocherlakota who advocated a 5.5% unemployment threshold for the Fed to tighten policy.

Turning to overnight markets, Asian equities are trading with gains on the back of the positive close in the US. Gains are being led by the Nikkei (+0.9%) which has been helped by the 0.75% depreciation in the yen against the greenback. The KOSPI (-0.1%) is underperforming after news that North Korea has rejected South Korean business owner’s requests to visit the Gaeseong joint industrial zone. North Korea said that talks with the US are possible once it has sufficient nuclear deterrents to ward off an attack (Bloomberg). There is solid buying in Asian bonds with cash and synthetic credit about 2-3bp tighter overnight.

Staying in the region, the FT reports that a senior Chinese auditor and vicechairman of China’s accounting association has described the local government debt situation in the country as “out of control”. The comment comes after the recent warnings from Fitch and Moody’s about the risks of China’s local government debt. The auditor says his firm has stopped signing off on bond sales by local governments as “most don’t have very strong debt servicing abilities”. On a related note, there has been some focus on Chinese corporate defaults after Chinese solar company, LDK Solar, reportedly defaulted on a bond on Monday. This follows last month’s default of its peer Suntech Power, which was once the world’s largest solar-panel maker by capacity.

It will be a relatively quiet day ahead for data both in Europe and the US. The minutes from the BoE’s last meeting are due as is the latest UK employment report. The Fed publishes its Beige Book. Companies scheduled to report earnings today include Bank of America, eBay, American Express and Tesco.

Strong demand for German debt usually indicates traders are pushing their money into "safe havens".

MEPs criticise Commission over botched Cyprus bailout.

The European Parliament is holding a session on the Cyprus bailout this morning - it's being streamed here (although the link is a little flaky).

The MEPs want to find out how the Cypriot rescue plan was so badly handled.

The session began with UKIP's Nigel Farage savaging the decision to force losses on depositors in Cyprus, before Sharon Bowles (who chairs the Economic and Monetary Affairs Committee), also laid into commissioner Olli Rehn.

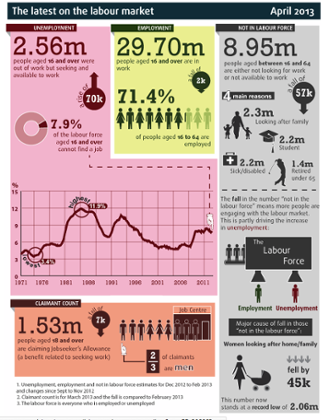

UK unemployment rate rises to 7.9%

Unemployment in the UK has jumped, in a sign that Britain's economy remains worryingly weak .

The number of people out of work in Britain rose by 70,000 in the three months to February, compared to the previous quarter. That pushed the jobless rate up to 7.9%, from 7.8% last month, to its highest level since last summer.

Youth unemployment rose by 20,000 to 979,000, as young people continues to face the brunt of the troubles in the economy.

There was also a nasty slump in wages. Total pay rose by just 0.8%, year-on-year, in the three months to February. With inflation at 2.8%, that means real wages kept shrinking.

The only good news was a 7,000 drop in the claimant count, in March.

Cyprus to decide on gold sale soon

Cyprus's finance minister has declared that the country will probably decide to start selling some of its gold reserves to help fund its bailout programme "in the coming months".

Haris Georgiades also told Bloomberg that the country's central bank will have to make the decision. This adds another potential complication to the sale, as governor Panicos Demetriades (under fire for his own handling of the crisis) has said he hasn't even been consulted about the plan.

Georgiades told Bloomberg:

The exact details of it will be formulated in due course primarily by the board of the central bank...Obviously it’s a big decision.

News that Cyprus would sell €400m of gold broke last week, when the details of the European Commission's debt sustainability report on the country leaked.

Cyprus holds around 13.9 metric tonnes of gold, which was worth around $760m (€580m) last week. Its value has now dropped to $670m (€508m) following the plunge in the gold price.

Some analysts have suggested that Cyprus's planned gold sale helped to puncture the gold price. Georgiades commented:

I’m not really sure if the series of events is exactly matching with the recent movements in the price of gold, but I suspect maybe it was a contributing factor.

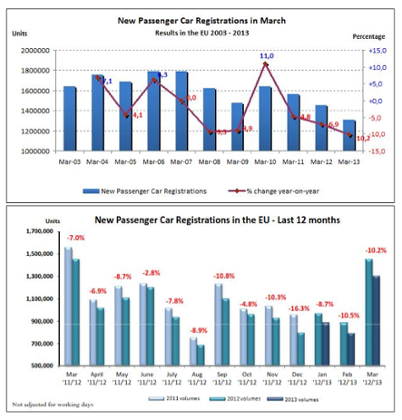

It's another bleak morning for Europe's carmakers. New figures show that sales across the region tumbled by 10.2% in March, led by a slump in sales in Germany.

This proved seriously bad news for the region's carmakers, who saw their own sales slump again.

The Association of European Carmakers reported that last month:

Italy: -4.9% year-on-year

Spain: -13.9% year-on-year

France: -16.2% year-on-year

Germany: -17.1% year-on-year

The UK, though, continues to defy the downturn, with sales rising 5.9% last month.

Denand for new passenger cars across the EU has now fallen for the last 18 months. These graphs suggest that the downturn is actually picking up pace.

Photograph: Association of European Carmakers

Today's data underlines the link between consumer spending and manufacturing. With austerity-hit European customers spending, many of the region's carmakers suffered deep sales falls last month.

The decline in sales makes those recovery plans even tougher -- Reuters reckons we could see profits warnings from some of the major players in the months ahead.

With the International Monetary Fund warning yesterday that the eurozone will shrink by 0.3% this year, Europe's economic woes remain very worrying.

We'll be hearing more from the IMF today, as its Spring Conference continues in Washington. There's also the latest Bank of England minutes, UK unemployment data, and a debate in the European Parliament on Cyprus coming up.

Submitted by Tyler Durden on 04/17/2013 15:41 -0400

Submitted by Tyler Durden on 04/17/2013 15:41 -0400

No comments:

Post a Comment