Commentary on the economic , geopolitical and simply fascinating things going on. Served occasionally with a side of snark.

Monday, March 11, 2013

Morning news - focus on Europe ( Greece , Italy at the forefront) , Might Christine Lagarde be forced to step down from her perch at the IMF ? Weekend data from china - inflation running to hot , industrial production slipping , retail sales slipping ......

THE ROVING EYE The Fall of the House of Europe By Pepe Escobar

The Enchanters came / Cold and old, Making day gray / And the age of gold Passed away, / For men fell Under their spell, / Were doomed to gloom. Joy fled, / There came instead, Grief, unbelief, / Lies, sighs, Lust, mistrust, / Guile, bile, Hearts grew unkind, / Minds blind, Glum and numb, / Without hope or scope. There was hate between states, A life of strife, / Gaols and wails, Dont's, wont's, / Chants, shants, No face with grace, / None glad, all sad. W H Auden, The Golden Age

We have, unfortunately, no post-modern version of Dante guidedby Virgil to tell a startled world what is really happening in Europe in the wake of the recent Italian general election. On the surface, Italians voted an overwhelming "No" - against austerity (imposed the German way); against more taxes; against budget cuts in theory designed to save the euro. In the words of the center-left mayor of Florence, Matteo Renzi, "Our citizens have spoken loud and clear but maybe their message has not been fully grasped." In fact it was.

There are four main characters in this morality/existential play worthy of the wackiest tradition of commedia dell 'arte.

The Pyrrhic winner is Pier Luigi Bersani, the leader of the center-left coalition; yet he is unable to form a government. The undisputed loser is former Goldman Sachs technocrat and caretaker Prime Minister Mario Monti.

And then there are the actual winners; "two clowns" - at least from a German point of view and also the City of London's, via The Economist. The "clowns" are maverick comedian Beppe Grillo's 5 Star movement; and notorious billionaire and former prime minister Silvio "Bunga Bunga" Berlusconi.

To muddle things even further, Berlusconi was sentenced to one year in prison last Thursday by a Milan court over a wiretapping scandal. He will appeal; and as he was charged and convicted before, once again he will walk. His mantra remains the same: ''I'm 'persecuted' by the Italian judiciary.''

There's more, much more. These four characters - Bersani, Monti, Grillo, Berlusconi - happen to be at the heart of a larger than life Shakespearean tragedy: the political failure of the troika (European Commission, European Central Bank and International Monetary Fund), which translates into the politics of the European Union being smashed to pieces.

That's what happens when the EU project was never about a political ''union'' - but essentially about the euro as a common currency. No wonder the most important mechanism of European unification is the European Central Bank. Yet abandon all hope of European politicians asking their disgruntled citizens about a real European union. Does anybody still want it? And exactly under what format?

Meet Absurdistan Why things happened in Italy the way they did? There is scarcely a better explanation than Marco Cattaneo's, expressed in this blog where he tries to understand ''Absurdistan''.

It all started with an electoral law that even in Italy was defined as ulna porcata (a load of rubbish), validating a ''disproportional'' system (political scientists, take note) that could only lead to an ungovernable situation.

In Cattaneo's matchless depiction, in the Senate the One for All, All For One coalition (Bersani's) got 31.6% of the votes. The Everyone for Himself coalition (Berlusconi's) got 30.7%. And the brand new One Equals One All the Others Equal No One movement (Grillo's) got a surprising 23.8%.

And yet, defying all logic, in the end Everyone for Himself got 116 seats, One for All, All for One got 113 seats, and One Equals One All the Others Equal No One got only 54 - less than half.

At street level, from Naples to Turin and from Rome to Palermo, there's a parallel explanation. No less than 45% of Italians, from retired civil servants living on 1,000 euros (US$1,300) a month to bankers making 10 million euros a year, don't want any change at all. Another 45% - the unemployed, the underpaid - want radical change. And 10% don't care - ever. Add that to the ungovernability lasagna.

And extract from it a nugget of cappuccino-at-the-counter wisdom. Absurdistan's finances will soon be in a state as dire as Hellenistan - those neighborly descendants of Plato and Aristotle. And then Absurdistan will become a model to Europe and the world - where 1% of the population will control 99% of the national wealth. From Lorenzo de Medici to Berlusconi; talk about Decline and Fall.

Bunga Bunga me baby Tried to death (including being convicted for tax fraud in October 2012; he walked); beneficiary of dodgy laws explicitly designed to protect himself and his enormous businesses empire; the Rabelaisian Bunga Bunga saga. He beat them all (so far). Silvio Berlusconi may be the ultimate comeback kid. How did he pull it off this time?

It's easy when you mix a billionaire's media wattage (and corporate control) with outlandish promises - such as scrapping a much-detested property tax. How to make up for the shortfall? Simple: Silvio promised new taxes on gambling, and a shady deal to recover some of the funds held by Italians in Swiss banks.

Does it matter that Switzerland made it clear it would take years for this scheme to work? Of course not. Even Silvio's vast opposition was forced to admit the idea was a ''stroke of genius''. Nearly 25% of Italians voted for Silvio's party. Nearly a third backed his right-wing coalition. In Lombardy - informally known as the Italian Texas - the coalition smashed the center-left to pieces; Tuscany on the other hand voted traditionally left, while Rome is a quintessential swing city.

Silvio's voters are essentially owners of small and medium-sized businesses; the northern Italy that drives the economy. They are all tax-crazy; that ranges from legions of tax evaders to those who are being asphyxiated by the burden. Obviously, they couldn't care less about Rome's budget deficits. And they all think German Chancellor Angela Merkel should rot in Dante's ninth circle of hell.

Frau Merkel, for her part, had been entertaining the idea of quietly cruising the eurozone waters towards her third term in the coming September elections. Fat chance - now thanks to Silvio's and Beppe Grillo's voters. Talk about a North-South abyss in Europe. The EU summit this month is going to be - literally - a riot.

Those sexy polit-clowns All hell is breaking loose in the EU. Le Monde insists Europe is not in agony. Oh yes, it is; in a coma.

And yet Brussels (the bureaucrat-infested European Commission) and Berlin (the German government) simply don't care about a Plan B; it's austerity or bust. Predictably, Dutch Finance Minister Jeroen Dijsselbloem - the new head of the spectacularly non-transparent political committee that runs the euro - said that what Monti was doing (and was roundly rejected by Italians) is ''crucial for the entire eurozone''.

In 2012, Italy's economy shrank 2.2%, more than 100,000 small businesses went bust (yes, they all voted for Silvio), and unemployment is above 10% (in reality, over 15%). Italy may have the highest national debt in the eurozone after Greece. But here Absurdistan manifests itself once again via austerity; Italy's fiscal deficit is much lower than France's and Holland's.

Pop up the champagne; France is in vertical decadence. It's not only the industrial decline but also the perennial recession, social turbulence and public debt beyond 90% of GDP. France, the second-largest eurozone economy, asked the European Commission for an extra year to lower its deficit below 3% of GDP. Jens Weidman, president of the Bundesbank, roared ''Forget it''.

Portugal is also asking the troika for some room. Portugal's economy is shrinking (by 2%) for the third year running, with unemployment at over 17%.

Spain is mired in a horrendous recession, also under a monster debt crisis. GDP fell 0.7% in 2012 and according to Citibank will fall a further 2.2% this year. Unemployment is at an overwhelming 26%, with youth unemployment over 50%. Not everyone can hit the lottery playing for Barcelona or Real Madrid. Ireland has the eurozone's highest deficit, at 8%, and has just restructured the debt of its banks.

Greece is in its fifth recession year in a row, with unemployment over 30% - and this after two austerity packages. Athens is running around in circles trying to fend off its creditors while at least trying to alleviate some of the draconian cuts. Greeks are adamant; the situation is worse than Argentina in 2001. And remember, Argentina defaulted.

Even Holland is under a serious banking crisis. And to top it off, David Cameron has thrown Britain's future in Europe in turmoil.

So once again it was Silvio's turn - who else? - to spice it all up. Only the Cavaliere could boom out that the famous spread - the difference between how much Italy and Germany pay to borrow on the bond markets - had been ''invented'' in 2011 by Berlin (the German government) and Frankfurt (the European Central Bank), so they could get rid of himself, Silvio, and ''elect'' the technocrat Monti.

German media, also predictably, has been taking no prisoners with relish. Italy and Italians are being routinely derided as ''childlike'', ''ungovernable'', ''a major risk to the eurozone''. (See, for example, Der Spiegel.)

The ultra-popular tabloid Bild even came up with a new pizza; not a Quattro Stagioni (Four Seasons) but a Quattro Stagnazioni (Four Stagnations).

The verdict is of an Italy ''in the hands of polit-clowns that may shatter the euro or force the country to exit''. Even the liberal-progressive Der Tagesspiegel in Berlin defines Italy as ''a danger to Europe''.

Peer Steinbruck, Germany's former finance minister and the Social Democratic candidate against Merkel next September, summed it all up: "To a certain degree, I am horrified that two clowns won the election."

So whatever government emerges in Italy, the message from Brussels, Berlin and Frankfurt remains the same: if you don't cut, cut and cut, you're on your own.

Germany, for its part, has only a plan A. It spells out ''Forget the Club Med''. This means closer integration with Eastern Europe (and further on down the road, Turkey). A free trade deal with the US. And more business with Russia - energy is key - and the BRICS in general. Whatever the public spin, the fact is German think-tanks are already gaming a dual-track eurozone.

The people want quantitative easing This aptly titled movie, Girlfriend in a Coma, directed by Annalisa Piras and co-written by former editor of The Economist Bill Emmett, did try to make sense of Italy's vices and virtues.

And still, not only via Prada or Maserati, Parma ham or Brunello wines, Italy keeps delivering flashes of brilliance; the best app in the world - Atom, which allows the personalization of functions on a mobile phone even if one is not a computer programmer - was created by four 20-somethings in Rome, as Republicreported.

Philosopher Franco Berardi - who way back in the 1970s was part of the Italian autonomous movements - correctly evaluates that what Europe is living today is a direct consequence of the 1990s, when financial capital hijacked the European model and calcified it under neoliberalism.

Subsequently, a detailed case can be made that the financial Masters of the Universe used the aftermath of the 2008 financial crisis to turbo-charge the political disintegration of the EU via a tsunami of salary cuts, job precariousness for the young, the flattening of pensions and hardcore privatization of everything. No wonder roughly 75% of Italians ended up saying ''No'' to Monti and Merkel.

The bottom line is that Europeans - from Club Med countries to some northern economies - are fed up of having to pay the debt accumulated by the financial system.

Grillo's movement per se - even capturing 8.7 million votes - is obviously not capable of governing Italy. Some of its (vague) ideas have enormous appeal among the younger generations especially an unilateral default on public debt (look at the examples of Argentina, Iceland and Russia), the nationalization of banks, and a certified, guaranteed ''citizenship'' income for everyone of 1,000 euros a month. And then there would be referendum after referendum on free-trade agreements, membership of the North Atlantic Treaty Organization and, of course, to stay or not stay within the eurozone.

What Grillo's movement has already done is to show how ungovernable Europe is under the Monti-Merkel austerity mantra. Now the ball is in the European financial elite's court. Most wouldn't mind letting Italy become the new Greece.

So we go back full circle. The only way out would be a political reformulation of the EU. As it is, most of Europe is watching, impotently, the death of the welfare state, sacrificed in the altar of Recession. And that runs parallel to Europe slouching towards global irrelevance - Real Madrid and Bayern Munich notwithstanding.

The Fall of the House of Europe might turn into a horror story beyond anything imagined by Poe - displaying elements of (already visible) fascism, neo-Dickensian worker exploitation and a wide-ranging social, civil war. In this context, the slow reconstruction of a socially based Europe may become no more than a pipe dream.

What would Dante make of it? The great Roberto Benigni, a native of Tuscany, is currently reading and commenting on in depth 12 cantos - from the XI to the XXII - in Dante's Inferno, a highlight of the Divine Comedy. Spellbound, I watched it on RAI - the square in front of the fabulous Santa Croce church in Florence packed to the rafters, the cosmic perfection of the Maestro's words making sense of it all.

If only his spirit would enlighten Inferno dwellers from Monti to Merkel, from Silvio to European Central bankers - aligning Man once again with the stars and showing troubled Europe the way.

There have been waves of threats by Eurozone politicians to bully people into accepting “whatever it takes” to keep the shaky construct of the monetary union glued together. These threats peaked last year with disorderly default, and when that wasn’t enough, with thecollapse of the Eurozone. But now, the ultimate threat has been pronounced: war.

It wasn’t an idle thought by a wayward parliamentarian on the radical fringe but a well-articulated statement by Luxembourg Prime Minister Jean-Claude Juncker who was, until January, the President of the Eurogroup that manages the political aspects of the euro. And he’d picked Europe’s largest magazine, Der Spiegel, to make it (excerpts here, rest behind pay wall; update March 11: Der Spiegel's own translation into English just came out here).

He’d alluded to it before. Last August, as he was jabbering about Greece’s potential exit from the Eurozone, he lamented that “many Germans and the German media” talked about Greece as if it were “a people you couldn’t respect,” and that Greeks depicted Chancellor Angela Merkel as if she were “the heiress of the Nazis.” And then his big threat, albeit in veiled form: “What we thought had been buried long ago, very quickly rises again.”

His problem: the halting integration of Europe. European countries were small, but there was a solution. “We must show the world something giant, and that’s the euro,” he said. He wanted Europeans to integrate more closely. And not just within the EU, but “the total continent, with extensions”—so maybe Turkey. They’d all eventually use the euro. And if it didn’t work out....

That was last year. Now, given the Italian election, he made it explicit. “For my generation, the common currency has always been a policy of peace,” he said. He was worried that people were getting lost in national naval gazing. “Those who believe that the eternal question of war and peace in Europe would never reappear could be seriously mistaken,” he said. “The demons aren’t gone; they’re only sleeping, as the wars in Bosnia and Kosovo have shown.”

The possibility of war—unless the euro survived and became the currency of the entire EU.

He was struck by the realization how much the European conditions resembled those of 1913, on the eve of World War I. But then, after having thrown “war” on the table, he backed off; he didn’t believe that Europe was facing armed conflicts, but he saw “conspicuous parallels.” In 1913, the prevailing wisdom was that there could never be another war in Europe because the powers on the continent were economically so interwoven that they couldn’t afford it, he said. “Particularly in Western and Northern Europe, there reigned a complacency that assumed that peace had been secured forever.”

By 2050, Europe would have about 7% of the world population, he said. In order to remain relevant, it would have to be united. The heads of the governments in Germany, France, and Great Britain knew that their voices were heard internationally only because they were speaking through the “megaphone” of the EU.

And the EU’s destiny was the euro. He listed proudly the “serious reforms” that had been carried out, like keeping Greece in the Eurozone—regardless of what that did to the Greeks whose belts had been tightened by five notches, or what it did to their economy that would be downgraded to “developing nation” effective June 2013. He praised the bailout funds and the European banking union—regardless of how they’d use taxpayers in some countries to bail out banks and their investors in others.

But hadn’t the elections in Italy shown that Southern Europeans weren’t all that enthusiastic about his glorious plans? Hadn’t Italian voters just demolished Prime Minister Mario Monti and his pro-euro course of reforms and austerity? It didn’t matter. Abandoning the austerity policies “would be a big mistake,” he explained. Politicians shouldn’t promote the “wrong policies” just because they were afraid they’d lose the next election. “If you want to govern, you must take responsibility for your country and Europe overall. And that means: you must implement the correct policies even if many voters find them wrong.”

A curious understanding of democracy. One fraught with peril. But one that has become all too common in the Eurozone where the will of the people has consistently been trampled into the ground. To make his message more persuasive, to get politicians to toe the line, to get taxpayers in financially stable countries to give up resisting the transnational wealth transfers, and to get the people in crisis countries to swallow without demur the bitter pills of his reform programs, he’d added what has become the ultimate threat in the euro bailout and austerity racket—the possibility of war.

But there may be complications. The ECB and the national central banks of the Eurozone set out to collect information on household wealth. A massive bureaucratic undertaking. Results are now ready. No one in Europe had ever done a survey on that scale before. And no one might ever do it again. Because the results are so explosive that the Bundesbank is keeping its report secret—and word has leaked out why. Read.... A “Politically Explosive” Secret: Italians Are Over Twice As Wealthy As Germans

A new party led by economists, jurists, and Christian Democrat rebels will kick off this week, calling for the break-up of monetary union before it can do any more damage.

"An end to this euro," is the first line on the webpage of Alternative für Deutschland (AfD). "The introduction of the euro has proved to be a fatal mistake, that threatens the welfare of us all. The old parties are used up. They stubbornly refuse to admit their mistakes."

They propose German withdrawl from EMU and return to the D-Mark, or a breakaway currency with the Dutch, Austrians, Finns, and like-minded nations. The French are not among them. The borders run along the ancient line of cleavage dividing Latins from Germanic tribes.

The plans draw on work by Hans-Olaf Henkel, former head of Germany'sindustry federation (BDI) and a chastened europhile -- the "worst error of my professional life", he told me.

The appeal of German exit is obvious. It is the least traumatic way to end the 20pc to 30pc misalignment between North and South, the cancer eating Europe. Club Med keeps the euro. It enjoys instant devaluation, while still able to uphold euro debt contracts. The spectre of sovereign defaults recedes.

The party hopes to contest the federal elections in September, winning enough votes to scramble a tight race. Chancellor Angela Merkel suddenly has a "UKIP problem" on the her right flank.

Should she sign off on a bail-out out for Cyprus -- safeguarding the "dirty funds of Russian oligarchs", as the AfD puts it -- she will be raked by heavy fire.

That will test her solidarity mantra, and she can turn on a Pfennig. She ditched her nuclear energy policy days after surveying the post-Fukushima polls.

Nobody knows how much support AfD could command. Protest parties usually flop in Germany, but the Free Voters won 10pc in Bavaria in 2008 on a Right-leaning, eurosceptic ticket, and there have never been circumstances quite like this before.

The slide towards fiscal union is a constitutional revolution. It erodes the budgetary supremacy of the Bundestag and threatens to eviscerate Germany's vibrant post-war democracy. Large matters.

The AfD leader Bernd Lucke says Beppe Grillo's threat to default on Italy's external debt has demolished claims that Germany's rescue pledges will never be called.

"The Italian election shows how dangerous the whole euro crisis really is. Whether countries can and will pay back their debts is dependent on the unpredictable voting choices of their peoples," he said.

Professor Lucke, an expert on Real Business Cycle Theory, says German voters may not have mastered EMU mechanics but they can see it is going off the rails. "Everybody understands that 50pc youth unemployment in Greece and Spain is a catastrophe," he said.

The latest ZDF poll shows that 65pc of Germans think the euro is damaging, and 49pc think Germany would be better outside the EU. This is no doubt "soft", yet what is clear is that the all-party consensus on EMU gives voters nowhere to turn.

The rebels may struggle to cross the 5pc threshold for seats in the Bundestag, but they do not have to take seats to plague Angela Merkel over the next six months. She is already in trouble. Her Free Democrat (FDP) allies have crashed to 4pc in the polls.

Alternative für Deutschland threatens to take votes from the Right. On the other side, the Green resurgence to 16pc makes up for the sluggish Social Democrats. As things stand, the Left is slightly ahead. Angela Merkel is on course to lose office.

"Merkel will have to be even tougher on Europe, she cannot allow herself to be outflanked," said David Marsh, author of books on the euro and the Bundesbank. "She will try to keep up a steely facade and hope everything stays calm until September, but the next crisis may come to a head before that."

Indeed it may. Italy does not have a government, and putatitve premier Pier Luigi Bersani has vowed break out of the "austerity cage", explicitly rejecting policies that anchor the EU backstop for Italian bonds.

Fitch expects Italy's public debt to hit 130pc of GDP this year, up from 125pc forecast a few months ago. The country has one foot in a debt compound trap already. One more shock will do it.

This latest deterioration is self-inflicted, the result of contractionary EU policies that have pushed Euroland into a double-dip slump, and ravaged Italy in particular with fiscal tightening of 3pc of GDP in 2012.

This policy was deranged. Italy's primary budget was already near balance. Fiscal overkill caused to the economy to contract by 2.6pc in 2012, and the debt ratio to rise even faster. In flogging Italy's economy to death, EU elites have destroyed political consent for the reforms that are most needed.

For Germany's Alternative, September may come too soon. Michael Wohlgemuth from Open Europe says they lack the organization for a quick breack-through, but their moment may come in next year's vote for Euro-MPs.

"By then the real costs of the bail-outs for German taxpayers will be clearer. People sense that at a crisis is looming, but they have not yet felt it," he said.

The tragedy for Germany is that the bill for EMU will come due just as the country's aging crunch hits. Germany will have impoverished itself for no useful purpose, and without winning much love in the process.

Some say Germany is "winning" because its firms are conquering Club Med markets with a rigged exchange rate, but that is a Pyrrhic triumph. Latins will not tolerate this, once they grasp that the "gains" of their internal devaluations -- ie 1930s wage cuts -- are dwarfed by the greater losses of a wasted youth.

There are no winners. Each country is blighted in turn, and in different ways. Like Goethe's Sorcerer's Apprentice, they have launched an Like Goethe's Sorcerer's Apprentice, they have launched an experiment they cannot control. The broom has a fiendish will of its own.

and news of the day and from the wekend as well......

And over to another crisis-hit country... Portuguese GDP dropped 1.8% in the fourth quarter.

That's a very bad result as it shows a rapid acceleration in the contraction of the economy, driven by a fall in exports.

Portugal is weighed down by a stinging austerity package, which many say have worsened the country's economic outlook.

Today's figures confirm original estimates and provide new data showing exports dropped 2.4% in the fourth quarter.

Greece remains mired in deep recession

The Greek economy, meanwhile, contracted by 5.7% in the fourth quarter, a slight improvement on initial estimates of a 6% decline.

That points to Greece contracting by 6.4% over the year, an improvement on the 7.1% contraction in 2011.

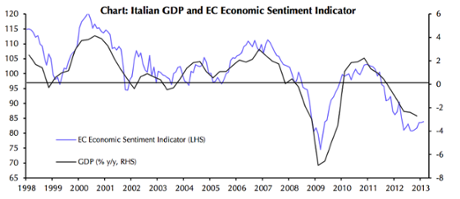

Italy's fourth quarter GDP figures confirmed the economy remained deep in recession at the end of last year.

Recent business surveys, which provide more up-to-date information, point to further sharp falls in GDP this year, while the ongoing political uncertainty will put spending under pressure. As a result, Capital Economics estimates the Italian economy could contract by as much as 3.5% this year.

Italian GDP and EC economic sentiment indicator Chart: Capital Economics

Looking at the French industrial production figures (see 8.32am), Capital Economics says it looks likely that France will officially re-enter recession this quarter.

Which just adds to a gloomy picture for the region as a whole. They write:

In all, then, the latest hard data, like the timelier business and consumer surveys, suggest that the euro-zone probably remained in recession in Q1. Given this, we continue to think that the consensus forecast for a fall in euro-zone GDP of just 0.2% this year is much too optimistic.

Sticking with Greece, our correspondent in Athens Helena Smith reports in this morning's paper that the country's privatisation chief Takis Athanasopoulos has resigned after only a few months in the job. She writes:

In another setback for Greece's reforms, Athanasopoulos resigned, after being charged with dereliction of duty in his former role as chief executive of the public utility PPC.

An official at the Greek finance ministry, Giorgos Mergos, also stepped down after being charged. Both men denied knowingly commissioning a loss-making plant when on the board of PPC, which led to losses of more than €100m for the state-owned power company.

Athanasopoulos said he welcomed the charges. "It gives me the opportunity to prove that the interest of the PPC and the state were fully served," he wrote in a resignation letter, insisting his decision to step down had been motivated by the desire not to further impede Greece's problem-plagued privatisation process.

More protests in Athens

Over to Athens, which has been rocked with protests and violence over the weekend. The so-called 'indignants' returned to Syntagma Square last night to be met by riot police, who used tear gas on them and made at least one arrest.

This morning, the protests continue. ekathimerini reports:

Culture Ministry employees were holding a protest in central Athens on Monday morning, on their second 24-hour strike in the last four days.

The civil servants gathered outside the Culture Ministry as archaeological sites and state-run museums remain closed.

The ministry employees are protesting about their department’s new organizational chart amid concerns about their job security.

Elsewhere in the city, ekathimerini reports that a homemade bomb went off late last night outside a branch of a courier service. No injuries were reported and the building suffered minor damage.

An Acropolis police station, meanwhile, was subject to an arson attack. A statement online said that it had been carried out in remembrance of Lambros Fountas, the member of the Revolutionary Struggle urban guerrilla group, who was shot dead by police two years ago. Nobody was injured in the attack although it caused substantial damage.

Police surround gathering demonstrators in front of the Greek parliament in Athens last night. Photograph: LOUISA GOULIAMAKI/AFP/Getty Images

Italy poses 'near and present danger'

But analysts still see political deadlock in Italy as a "near and present danger" for the eurozone.

Gary Jenkins of Swordfish Research says the most likely outcome from Italy's inconclusive elections is that some kind of market-friendly resolution will be found. But he says that could come under threat if Italian politicians come into conflict with the ECB.

The promise by ECB chief Mario Draghi 'to do whatever it takes' has largely becalmed the markets, he writes. But that could be tested if the crisis-hit countries refuse to play by Draghi's rules.

He notes Draghi's response at last week’s ECB press conference to a question regarding the potential for Italy to depart from the strategy of austerity:

Italy, like all the other countries, should continue first on the structural reform path, which is the only way that can restore growth, and second build on the very significant fiscal consolidation it has reached. That is very important because that is what gives credibility in the markets and therefore lower spreads and therefore in the end lower lending rates, therefore more credit to the economy and more job creation. This is the path.

Jenkins writes:

Now that didn’t sound to me like a man who thought that it was appropriate for Europe to move away from austerity. Thus it could bring him into conflict with politicians before very long if the economy does not recover and job creation remains non-existent in the stressed countries of Europe. Whilst Mr Draghi has stated he will do ‘whatever it takes,’ that does not necessarily mean that he will immediately cave in to the demands of politicians.

If Italy ends up with an anti-austerity government, the market might therefore assume that the ECB's promise of support via its bond-buying programme – the so-called OMT – could be weakening. Which could cause Italy (and consequently Spain)'s borrowing costs to escalate. Which could takes us back to the dark days of the crisis once more.

Italians in favour of sticking with euro

Back to Italy, where polls are showing a large majority if the population are in favour of staying in the eurozone and against a referendum on membership.

An opinion poll in Italian newspaper Corriere della Sera showed on Sudnay that 74% of Italians wanted to keep the euro, and just 16% wanted to return to the lira.

Almost 70% of Italians said they were either strongly or moderately against holding a referendum on membership of the eurozone, compared with 30% who though it was a quite good or very good idea.

That seems to conflict with last months' election results, where parties critical of austerity measures imposed by Europe fared particularly well.

But the poll showed that even among voters for Beppe Grillo's populist 5-Star Movement, some 73% did not want to return to the lira and 65% did not want a referendum.

For his part, Beppe Grillo has toned down his rhetoric on the single currency and last month denied that he ever called for a euro exit.

All I said was that we want to be informed about a plan B on leaving the euro, on what happens if we stay in and what happens if we leave, this information is our

right.

French factory output slumps

Ouch. French industrial production dropped by 1.2% in January, compared with a 0.9% rise in December.

Factory output contributed to the decline, down 1.4% on the month.

Looking over a longer time-horizon, industrial production dropped 3.3% in November-January, compared with the same period 12 months previously.

German imports rebound strongly

A quick look at the data out of Germany show the surplus narrowing in the eurozone's largest economy.

Imports rebounded in January after two weak months to rise by 3.3%, their fastest rate of growth since last May.

Exports were also up, rising 1.4% in January (seasonally-adjusted), the biggest rise in five months.

The surplus came down to €15.7bn, bang in line with economist expectations.

Chinese data disappoints

There was disappointing data out of China over the weekend, with inflation at a 10-month high in February while factory output and consumer spending were weaker than forecast.

First off, the inflation numbers. Official data showed the consumer price index rose 3.2% in February from a year ago, compared with expectations of a 3% rise. That could temper hopes that the Chinese government will boost spending in order to drive growth, which had lifted markets last week.

Annual growth in industrial production also slowed to 9.9% in January and February, compared with estimates of 10.6%.

While retail sales figures came in well below expectations, rising 12.3%, compared with forecasts of a 14.5% rise. That will raise concerns about domestic demand, particularly in light of rising prices.

Xu Gao at Everbright securities told Reuters:

This data shows that the economy is in the process of a mild recovery and that it is still fragile. It faces a lot of uncertainties.

Good morning and welcome to our rolling coverage of the eurozone crisis and other global economic events.

This weekend, the party set up by comic-turned-politician Beppe Grillo –the 5-Star Movement – said it wanted to lead the next Italian government and reiterated its opposition to an alliance with any of the main parties.

Reuters reports:

The movement's newly elected parliamentary leaders told reporters it would make this position clear to President Giorgio Napolitano when he begins consultations later this month on the formation of a government.

"Our proposal will be a 5-Star government," the movement's Senate leader Vito Crimi said after a meeting of its lawmakers in a Rome hotel.

It is unlikely that the other parties would accept a government led by the 5-Star Movement. This is partly because of policy differences and partly because although it was the most voted single party at the election, 5-Star has fewer seats in parliament than the center-left and center-right coalitions.

Italy was downgraded by Fitch on Friday to BBB+, with a negative outlook due to “increased political uncertainty and a non-conducive backdrop for further structural reform measures constitute a further adverse shock to the real economy”.

The country also awaits the final revision to fourth quarter GDP at 9am. We'll have all the news on that and other developments in the eurozone and beyond.

Lagarde could face formal investigation - Sunday Times

IMF chief Christine Lagarde could be forced to step down as a result of an inquiry into whether former French government officials were complicit in the payment of huge damages to a tycoon, the Sunday Times has reported.

Matthew Campbell writes:

Speculation is growing that Christine Lagarde, the former French finance minister who succeeded Dominique Strauss-Kahn at the helm of the IMF, may be placed under formal investigation after being summoned to answer questions by a judge in the next few days.

She is facing accusations of “complicity in embezzlement” of public funds for instigating an arbitration process that awarded £348m to Bernard Tapie, a controversial businessman who claimed to have been defrauded by a state-owned bank in the 1990s.

Lagarde, 57, has denied any wrongdoing, as has Stéphane Richard, the chief executive of France Telecom, her former chief of staff, whose home was raided by police last month.

Christine Lagarde, the managing director of the IMF, could be placed under formal investigation. Photograph: Art Widak/Demotix/Corbis

1112 Comments

1112 Comments