http://globaleconomicanalysis.blogspot.com/2012/12/more-nannycrat-insanity-eu-wants-to-ban.html

Looking for a reason for the rise of the neo-Nazis in Greece? Look no further than economic depression and over 50% youth unemployment. So what to do about it?

Courtesy of Google translate from German of Frankfurter Allgemeine, please consider EU Wants to Ban Youth Unemployment.

Economic Idiocy

It would be nice if the economic illiterates in the nannyzone would stop and figure out why youth unemployment is so high.

The primary answer is work rules, pension rules, and other rules are so harsh that companies simply do not want to hire workers.

France is heading down the same idiotic path with an economically insane proposal by French president Francois Hollande "Make Layoffs So Expensive For Companies That It's Not Worth It"

Any clear-thinking person should quickly realize that if companies cannot fire workers they will be extremely reluctant to hire them in the first place.

Thus, it should be no surprise to discover French Unemployment Highest in 14 Years (And It's Going to Get Much Worse).

Moreover, Italy, Spain, France, and Greece are already suffering from massive public sectors. Those sectors need to shrink, not expand.

In France, Government spending amounts to 55% of total domestic output. For discussion, please see Hollande's Honeymoon is Over; 54% of Voters Unhappy; Unions Promise "War" in September.

Now the nannycrats want government to take over still more of total output instead of shrinking it, at a time when every country in the EU is struggling to reduce deficits.

Insanity does not begin to describe the stupidity of this proposal, which I might add (the EU offers no way to implement in the first place).

Mike "Mish" Shedlock

and.....

http://www.ekathimerini.com/4dcgi/_w_articles_wsite2_1_03/12/2012_472775

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_03/12/2012_472594

( Greek Pension funds ( bonds still marked to par I bet ) out but Greek Banks in ? Wonder why the Greek Banks said they were going to refuse to participate last week , if that is the case ? And I haven't seen the Greek Banks ( one has to ask are the bonds they hold still at par or have they been marked down to market prices ) say they were agreeable to participating yet ! For the buyback to work , all Greek Banks have to sell plus a significant portion of the hedge funds need to pitch their bonds as well ! Recall , the Troika expects at least 40 billion in bonds to be bought by Greece !)

http://www.ekathimerini.com/4dcgi/_w_articles_wsite2_1_02/12/2012_472579

http://www.zerohedge.com/news/2012-12-03/greek-government-bonds-jump-12-buyback-means-early-christmas-hedge-funds

Submitted by Tyler Durden on 12/03/2012 09:04 -0500

Submitted by Tyler Durden on 12/03/2012 09:04 -0500

http://www.zerohedge.com/news/2012-12-03/greece-announces-terms-bond-buyback-repuchase-prices-higher-government-indicated-pre

Submitted by Tyler Durden on 12/03/2012 06:54 -0500

http://www.zerohedge.com/news/2012-12-02/next-recovering-europe-30-50-collapse-wages-spain-italy-and-france

Submitted by Tyler Durden on 12/02/2012 22:19 -0500

http://www.businessweek.com/news/2012-12-02/ecb-can-t-deliver-spain-spread-rajoy-wants-wellink-says

Photograph: Guardian/Markit

Photograph: Guardian/Markit

Photograph: Reuters

Photograph: Reuters

Monday, December 03, 2012 2:42 PM

More Nannycrat Insanity: EU Wants to Ban Youth Unemployment

Youth unemployment is shockingly high in Greece, Spain, and Italy as shown by Europe's Most Tragic Graph by The Atlantic.

Young workers in Greece and Spain are facing an absolutely egregious work drought, where half of high-school and college-graduates ready to find a job aren't finding one. And 55% isn't the ceiling. Both economies are shrinking and unemployment is a lagging indicator -- as Americans have learned, the rate can keep going up after an economy technically starts growing. This economic tragedy can easily become a social disaster as young promising people either leave their country to work somewhere else or else turn to illegal or violent activities to protest policies wrecking their economies or lash out against a country that's leaving them behind.EU Wants to Ban Youth Unemployment

Looking for a reason for the rise of the neo-Nazis in Greece? Look no further than economic depression and over 50% youth unemployment. So what to do about it?

Courtesy of Google translate from German of Frankfurter Allgemeine, please consider EU Wants to Ban Youth Unemployment.

The European Commission wants to oblige EU countries to all people under 25 to secure a job. How states are to implement the guarantee, it will not betray.

The Member States of the European Union should guarantee all people aged less than 25 years in the future, within four months some form of employment. These governments should issue a so-called youth guarantee, as stated in a regulatory package that wants the department responsible Commissioner László Andor imagine this Wednesday in Brussels.

Economic Idiocy

It would be nice if the economic illiterates in the nannyzone would stop and figure out why youth unemployment is so high.

The primary answer is work rules, pension rules, and other rules are so harsh that companies simply do not want to hire workers.

France is heading down the same idiotic path with an economically insane proposal by French president Francois Hollande "Make Layoffs So Expensive For Companies That It's Not Worth It"

Any clear-thinking person should quickly realize that if companies cannot fire workers they will be extremely reluctant to hire them in the first place.

Thus, it should be no surprise to discover French Unemployment Highest in 14 Years (And It's Going to Get Much Worse).

Moreover, Italy, Spain, France, and Greece are already suffering from massive public sectors. Those sectors need to shrink, not expand.

In France, Government spending amounts to 55% of total domestic output. For discussion, please see Hollande's Honeymoon is Over; 54% of Voters Unhappy; Unions Promise "War" in September.

Now the nannycrats want government to take over still more of total output instead of shrinking it, at a time when every country in the EU is struggling to reduce deficits.

Insanity does not begin to describe the stupidity of this proposal, which I might add (the EU offers no way to implement in the first place).

Mike "Mish" Shedlock

and.....

http://www.ekathimerini.com/4dcgi/_w_articles_wsite2_1_03/12/2012_472775

State bond buyback terms seen as favorable

Market gives positive response to PDMA proposal to cut Greek debt and help release bailout tranche

By Sotiris Nikas

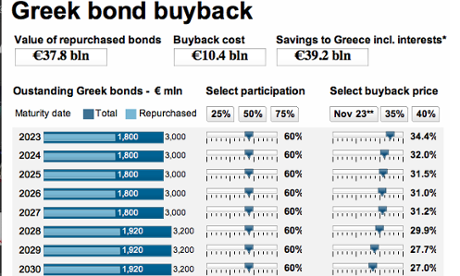

The buyback process for Greek state bonds began officially on Monday on better terms than expected, with the government well aware that its outcome will determine whether Greece manages to secure the disbursement of 34.4 billion euros in bailout funds on December 13.

The price range at which the state will buy back its bonds is higher than what the markets had anticipated, as it stands about 4 to 10 percent above November 23 prices, which were originally thought to be the yardstick. The Dutch auction method chosen sets a minimum price for bonds and means that the state will pay the same amount to all bidders at the price of the highest bid, a measure which will be good for Greek banks, which will also participate.

The Public Debt Management Agency (PDMA) announced on Monday that the country will have 10 billion euros at its disposal for the program from the European Financial Stability Facility (EFSF), with offers from private bondholders to be accepted up until 7 p.m. on Friday.

However, as the text of the invitation states, Greece reserves the right to stop the program when it sees fit, or extend it or even cancel it altogether. The most likely of the three is an extension if that is considered useful to cover the interest by bondholders.

As things stand, the arrangement date is December 17, but what is certain is that Pthe DMA maintains the right to accept any offers it considers as the best for Greece and the effort to reduce its debt, regardless of what private bondholders offer.

The total amount of bonds for the buyback stands at 61.4 billion euros. The PDMA will conduct 20 different auctions, as many as the number of bonds in question.

The market’s response to the invitation of interest was favorable. Foreign analysts told Kathimerini that the terms of the proposal are good, and this was also reflected in the spread between the Greek 10-year bond and the benchmark 10-year German bund, that was reduced by about 150 basis points yesterday compared with last Friday. The Royal Bank of Scotland recommended that investors participate in the Greek bond buyback program, while the Financial Times cited Greek bankers saying that the minimum price set will bring the desired result.

and.....

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_03/12/2012_472771

Coalition seeks to heal splits over new tax bill

Income tax proposal splits coalition, likely forcing Stournaras to find alternative

Finance Minister Yannis Stournaras presented at Monday’s Eurogroup meeting in Brussels the plan for buying back Greek government bonds, which Athens had announced several hours earlier. The Finance Ministry said it would buy back the paper, paying from a minimum of 30.2 to 38.1 percent and a maximum of 32.2 to 40.1 percent of the principal amount, depending on the maturities. The aim is to reduce Greek debt by about 20 billion euros. At the end of the meeting, Eurogroup chief Jean-Claude Juncker said no further decisions would be taken regarding the release of Greece's next loan tranche until the buyback has been completed. “I would not wish to go into details [of the buyback] at this time,” he said. “We will reconvene on December 13 to finalize our decision.” However, Juncker said that he was confident Greece would receive approval for its next installment. Back in Athens, Prime Minister Antonis Samaras summoned Stournaras’s deputy, Giorgos Mavraganis, to a meeting at Maximos Mansion to discuss the proposed new tax code, which the government needs to pass through Parliament in order to reach one of the “milestones” its lenders have demanded before approving the release of more funding early next year. Coalition partners PASOK and Democratic Left oppose plans to tax annual incomes above 26,000 euros at a rate of 45 percent. PASOK leader Evangelos Venizelos said this would turn society in its entirety against the government. “People cannot pay this. We need to find alternatives,” said Democratic Left spokesman Andreas Papadopoulos. “There is no way the tax bill will reach Parliament in its current form.”

|

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_03/12/2012_472594

( Greek Pension funds ( bonds still marked to par I bet ) out but Greek Banks in ? Wonder why the Greek Banks said they were going to refuse to participate last week , if that is the case ? And I haven't seen the Greek Banks ( one has to ask are the bonds they hold still at par or have they been marked down to market prices ) say they were agreeable to participating yet ! For the buyback to work , all Greek Banks have to sell plus a significant portion of the hedge funds need to pitch their bonds as well ! Recall , the Troika expects at least 40 billion in bonds to be bought by Greece !)

Pension funds not part of buyback, says PM

In an interview with the Sunday edition of Ethnos newspaper, Antonis Samaras said Greek banks will benefit from the transaction, because the book value of the bonds they hold is really low. Greek bank stocks have been hit over the past week after it became clear that the buyback scheme was a precondition for the release of nearly 44 billion euros ($57 billion) in bailout aid from Greece's creditors. Samaras says buying back the holdings of Greece's pension funds was never in play because this would not reduce Greece's debt. Finance Minister Yannis Stournaras is due in Brussels again on Monday – for the fourth Eurogroup meeting in as many weeks – where he is expected to present to his eurozone peers details of a bond buyback scheme. [Combined reports] |

http://www.ekathimerini.com/4dcgi/_w_articles_wsite2_1_02/12/2012_472579

Memorandum brings forward selloff projects

The selloffs of train service operator TRAINOSE, Hellenic Post, horse racing organization ODIE, Athens International Airport and others are expected to begin one or two quarters earlier than the previous draft provided for. The November 27 draft now provides for the postal company’s privatization to start in the first quarter of 2013, instead of the second, while the start of the process for the sale of TRAINOSE is brought forward from Q4 to Q2 of next year. The procedure for the sale of ports and regional airports has been accelerated by three months, while the restart of the privatization of Athens airport is to take place six months earlier. The only exception is the privatization of Egnatia Odos, the highway that runs across northern Greece, which has been postponed from the first to the second quarter of next year. |

http://www.zerohedge.com/news/2012-12-03/greek-government-bonds-jump-12-buyback-means-early-christmas-hedge-funds

Greek Government Bonds Jump 12% As Buyback Means Early Christmas For Hedge Funds

Greek Government Bonds (GGBs) jumped by over 12% today to over EUR40 - by far the highest post-PSI - as fast money floods the limited size illquid market to front-run the Greek buyback. Every day that goes by means less and less benefit for the Greek people as the discounted price of buying back the debt - with all of the money that Greece doesn't have, goes up. This is a perfect example of greater-fool-theory at work as everyone knows that if this price gets too high, the Greek government (via Troika) will (should) reneg on the buyback which will cause GGB prices to plunge back towards zero. What many misunderstand is that the buyback crystalizes the losses for banks that currently carry this worthless paper on their books at Par and garner the carry (and accruals) and thus in true European fashion, the unintended consequence of this action lines the pockets of fast-money hedge funds along for the short-ride and drains any pretense of capital from the Greek banking system.

http://www.zerohedge.com/news/2012-12-03/greece-announces-terms-bond-buyback-repuchase-prices-higher-government-indicated-pre

Greece Announces Terms Of Bond Buyback, Repuchase Prices Higher Than Government Indicated Previously

It may still be unclear just where Greece will get the ~€10 billion in cash needed to buyback up to 20 various tranches of the post-restructuring GGB2 bonds (full CUSIP list below), but what the Greek Public Debt Management Agency announced today was the sound of money in the ears of the hedge funds that had bought up Greek bonds in the low teens several months ago, if not so much Greek banks many of whom may still have this debt market at up to par, as no matter which particular group of taxpayers ends up funding this "buyback" - a process that will have zero benefit to the Greek population who will see not one penny of the buyback proceeds (as described before) - it is the hedgies that benefit, who also have clearly controlled the process from the beginning as the announced tender prices were well above the levels Greek bonds eligible under the buyback closed at on Nov. 23, even though Greece's lenders last week said they did not expect the bonds to be purchased for more than the closing price on that date. In other words, the Greek government lied to its people again for the benefit of wealthy financial interests yet again.

And sure enough, with the purchase price for most issues which will be set in a Ducth Auction, anywhere between 30.2% and 32.2% for the longer date issues, and 38.1% to 40.1% for the short-maturities, coming in higher than expected, the entire Greek bond market has risen to fresh post restructuring highs, as have bonds across the periphery, with Spanish and Italian bonds moving higher in price, on hopes that since Greece gets the benefit of massive bond upside from market lows, why shouldn't these two countries. After all, European taxpayers now appear to be the involuntary benefactors for the world's largest hedge funds, courtesy of their unelected Eurogroup leaders, and the IIF of course.

We now sit back in hopes of learning just where Greece will get the up to €10 billion in cash used to repurchase ~€30 billion in face notional

Details on the buyback:

Summary of Expected Terms of the EFSF Notes:

Issuer European Financial Stability Facility

Issue Not expected to exceed €10,000,000,000

Final Maturity Expected to mature on or about 6 months after the

Settlement Date of the Invitation

Interest Basis Zero coupon

Form Global Bearer Note deposited with Clearstream, Frankfurt

Clearing The EFSF Notes will clear through Clearstream, Frankfurt

Governing Law English Law

Issue Not expected to exceed €10,000,000,000

Final Maturity Expected to mature on or about 6 months after the

Settlement Date of the Invitation

Interest Basis Zero coupon

Form Global Bearer Note deposited with Clearstream, Frankfurt

Clearing The EFSF Notes will clear through Clearstream, Frankfurt

Governing Law English Law

Full list of participating issues:

And more from Reuters:

Greece said it would spend 10 billion euros to buy back bonds in a bid to reduce its ballooning debt and unfreeze long-delayed aid, setting a price range above market expectations to ensure sufficient investor interest.The bond buyback is central to the efforts of Greece's foreign lenders to put the near-bankrupt country's debt back on a sustainable footing, and its success is essential to unlocking funding Athens needs to avoid running out of cash.There have been questions about whether it will tempt enough bondholders to cut Greek debt by a net 20 billion euros, the target set by euro zone finance ministers and the International Monetary Fund. The buyback plan announced on Monday appeared designed to quell those concerns.

"It indicates they really want the swap to succeed," said Ricardo Barbieri, strategist at Mizuho, on the pricing.

"Some investors might be tempted to participate in the swap because of the ability to simplify their position, should they wish to maintain exposure to Greece, otherwise an opportunity to exit totally, completely their positions at a level that is better than Friday's close."The buyback will be conducted through a modified Dutch auction that introduces an element of competition among investors and set a price range above Friday's closing prices.The range set varied from a minimum of 30.2 to 38.1 percent and a maximum of 32.2 to 40.1 percent depending on the bond maturities of the 20 series of outstanding bonds.

It featured a spread of two percentage points between the highest and lowest price offered on each bond.

The prices were well above the levels Greek bonds eligible under the buyback closed at on Nov. 23, even though Greece's lenders last week said they did not expect the bonds to be purchased for more than the closing price on that date.The bonds, which have a nominal value of 63 billion euros, closed at between 25.15 to 34.41 cents in the euro on that date according to Reuters data.DOUBTS REMAINEuro zone officials said the bloc hoped Greece would be able to repurchase at least 40 billion euros of its own bonds.

Athens unveiled the structure of the buyback before a meeting of euro zone finance ministers, at which Greek Finance Minister Yannis Stournaras will brief his counterparts.

Despite the better than-expected terms, some analysts said it remained to be seen whether the buyback would be successful. Greek banks are under pressure from Athens to participate, but there is skepticism over how many foreign investors will do so."I still have my doubts regarding how many investors will participate on the buyback at these prices," said Diego Iscaro at IHS Global Insight. "The prices may be higher than expected .. but my doubts are whether they'll be high enough to encourage a high participation rate."

Even if the Greek debt buyback is successful, Athens' long-term debt problems have yet to be fully resolved. Greece's EU and IMF lenders want to cut the country's debt - which is expected to peak at 191 percent in 2014 - to 124 percent of gross domestic product by 2020 but there has been speculation that some write-off of loans will be necessary.

* * *

Next Up For A "Recovering" Europe: A 30-50% Collapse In Wages In Spain, Italy And... France

- Bond

- Double Dip

- Equity Markets

- European Central Bank

- Eurozone

- Fail

- France

- Germany

- Greece

- Gross Domestic Product

- Housing Bubble

- Italy

- None

- Portugal

- Reality

- Recession

- The Economist

- Unemployment

- United Kingdom

Several weeks ago Europe officially entered a double dip recession, and based on various secondary economic indicators, even Europe’s primary economic powerhouse, Germany, is on the verge of negative economic growth. The reasons for Europe’s woeful macroeconomic state are numerous, but boil down to two primary ones: i) massive external imbalances among Eurozone nations (think soaring peripheral debt) coupled with the inability to devalue the common currency as that would mean a failure and collapse of the joint currency union, ii) a desperate need for the periphery to regain price competitiveness (via wages and labor costs) with Germany in order to arrest and collapse an unemployment rate (general, but especially youth) that not even the most optimistic pundits dare claim is sustainable.

Said otherwise, most European countries (including France) face a desperate need for external devaluation, which is impossible under a monetary union, leaving only internal devaluation as an option. This is where the much maligned concept of austerity comes in: from a macroeconomic perspective, austerity is not so much an exercise at moderating the pace of debt increase (as neither Spain nor Italy have reduced their rate of debt issuance), but of gradually becoming more price competitive with Germany: a key outcome that will be needed for the Eurozone to have any chance of survival, i.e., lowering stickyunemployment rates from levels that virtually assure social "disturbances" in the months and years ahead.

And herein lies the rub: because while protests against “austerity” (which as we observed recently has still not been truly implemented in Europe, and certainly not in Portugal or Spain) are a daily event in most PIIGS nations, “you ain’t seen nothing yet.“ The reason: to achieve the unavoidable macroeconomic rebalancing, and to collapse the spread between soaring labor costs in the periphery and those of Germany (see chart below), the bulk of European countries will need to see wages collapse by anywhere between 30% and 50% to compensate for the lack of state-level currency devaluation optionality. And yes, this includes France.

Goldman’s Huw Pill explains the scary future facing peripheral European workers:

We ask the following question: For the Euro area countries of interest, how big a real exchange rate depreciation (which (to recall) in monetary union means (to a first approximation) a relative wage cut) is required in order to establish a sustainable external position.

The results of our exercise are shown below. They demonstrate that relying solely on internal devaluations to correct existing imbalances implies a need for very large wage and cost adjustments. For the small and vulnerable peripheral countries (Greece and Portugal), we would need to see wages fall by at least 50% relative to Germany (from their level at the start of 2011) if this mechanism alone were to re-establish external sustainability. And even for larger and richer countries such as Spain and France, relative wage reductions (on a comparable basis) of 30%+ are needed.

Which begs the question: how will the long-suffering workers of Greece, Spain, and Italy (and also France), who are confident they have gone to the 9th circle of hell in the past 4 years, react when they realize that none of the needed internal devaluation has actually taken place yet?

In other words, what happens when Spanish wages tumble by another 30%, as they must if the EUR, and the Eurozone, is to survive? Alternatively, if there are no labor cost cuts, how many more years and months of 1%/month unemployment increases will the unemployed in the periphery suffer before it realizes that chronic 25%+ unemployment is here to stay, as is the European Depression. What is most sad is that the economic reality is that regardless of the “all clear” that central-bank-manipulated market indicators tell us, the European imbalances continue deteriorating at a rapid pace.

And the paradox is that as long as market indicators aren’t flashing red, no politician has the urge to enact the critical laws needed to fix the underlying problem, as that same fix will lead to an immediate end of said politician’s career.

Needless to say, not even Goldman thinks that kindly asking for Greek and Spanish workers to take another 30-50% pay cut is feasible and would lead to anything short of revolution (and the alternative: asking Germany to adopt a wage increase and watch German inflation surge is just as ludicrous):

We view relative wage cuts of this magnitude as unfeasible:it is difficult to imagine France accepting a one-third fall in living standards relative to Germany. Of course, one could rely on Germany to raise wages, so as to redress the competitiveness gap from the other side. But ultimately such an approach would imply Germany accepting much higher rates of inflation, say above 4% pa for a decade or more, assuming the ECB met its target of keeping area-wide inflation close to 2%. We doubt the German public would countenance such an eventuality….

So does this mean that despite all best efforts to the contrary, when one looks beyond the daily hollow rhetoric emanating from Brussels and focuses on the simple economics of it all, that the Eurozone is doomed? While our pessimistic opinion on the viability of the failed European project is well-known, not even Goldman can bring much words of encouragement:

To answer that question, we need to explore the implications of relaxing some of the assumptions that underlie the exercise described above. First, we could implement the necessary relative wage adjustment through resort to nominal exchange rate changes. But allowing exchange rates to vary implies exit from the Euro area and reintroduction of national currencies. Relying on this mechanism implies recognising the impracticality of the euro, rather than describing how it can be saved.

Second, uncompetitive economies could suppress domestic demand to contain imports and run with mass unemployment on an ongoing basis. In our view, this is not politically feasible. British experience in the late 1920s (following Winston Churchill’s decision to put Britain back on the Gold Standard at its pre-first World War parity) demonstrates as much. High unemployment, recessionary conditions and lost export markets were the precursors to abandoning gold rather than mechanisms for sustaining British adherence to it. One would expect as much for the Euro area periphery: if mass unemployment become endemic and permanent, it would eventually precipitate euro exit.

Third, uncompetitive peripheral countries could be subsidised on an ongoing basis by the more competitive surplus countries, i.e., a system of fiscal transfers from north to south could close the current account deficit and eliminate the existing imbalances. Such mechanisms are quite normal in continental monetary unions: witness the transfers from wealthy New York to poorer West Virginia via the federal government in the United States.

But the institutional mechanisms and political support for such area-wide redistribution are (as yet, still) lacking in the Euro area.

It is worth pointing out that the ad hoc and very much informal (after all Merkel’s reelection chances are much lower if the German people understand what is really happening in Europe) transfer union has worked so far primarily because it funded the relatively modest economy of Greece. Yet even ordinary Germans understand that the Bundesbank’s TARGET2 claims are nothing more than Germany’s implicit fiscal transfer mechanism to the rest of Europe (one which happens to benefit German exporters: i.e., a public to private transfer scheme), one which is soaring by tens of billions each month.

To be sure all such indefinite ad hoc attempts to delay the day of “labor-cost equivalency”-reckoning using piecemeal and incomplete fiscal transfers from Germany to everyone else, will one day fail, when surging nationalist parties across Europe just say “nein” to ceding sovereignty to Germany which will eventually demand all Europe bow down to it in exchange for a full-blown fiscal union and Eurobond initiative in which Germany officially bears the cost of “temporary-to-permanent” Current Account imbalances, by shifting from TARGET2 to a wholesale German-funded fiscal union. This “unthinkable scenario” is quite thinkable by most, especially Europe, but in this case certainly Goldman:

A number of the options listed above are feasible for the smaller peripheral countries. Since the magnitude of structural change required to make them sustainable is so large (and the institutional capacity to implement those changes open to question), it is likely that we will see a prolonged period of both mass unemployment and subsidisation if they are to remain within the Euro area. This has been the experience thus far. Indeed, recent discussions over the terms of financial support for Greece in Brussels can be seen as a codification of how the subsidies will be provided in that case.

At the same time, we should not ignore the possibility of exit: were the rest of the Euro area to develop sufficient robustness to manage the transition, one could easily imagine a Euro without Greece or Cyprus.

But for the larger countries, options are much more limited. It is unthinkable to have a Euro area without France; at that point, it would become little more than a greater Deutsch mark zone. The politics of perpetual mass unemployment are equally infeasible as in the small peripheral countries. And France and Spain are simply too large to subsidise on an ongoing basis. So there is no alternative but to implement a restructuring of the economies to reduce the needed real depreciation to a plausible level. But the nature of the restructuring needs to be tailor-made for the country concerned.

The only good news to date, if one may call it so, is that Spain has already taken some modest steps to address its internal devaluation. However that former AAA-stalwart, and now bastion of resurgent socialism, France has not. And it is here that those who took offense to that recent edition of The Economist with the ticking time baguette cover should be paying attention.

Spain’s economy is weak and vulnerable at present. But while of little comfort to those unemployed, there is a silver lining to that weakness: it is associated with a necessary restructuring that offers hope of a more balanced and competitive Spanish economy in the future.

Unfortunately, there are reasons for greater caution with regard to developments in France. Like Spain, France also needs to shift resources into the tradable sector in order to reduce its chronic and deteriorating current account deficit. But France’s problem is not a bias towards the construction sector as in Spain, but rather a bloated public sector. Public expenditure in France is 56% of GDP, compared with 47% in Germany: the inherently domestic-oriented nature of government spending implies that France produces too few tradable goods relative to Germany.

In Spain, a largely spontaneous bursting of the housing bubble initiated the necessary restructuring of the economy. But in France a conscious political decision to shrink the state is needed to achieve the restructuring. And the political obstacles to that decision are high. While the French authorities increasingly recognise the need to improve French competitiveness, developing an understanding that this implies a deep restructuring of the economy remains elusive, at least at the political level, as recent discussion of industrial policy attests.

And then there is that other wildcard: the UK. As CLSA’s Chris Wood writes in his latest edition of Fear and Greed:

Europe, the path ahead for the Eurozone was made crystal clear with a plan unveiled by European Commission President Jose Manuel Barroso on Wednesday, outlining the need for an overhaul of Eurozone institutions to pave the way for the collective issuance of debt. This fits GREED & fear’s base case; namely that the Eurozone is moving towards “debt mutualisation”, a process which will ultimately lead to fiscal union. This week’s “deal” on Greece, with its extension of maturities and lowering of interest rates, is a further indication of the political determination to keep the Eurozone going in its present form and the unwillingness to contemplate the stresses of a Greek exit.

The above is also why the real political tension triggered by the direction in which the Eurozone has now embarked will turn out to be in Britain, not Spain or Greece. This is because there is real antagonism towards the Eurozone in Britain whereas in Greece and Spain the majority of people continue not to blame the euro for their problems. This is why it is possible that the Eurozone can make a deflationary adjustment, as indicated by the periphery countries’ improving current accounts. It is also why Britain’s fresh-faced Prime Minister, David Cameron,has a political problem.

All of the above is correct: the true European fulcrum nations have now shifted from the PIIGS to France and the UK, but it will take some time for this to become evident. What is unclear is the question of timing. And with Europe hell bent on actually addressing the real underlying causes for its persistent recessionary state instead of merely attacking the symptoms (soaring yield spreads, plunging equity markets, diving EUR FX rate), one can be sure nothing will change as long as the ECB gives the impression that European imbalances are under control, courtesy of a bond purchase backstop, which sooner or later will be activated at which point this too threat will become reality, and like QEternity, will lose all potency.

It is only then that Europe will have some hope of finally addressing that which is the true basis for its unsustainability: the internal imbalances which in the absence of currency adjustments can only be addressed through collapsing labor costs, and wages.

Yet telling a continent, which in its desperation is hopeful and confident that the worst is behind it (as its lying politicians take every opportunity to note) that the most acute of standard of living collapses is yet to come, is borderline cruel and unusual. So we will just keep our mouths shut and let Europe’s politicians bring this depressing message to their people. We are confident the reaction will be more than dignified.

and note the ECB OMT plan for Spain works only if just hopium and not actually executed .... as per ECB policy maker Wellink

Former European Central Bank policy maker Nout Wellink said Spain can’t realistically expect officials to narrow the bond spread with Germany to as little as 200 basis points, as he predicted “execution problems” with the ECB’s bond program.

If Prime Minister Mariano Rajoy envisages “that the maximum difference with the Germans is 200 basis points, then he makes a mistake,” Wellink, the former Netherlands central bank governor who retired from the post in 2011, said in a Bloomberg Television interview on Nov. 30. “Two hundred basis points seems to me too much” to hope for, he said.

Spain is still resisting asking for aid, a prerequisite to trigger the ECB’s Outright Monetary Transactions program, its new government bond-purchasing program. Rajoy said Nov. 6 that Spain needs to know by how much its borrowing costs would fall if it sought a bailout, signaling he favored a narrowing of the spread to 200 basis points, half the current one.

“As far as I understood it, the ECB wants to deal with the breakup risk of the system and there are other risks also,” said Wellink, who served on the ECB’s Governing Council for more than a decade. “These risks show up in interest-rate differentials.”

Spain’s 10-year bond yield was 5.3 percent at 9:16 a.m. in Frankfurt today. That’s 394 basis points above the German security of a similar maturity.

Market Rally

Financial markets have rallied since the ECB pledged sovereign-bond purchases in August to reduce the financing costs of debt-strapped nations such as Spain and Italy, and safeguard the euro. The program would be run in tandem with Europe’s bailout fund and countries have to agree to overhaul their economies and structural deficits.

While the OMT has been “very instrumental in calming markets,” Wellink said he also “sincerely” hopes it does not need to be activated and envisaged “some execution problems when it comes to using this instrument in practice.”

ECB President Mario Draghi has said the ECB would stop buying immediately if a country reneged on its commitments, and envisages that officials would also not buy bonds as long as the so-called Troika comprising the European Commission, the ECB and the International Monetary Fund are assessing a country’s progress.

“It’s easy to say you stop intervening the moment the Troika lands in the capital but it’s more difficult to forecast whether you can stick to this promise because you don’t know what’s going to happen during that period,” said Wellink, who is the chairman of the Basel Committee on Banking.

Greek Story

There could be other problems that “depend on the circumstances,” he said.

On Greece, Wellink said that last week’s deal easing the terms on emergency aid for the country “is not the end of the story” and “we might need a new program in 2014.”

He also said he doesn’t “exclude” a debt writeoff by the official sector “as a consequence of this package.”

“I see an increased willingness to solve the Greek problem,” Wellink said.

http://www.guardian.co.uk/business/2012/dec/03/eurozone-crisis-greece-bond-buyback-launched

Italian bonds rally

Italian government debt have been strengthening this morning, pushing down their yield (the interest rate on the bonds).

And in the last couple of minutes the spread between Italian and German 10-year bonds has dropped below 300 basis points mark for the first time since March.

Italy's 10-year bond yield: 4.39%, down 11 basis points

Germany's 10-year bond yield: 1.418%, up 3 basis points.

Another fillip for those who reckon the eurozone crisis is petering out

(or at least entering a calmer phase)

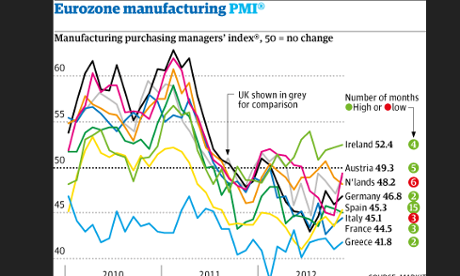

We've plotted this morning's manufacturing data (see 9.44am onwards) on one graph, showing how the main eurozone countries and the UK have performed:

Photograph: Guardian/MarkitScepticism in Greece over bond swap deal

Over in Greece our correspondent Helena Smith says the debt buyback has got a mixed reception this morning. She writes:

Among economists, analysts and even government officials there is widespread scepticism about the scheme. Speaking on the state-run TV channel NET this morning, finance experts described the buyback operation as “very problematic” with many calling it the most difficult part of the latest EU-IMF backed attempt to rescue Greece.“A big part of the bonds that have been issued are in the hands of hedge funds,” said prominent economics professorCharalambos Gotsis, adding that investors had acquired them earlier in the summer at very good rates. “With Greece no longer facing the scenario of a Grexit, it is debatable whether they will want to part with them,” added Gotsis who reckoned that hedge funds had acquired around €20bn worth of the government bonds.Greek banks, which hold an estimated €15bn of the new bonds, have also opposed the scheme claiming it will put them in the onerous position of having to forfeit potential profits.Their stance prompted Prime Minister Antonis Samaras to insist over the weekend that banks would actually benefit from the deal as the value of the bonds they held was far lower. Samaras, who is acutely aware that Greece’s next €44bn loan tranche is dependent on the buyback (with officials saying it will pare back the country’s debt load by at least €30bn), also quashed speculation that Greek pension funds would be part of the transaction. “The banks’ reaction undoubtedly played a role in the offer being better than expected,” said one insider referring to government prices being more generous than anticipated [as explained at 8.38am]

But, interestingly, Greek finance ministry officials this morning did not rule out the scheme being extended beyond the official close of the deal at 5pm Friday, adds Helena.

'If it doesn’t go well then logically [the scheme] will be extended,' said one finance ministry official. 'But let’s not jump the gun and talk about failure before it has even got off the ground.'

Updated

Eurozone manufacturing sector shrinks again

It's one of those mornings when we're inundated with manufacturing data for the previous month from across the global economy (via Markit)

Today's Purchasing Managers Indexes (PMIs) paint a mixed picture - so here are the highlights (and as a reminder, any number below 50 = contraction).

• The eurozone's manufacturing sector's PMI of 46.2 for November was the highest since March, but means the sector has now shrunk for the last 16 months

• Germany kept shrinking, with a PMI of 46.8, up from 46.0 in October.

• France's manufacturing output fell sharply again, with a PMI of just 44.5, up from October's 43.7. [garble corrected - thanks madeupname2 !]

• Greece's manufacturing sector continued to contract sharply, with a PMI of just 41.8 (slightly better than October's 41.0).

Updated

A Greek debt calculator

Those bright sparks at Reuters have created an interactive Greek bond buyback calculator, which lets you work out how much Athens could slice off its debt mountain through the swap.

Photograph: Reuters

Remember that the buyback cost can't exceed €10bn (the maximum amount of new bonds that Greece plans to offer in exchange).

Playing around with it, I can get Greece's savings up to €52bn....

No comments:

Post a Comment