Commentary on the economic , geopolitical and simply fascinating things going on. Served occasionally with a side of snark.

Friday, February 7, 2014

Bitcoin Plunges As Major Exchange Mt. Gox Halts All Withdrawals ( Is the amount of customer money frozen 38 million dollars , seems like that is the amount of unfilled withdrawals as of 2/4/14 ? And are more than one million Mt Gox customers at risk ? ) - volume on the top three exchanges appears much higher than normal today ! BTC-e Pulls Support for Ruble As Russia Bans Bitcoin ....... LocalBitcoins.com Users Face Criminal Charges in Florida ...... Coinbase Moves to Calm Security Concerns Amid Theft Reports ......Following Mt. Gox Sell-Off, Cyprus Warns of Bitcoin’s Volatility ...... Bad news day for bitcoin !

With the ongoing mess with MT Gox , trust is going to be an issue moving forward - Say hello to regulation folks !

SecondMarket Takes First Step to Becoming a US Bitcoin Exchange

SecondMarket has taken its first step to becoming a US-based bitcoin exchange, the company’s founder and CEO Barry Silbert has suggested.

Silbert took to Twitter today to announce that his alternative investment company is now buying bitcoins from interested sellers, then told CoinDesk this could mark a move into the US exchange market. He said:

“There is a clear need for a US-based, regulated, compliant and trustworthy bitcoin exchange. This could be the first step in that direction.”

The announcement follows Mt. Gox’s decision to halt all bitcoin withdrawals from its service one day earlier. The surprise move sent bitcoin markets into decline in the hours that followed, and caused uncertainty to spread throughout the bitcoin community.

Silbert did not mention the big-picture implications of the new service in his Twitter post, but did indicate that SecondMarket is now open to both buyers and sellers.

Major Bitcoin Exchange Not Executing Withdrawals; Now Owes Clients $38M In Disappeared Money

114

CRYPTOCURRENCY

CRYPTOCURRENCY

MtGox, the oldest and once-largest bitcoin exchange, appears to have a serious problem. Since about a week ago, clients’ bitcoin withdrawals have been deducted from their account, but the clients never received the money – the money withdrawn was effectively disappeared into thin air. The community is furious and as of now, MtGox has racked up over USD 38 million in such unfulfilled withdrawals.

MtGox was once the undisputed king of the hill among bitcoin exchanges. If MtGox froze its trading, which has happened, then bitcoin trading froze as a whole – the exchange was that dominant. In the past year, other exchanges have gradually sprung up, and today, MtGox accounts for about one-third of trade – it’s still a very strong player, even if not dominant.

MtGox has always had various regulatory problems transferring funds in and out of US Dollars, but according to client testimonies and reviews, other central-bank currencies – euros, yen – have always worked like clockwork. Since about a week back, though, withdrawals of bitcoin – the opposite of central-bank currency – from the exchange have started to fail in a seemingly random fashion.

When bitcoin funds are transferred, that normally happens instantly – the received sees the funds within seconds. That’s one of the strengths of bitcoin: you can transfer money, unlimited amounts of money, anywhere in the world instantly and unstoppably.

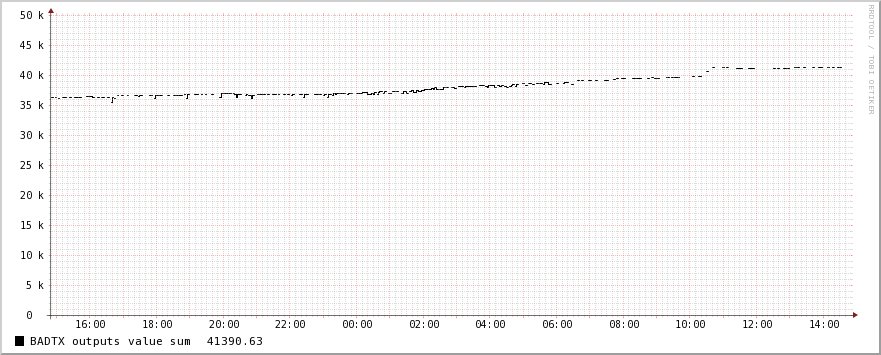

Since about a week ago, MtGox has not processed all requested bitcoin withdrawals and many clients have not received their bitcoins. Instead, some of the withdrawals were processed while the rest of the withdrawals remain frozen in an undetermined condition. Affected users are upset by this since the money is gone from their account, but the bitcoins have not been transferred to the client’s control. As of noon on February 4, The Gox Report has this chart, which is based on MtGox’ own internal data:

Note the bottom, the sum of all “failed transactions” (BADTX), which is technospeak for “withdrawals where the money is gone from the client’s account but where the funds were not actually transferred to the client”. The total of such withdrawals, a total that has been steadily climbing since about January 25, has now reached 41,390. That amount is in bitcoin, and each bitcoin is worth $934 by MtGox’s own rate, making the disappeared client money exceed 38 million US dollars. That’s not exactly small change.

MtGox’ twitter account as of noon on Feb 4. It’s full of autoreplies, the newest response to a client being one month old.

Three years ago, I highlighted exchanges as one of four areas where the bitcoin community positively must improve to go mainstream. The above problem of the missing 38 million dollars is exacerbated by the fact that MtGox does not respond to clients’ questions until well over a week has passed, at which point a canned autoresponse is given. Additionally, there has not been any communication whatsoever about the ongoing problem. The lack of a phone number, the non-responses to client concerns over tens of millions of missing dollars, and the complete absence of messages about the situation does not make a professional operation.

Instead, clients of tens of millions of dollars are left on their own trying to figure out what is going on, if they’ll get their funds or not, and if so, when, and what the underlying problem could possibly be.

(I was recently asked by the Wall Street Journal in what ways MtGox failed to live up to Wall-Street-level professionalism, and declined to respond at the time. This is one of those ways. There are others, that are worse, that I have not published yet. That WSJ article concerned delays in withdrawals to dollars and euros, which could be explained by legacy-banking inertia; up until ten days ago, MtGox had executed bitcoin withdrawals perfectly.)

Looking at the bitcoin services forum, there are tons of complaints with the current exchange services. The entrepreneur should identify several opportunities here, just by looking at the front page of “discussions”, which read more like outraged complaints – mostly about MtGox.

As of February 4, clients are left speculating in these threads what the reason for this behavior is – whether it’s legitimate technical problems coupled with abysmal communication, deliberate fraud, possible insolvency, a technical attack on MtGox, or a number of other theories.

DISCLOSURE

The author is personally affected by MtGox’ behavior, having a six-figure dollar amount in such non-executed withdrawals. He considered Gox to be a safer repository for bitcoin than his own probably-hackable computer. That judgment may not have been accurate.

UPDATE 1: One hour after this article was published, MtGox broke the week-long silence with a statement saying little more than “we’re working on it”. In the statement, they also claim that the problem applies “primarily to large transactions”, a statement that doesn’t seem entirely correct when compared to client statements and testimonies on the bitcoin forums.

UPDATE 2: Three days after this article was published, on Friday Feb 7, MtGox disabled bitcoin withdrawals entirely in order to, according to them, sort out their problems. They’ve promised to return with a statement Monday as to how that went.

Exchange is refusing to give customers their money, CEO is at large, and company faces "significant losses"

Early Friday morning Tokyo, Japan-based Bitcoin exchange Mt. Gox froze customers accounts, refusing to give customers their money back. Customers were still allowed to trade the Bitcoins in their accounts for other currencies, Mt. Gox's primary function.

But this problem has been snowballing for nearly a year now. And it’s amazing that no one has recognized this for what it is -- a digital age bank run.

I. The Building is Ablaze, Get Out Now

But reports are largely missing that Mt. Gox appears to be seeing the first major digital bank run and that nearly 1 million users are at risk.

In the last day, panicked customers carried out $32M USD of transactions on the site, nearly five times the normal daily volume. And there are growing signs that customers may get only partial repayment if anything, as Mt. Gox has taken to largely refusing to give customers their money back unless they pay a withdrawal fee "to expedite the transaction".

The exchange, once the biggest converter of Bitcoins to USD and vice versa, blamed it all on a glitch in a press release. It's previously tried to claim that its backing bank in Japan was limiting it to 10 wire exchanges a day, hence why it was taking weeks or even months to give customers their money.

But it hasn't mentioned that claim in while. It appears Mt. Gox is trying to use whatever excuses it can think up to disguise the serious problem -- it may not be able to pay back customers unless its current owner and CEO taps into his own fortune.

A drawing depicts a banker trying to offer reassurances to customers during a bank run in Montreal in 1872. [Image Source: Wikimedia Commons]

In a post it writes:

During our efforts to resolve the issue being encountered by some bitcoin withdrawals it was determined that the increase in withdrawal traffic is hindering our efforts on a technical level. As to get a better look at the process the system needs to be in a static state.

In order for our team to resolve the withdrawal issue it is necessary to temporarily pause all withdrawal traffic to obtain a clear technical view of the current processes.

We apologize for the extremely short notice, but as of now all bitcoin withdrawals will be paused, and withdrawals in the queue will returned to your MtGox wallet and can be re-intiated once the issue is resolved. Customers can still use the trading platform as usual.

Our team will be working hard through the weekend and will provide an update on Monday, February 10, 2014 (JST).

Again, we apologize for the inconvenience, and ask for your continued patience and support while we work to resolve this issue.

But that is a highly suspicious claim, given the run on withdrawals on the site and its serious monetary losses.

Anyone with a basic economics background will recognize the shutdown for what it is -- a desperate attempt to survive in the midst of a digital age bank run. Banks typically keep only a small fraction of customer assets in liquid form, ready for withdrawals. A bank run occurs when a large number of withdrawals overwhelm a bank's capacity to liquify its holdings.

Even a relatively healthy and well-run bank can suffer a bank run in times of severe economic crisis. But bank runs can also be triggered by problems with the bank itself -- monetary losses, reputation damage, and failing to operate transparently. It appears that the Mt. Gox run falls under this category of individual run.

Some may be confused. Isn't Mt. Gox a currency trader? Indeed, it is. But Mt. Gox also stores consumers' currency and thus is acting essentially as an online bank. If anyone has doubts that a run of occurring they should read up on "suspension of convertibility" -- which is precisely what Mt. Gox has been doing for almost a year now with increasing frequency and severity. This tactic is a hallmark of a bank trying to disguise the dire crisis of a bank run.

In the U.S. banks are required to pay for insurance via the U.S. Federal Deposit Insurance Corporation (FDIC), which has largely prevented customers from losing the money they deposit. By contrast, Mt. Gox -- as a registered foreign money trader -- carries no such insurance. As this bank run worsened customers may be forced to turn to class action lawsuits and other mechanisms, but the reality is that Mt. Gox is likely to go under and its customers may lose a substantial part of their holdings.

A bank run in Berlin in 1931 draws a panicked crowd. [Image Source: Biln]

One thing is for sure: things appear to be going downhill fast for Mt. Gox, and its million or so serious customers may face millions in real-world USD losses as the digital bank-run and Mt. Gox's refusal to give customers back their money escalates.

II. "Where's My Money?"

There's widespread media reporting on the Mt. Gox withdrawal freeze announcement from this week, but what most are missing is that the exchange in the last two months has rejected most customer withdrawals silently. This is not a new development; signs of Mt. Gox's insolvency have grown since last year.

"Nope, you can't have your money back." -- that's what Mt. Gox began to tell customers last year. [Image Source: eVoorhees]

Most serious Bitcoin veterans have already fled the exchange, but for those who are still hanging out at Mt. Gox, it's important to recognize that your assets are in extreme danger.

Users are left wondering whether this is simply minor technical glitch, the first hint at another security compromise, or signs that Mt. Gox may be treading dangerously close to insolvency.

Confidence in Mt. Gox was once strong.

Founded in 2010, Mt. Gox quickly grew to dominate a far greater portion of the overall Bitcoin trading volume than it does today. Its troubles began shortly after its original owner Jed McCalebsold the Tokyo, Japan based web portal to new owners in March 2011.

The 2011 hack of Mt. Gox triggered a plummet in trading prices. [Image Source: LeanBack.eu]

While some in the Bitcoin community pushed legitimacy as the cybercurrency grew in usage and values, Mt. Gox paid a steep price last year for stubbornly resisting such efforts. In February it became embroiled in a feud with online payments firm Dwolla over Dwolla's new restrictions that cracked down on money laundering.

Then in April 2013 Mt. Gox announced the first of several "cool down" periods. Trading shut down for at least a day in April, and during another shutdown buying (order placing) was halted.

III. Mt. Gox Has Admitted to "Significant [Financial] Losses"

In May 2013 Mt. Gox's financial troubles grew when CoinLab sued Mt. Gox. Mt. Gox has previously partnered with the U.S. startup, which had allegedly promised it exclusive rights to run trade in the U.S. under the Mt. Gox brand. But to CoinLab's chagrin, Mt. Gox continued to directly trade to U.S. buyers. CoinLab sued it for $75M USD writing that the figure "likely underestimates the actual damages."

Meanwhile the damages to Mt. Gox were growing. In May the U.S. Department of the Treasuryseized an estimated $5M USD in accounts belonging to Mt. Gox's owners. Some of these funds were reportedly returned by the Financial Crimes Enforcement Network (FinCEN) -- the enforcement arm of the Treasury -- after Mt. Gox registered in June 2013 as a money exchange, agreeing to file paperwork and finally crack down on overt money laundering.

Mt. Gox CEO Mark Karpeles holds up a commemorative Bitcoin medallion.

But its woes were growing. Customers began complainingin forum posts that throughout mid-to-late 2013 Mt. Gox was denying their request to transfer their funds to other exchanges or back into their wallets. Customers were greeted by messages such as "your withdrawal is yet to process. we will keep you posted once it is done."

Mt. Gox further stoked the flames when it introduced a 5 percent fee for "expedited" withdrawals (which are normally free). Some users tried the service and declared it a scam, after seeing their withdrawals still languish for weeks unfilled.

In June Mt. Gox CEO Mark Karpeles -- the man who had purchased the company back in 2011 --disappeared from popular Bitcoin forums and other online sites. This was yet another troubling sign, given that previously he had been a very active participant in a number of online communities, evangelizing Mt. Gox.

After accumulating a quarter-billion dollar fortune, Mt. Gox CEO has reportedly vanished from the digital doman. [Image Source: Reuters]

In Aug. 2013 Mt. Gox admitted it was in serious financial trouble, saying it had seen "significant losses" from unfulfilled transactions. A release to customers at the in December 2013 noted the company had only a million current customers -- less than an eighth of the accounts that were registered with it in 2011.

That's not to say the company hasn't seen some gains, as well. In April 2013, it was doing about $6M USD worth of trades a day, according to Bitcoin Charts. In the past day it was average $7.8M USD in volume -- a modest growth in value driven by the rising value of the Bitcoin.

However, last April it was handling 76 percent of transactions, in the last month it handled only 19 percent of transactions. It is currently the third biggest exchange behind BitStamp and btc-e -- the first and second place exchanges, respectively, in terms of volume in the last 30 days.

IV. Bitcoin, Other Cryptocurrencies, Must Adopt Insurance or Risk Losing Everything in Bank Runs

Introduced in 2008 by a programmer or group of programmers using the pseudonym Satoshi Nakamoto, the Bitcoin was the first of its kind, turning the science fiction fantasy of a decentralized, encryption-based global currency into reality.

Despite recent largely overstated and misinformed controversy over illegal uses of the Bitcoin, the cryptocurrency is the foundation of a generally credible and secure global digital payment network. While other cryptocurrencies have since emerged, Bitcoin remains the most prominent with a market value of over $10B USD. Blockchain estimates Bitcoin has roughly 1.2 million users, working out to an average wallet value of around $10,000 USD.

Bitcoins are the world's most popular cryptocurrency, used by over a million people worldwide [Image Source: Bit-Square]

In this moment of need Mt. Gox CEO is oddly silent, with some sources saying he has disappeared. He has good cause to want to escape the mess, as he has plenty to lose. Fueled by Mt. Gox's fees (e.g. 10 percent for many exchanges) he amassed a fortune of $8M USD plus and 345,000 Bitcoins (at current rates: $250M USD). Even with the FinCEN seizures, he likely has a quarter of billion dollars in assets. It would not be surprising to see him disappear altogether if Mt. Gox sees a full collapse.

The good news is that a relatively small slice of the Bitcoin community will be affected by this run.

But ultimately, this somewhat unprecedented saga may affect the entire Bitcoin market. If Mt. Gox fails to pull off a miracle and show itself to indeed be soluble, the run will likely only worsen. And if Mt. Gox defaults and goes under, that will cast a dark light on the entire cryptocurrency global phenomena, perhaps forcing cryptocurrency developers to band together to introduce some form of collective insurance.

Volatility at MtGox continued throughout the weekend with BTC/USD again testing the 660 to 670 support level. After making a small dead cat bounce to 720 yesterday, the pair is once again glued to support. The likely course of action is further move to the downside.

In the statement released few days ago MtGox said that they will provide an update on Monday. It remains to be seen what happens to bitcoin prices at Gox if the situation turns out to be just ‘’technical difficulties’’ and people are allowed to withdrawal bitcoins again. Due to the inability to withdraw fiat currency, one would assume that btc prices would spike as a flood of traders sell their USD and buys bitcoins so that they can withdraw from the exchange.

This isn’t what the market is telling us unfortunately. The spread between MtGox and the rest of the exchanges is currently at negative – 30 points. One bitcoin trades at 676 on Gox, that same bitcoin is currently worth 705 on Bitstamp and 715 on BTC-E. Market participants seem to be pricing in something more sinister than simple technical issues. Of course this could just be fear on the part of traders and the whole situation could be resolved on Monday. The exchange has shown severe incompetence in the past, this certainly wouldn’t be the first time ‘’technical issues’’ caused problems or stopped trading altogether. After all, that’s why the term GOXED is in the urban dictionary. Stay safe.

Mt. Gox CEO Mark Karpeles. Image: A screenshot from a 2013 Reuters video.

It was once the only serious bitcoin exchange on the internet. But now, just a year later, Japan’s Mt. Gox is in shambles.

U.S. regulators have seized more than $5 million of the company’s money. Customers report month-long delays in getting their U.S. dollars out of the exchange. And now a technical glitch has prevented the exchange from paying out in bitcoins too, effectively locking away customer assets until further notice.

Early Friday morning, Mt. Gox said it needed to suspend Bitcoin payouts in order to fix a technical glitch in its trading platform. The company promised an update on Monday, but didn’t explain exactly what the issue was. Over the past week, complaints about Mt. Gox’s bitcoin payout problems have gown louder as the queue of unfulfilled withdrawals has grown longer and longer.

The company’s situation shows that some of the earliest businesses to embrace the bitcoin digital currency are now struggling to adapt now that the technology is moving into the mainstream. As more and more people use bitcoin — and regulators begin to take notice — an outfit like Mt. Gox, which is run by computer geeks, not financial experts, has a tough row to hoe.

‘It seems very likely to me that for some reason Mark Karpeles is not able to work on his codebase anymore, and isn’t able to resolve bugs in a timely manner, leaving his support staff to try and clean up the mess by making horrible hacks’

— Mike Hearn

Over the past year, Mt. Gox has lost its position as the world’s top bitcoin exchange to new players such as Bitstamp and BTC-China, but the Gox crash is still a big black-eye for bitcoin. Mt. Gox CEO is a board member of the Bitcoin Foundation, a non-profit advocacy group that promotes the digital currency.

It’s a sign of a changing of the guard in the bitcoin world, as old players are being elbowed out by new more professional companies. In the United States, the easiest way to buy and sell bitcoins is through a company called Coinbase. They’re backed by well heeled venture capitalist firm Andreessen Horowitz. Another company, called Buttercoin is expected to launch soon. They’re building open-source bitcoin exchange software.

Glitch or Liquidity Crisis?

Although bitcoin’s price initially dropped more than $100 — to below $700 — Friday morning on fears of a Gox liquidity crises, trades started edging back up later in the day on speculation that the problems are really due to a technical glitch, and not a lack of bitcoins.

“It seems very likely to me that for some reason Mark [Karpeles] is not able to work on his codebase anymore, and isn’t able to resolve bugs in a timely manner, leaving his support staff to try and clean up the mess by making horrible hacks like “throw away and retry later’,” wrote Mike Hearn, a respected Bitcoin developer on a Bitcoin Foundation discussion forum “The question in my mind then becomes – where is Mark and what is he doing?”

One Redditor says he flew from Australia to Japan in an attempt to withdraw his bitcoins. He met Karpeles in front of the Gox office, but never got his money back. Mt. Gox does not typically respond to media inquiries, and it did not reply to an email seeking comment for this story.

BTC-e Pulls Support for Ruble As Russia Bans Bitcoin

Bulgarian bitcoin exchange BTC-e has pulled support for the ruble, following a decision by the Russian Prosecutor’s Office to ban bitcoin.

A statement issued by Russia’s General Prosecutor’s Office said that it saw growing interest in the cryptocurrency, including from money launderers.

“The official Russian currency is the ruble. The use of any other monetary instruments or surrogates is forbidden,” it said, citing Russian Article 27 of Russia’s Federal Law, regarding the Central Bank of Russia.

The announcement is the clearest indication yet of its position regarding cryptocurrencies.

“The anonymous payment systems and crypto-currencies, including bitcoin – which is the most popular of them – are monetary surrogates. As such, their use by private citizens or legal entities is not allowed.”

BTC-e withdraws ruble support

In response, BTC-e announced that it would discontinue support for the ruble.

“In connection with decision-making in relation to the crypto-currency in Russia working with QIWI suspended indefinitely, as well as with other payment systems in Russia,” said the exchange, in a (translated) news posting only visible for those with their locale set to Russia.

“The official Russian currency is the ruble. The use of any other monetary instruments or surrogates is forbidden.”

“All financial obligations are met in full means available without commission.

Recommend that you use the systemOKPAY (USD, EUR), interest on the conclusion on it is reduced to zero.

We apologize for any inconvenience.”

In the last few days, BTC-e had reported some technical work on its QIWI interface. BTC-e did not respond to queries, but as of this evening UK time, there was no ‘deposit’ option for rubles on BTC-e’s account management pages.

Russia’s decision to ban bitcoin was made at a meeting of an inter-agency working group this week.

Attendees included the deputy chair of the Central Bank of Russia, and heads of relevant departments of the Bank of Russia. Officials from the Russian FSB and the Russian Interior Ministry were also there.

In short, the decision has widespread support.

The Prosecutor’s Office also discussed enforcement options, explaining that it was planning specific steps to choke off the distribution of cryptocurrencies in the country. There will be another meeting of the expert group, to discuss implementation options, the statement said.

Market impact

This development wasn’t unexpected, although the speed and strength of escalation is surprising. The Bank of Russia issued a warning in late January, also citing Article 27, and warning that the issuing of cryptocurrencies in the Russian Federation was illegal.

The head of Sberbank, the third-largest bank in Europe, has been bullish on bitcoin, affirming his support as recently as late January. But, the Bank of Russia is the state bank and a powerful institution that mirrors government policy.

That, along with the Russian news, is doubtless what sent prices plummeting today. The price had levelled out on 6th February after dropping around 4.5% to $804. Then, on 5th February at around 5:30 UK time, it began dropping drastically, reaching around $664 at 8am today. Twelve hours later, a rally appeared to have faltered, as prices dropped again.

At the time of posting, the Coindesk Price Index stood at around $729.

LocalBitcoins.com Users Face Criminal Charges in Florida

At least two men in Florida have been charged for moving large volumes of bitcoins via the popular person-to-person exchange LocalBitcoins.com. They were charged under state anti-money-laundering laws following an investigation by the US Secret Service, said reports.

Security blogger Brian Krebs reportedthat Michell Abner Espinoza of Miami Beach was arrested after a sting in which an undercover agent engaged him in a fake transaction to convert $30,000 worth of cash into bitcoins.

In addition, 29-year-old Pascal Reid was also arrested after meeting with an undercover agent to exchange $30,000 for bitcoins.

The charges

Both of the men are being charged under two laws. The first is Florida’s anti-money laundering law, which targets money exchanges above $10,000.

The second is running an unlicensed money transmission business. Statute 560.125 forbids people from exgaging in frequent unlicensed money transmission-type transactions of more than $300 but less than $20,000 in any 12-month period in the state.

Depending on the amount involved, it is considered a felony of the third, second, or first-degree. Exchanging more than $100,000 in funds during any 12-month period is considered a first-degree felony. Fines of twice the currency value, up to a value of $250,000, are possible.

Espinoza, said to go under the name MichaelHack on LocalBitcoins.com, had trades involving more than 150 bitcoins in the last six months, say reports.

Headquartered in Finland, LocalBitcoins.com is a person-to-person trading website, which facilitates trades both online and in person. Unlike exchanges that automatically reconcile trades using an online order book, exchanges like LocalBitcoins.com let users find each other, and handle the trades themselves. The site has been gaining popularity rapidly in recent months, adding roughly 1,000 users each day.

LocalBitcoins reacts

Jeremias Kangas, the owner of LocalBitcoins.com, wasn’t aware of the charges when contacted by CoinDesk. He explained that the site relied on users to follow the laws in their own countries when conducting trades. “That’s our guideline. But it’s quite difficult for us to look after everyone,” he said.

Currently, users are expected to verify each other themselves when handling in-person trades, Kangas noted. The company has been working on a central verification system, although that has not yet been implemented.

“This is inevitable of course,” said Kangas of the Florida incident. “We have to have more scrutiny and tools to watch that everything on our website is legal, and our users can follow their local laws. We are spending a lot of resources on that, but we are a startup.”

Localbitcoins.com does not limit the size of trades, admitted Kangas. “That might be possible, actually. We haven’t thought about that,” he said.

Next steps

Espinoza had his bond hearing today, and faces three charges; two related to money laundering amounts under $20,000 and between $20,000 and $100,000. The third charge relates to money transmission services for amounts between $20,000 and $100,000.

Reid’s case details were not yet on file at the time of writing, but he is being tried for unlicensed money transmission services on a third degree felony.

State authorities in Florida on Thursday announced criminal charges targeting three men who allegedly ran illegal businesses moving large amounts of cash in and out of the Bitcoin virtual currency. Experts say this is likely the first case in which Bitcoin vendors have been prosecuted under state anti-money laundering laws, and that prosecutions like these could shut down one of the last remaining avenues for purchasing Bitcoins anonymously.

Working in conjunction with the Miami Beach Police Department and the Miami-Dade State Attorney’s office, undercover officers and agents from theU.S. Secret Service’s Miami Electronic Crimes Task Force contacted several individuals who were facilitating high-dollar transactions via localbitcoins.com, a site that helps match buyers and sellers of the virtual currency so that transactions can be completed face-to-face.

One of those contacted was a localbitcoins.com user nicknamed “Michelhack.” According to this user’s profile, Michelhack has at least 100 confirmed trades in the past six months involving more than 150 Bitcoins (more than $110,000 in today’s value), and a 99 percent positive “feedback” score on the marketplace. The undercover agent and Michelhack allegedly arranged a face-to-face meeting and exchanged a single Bitcoin for $1,000, a price that investigators say included an almost 17 percent conversion fee.

According to court documents, the agent told Michelhack that he wanted to use the Bitcoins to purchase stolen credit cards online. After that trust-building transaction, Michelhack allegedly agreed to handle a much larger deal: Converting $30,000 in cash into Bitcoins.

Investigators had little trouble tying that Michelhack identity to 30-year-old Michell Abner Espinoza of Miami Beach. Espinoza was arrested yesterday when he met with undercover investigators to finalize the transaction. Espinoza is charged with felony violations of Florida’s law against unlicensed money transmitters – which prohibits “currency or payment instruments exceeding $300 but less than $20,000 in any 12-month period” — and Florida’s anti-money laundering statutes, which prohibit the trade or business in currency of more than $10,000.

Police also conducted a search warrant on his residence with an order to seize computer systems and digital media. Also arrested Thursday and charged with violating both Florida laws is Pascal Reid, 29, a Canadian citizen who was living in Miramar, Fla. Allegedly operating asproy33 on localbitcoins.com, Reid was arrested while meeting with an undercover agent to finalize a deal to sell $30,000 worth of Bitcoins.

Documents obtained from the Florida state court system show that investigators believe Reid had 403 Bitcoins in his on-phone Bitcoin wallet alone — which at the time was the equivalent of approximately USD $316,000. Those same documents show that the undercover agent told Reid he wanted to use the Bitcoins to buy credit cards stolen in the Target breach.

Nicholas Weaver, a researcher at the International Computer Science Institute (ICSI) and at the University of California, Berkeley and keen follower of Bitcoin-related news, said he is unaware of another case in which state law has been used against a Bitcoin vendor. According to Weaver, the Florida case is significant because localbitcoins.com is among the last remaining places that Americans can use to purchase Bitcoins anonymously.

“The biggest problem that Bitcoin faces is actually self-imposed, because it’s always hard to buy Bitcoins,” Weaver said. “The reason is that Bitcoin transactions are irreversible, and therefore any purchase of Bitcoins must be made with something irreversible — namely cash. And that means you either have to wait several days for the wire transfer or bank transfer to go through, or if you want to buy them quickly you pay with cash through a site like localbitcoins.com.”

One very popular method of quickly purchasing Bitcoins — BitInstant — was shuttered last year. Last month, BitInstant CEO Charlie Shrem was arrested for money laundering, following allegations that he helped a man in Florida convert more than a million dollars in Bitcoins for use on the online drug bazaar Silk Road.

It’s still unclear how the defendants Espinoza and Reid were able to obtain so many Bitcoins for sale, although a review of Michelhack’s profile suggests little more than arbitrage — that is, buying Bitcoins for $700 apiece and selling them for a couple hundred dollars more.

Weaver said he anticipates that more states will soon seek to crack down on high-dollar Bitcoin sellers on localbitcoins.com. “I’d expect many more state cases like this one because it will act to strangle the lifeblood of the online dark markets,” such as Silk Road, Weaver said. “If you want a significant amount of anonymous Bitcoins, right now this community is about the only mechanism still available.”

News of the Florida actions comes on the heels of the arraignment of Ross Ulbricht — the alleged onetime owner of the Silk Road. Ulbricht was scheduled to be arraigned in New York today.

The court documents in this case also offer a great example of the traceability of Bitcoin transactions — a potential danger for both those seeking anonymous payments and for law enforcement officials posing as criminals as part of an undercover investigation. The ICSI’s Weaver noted that, by examining the times and transactions in the criminal complaint, it appears that this is the Bitcoin wallet associated with the undercover officer.

Coinbase Moves to Calm Security Concerns Amid Theft Reports

Andreessen Horowitz-backed bitcoin wallet provider Coinbase confirmed via a company blog post on 7th February that “a small handful” of its customers have fallen victim to phishing attacks.

The reports of bitcoin wallet security vulnerabilities, however small, have nonetheless reverberated widely in an industry that is being increasingly cast in a shroud of uncertainty by the mainstream media.

A separate account of the incidents by online news source The Verge paints a very different picture of the situation, suggesting that the thefts, while in some cases the fault of Coinbase‘s users, were sizable and perhaps more frequent than has been reported.

The Verge confirmed what it called “a string of Bitcoin thefts that have hit the service in recent weeks”.

In its piece, it profiled the story of a Coinbase user named Jeff, who lost 10.6 BTC in bitcoins due to theft this December. What’s most unique about Jeff’s story, however, is that one month later, his refunded money was stolen from the service yet again.

The media outlet revealed that it has confirmed two separate thefts occurred to users on the service, for amounts of $16,000 and $5,000, respectively. The sum total of the thefts, as noted in the piece, is roughly $40,000.

The extent of the attacks

The security firm FireEye told the Verge that it believes it is unlikely that Coinbase suffered a system-wide vulnerability, and that instead, each individual victim was compromised in isolation.

However, it suggested that Coinbase’s “unusually powerful” API may have been a factor:

“The right API key will let any program move bitcoins in and out of a given accounts. Once the key is compromised, attackers can even access linked bank accounts to purchase more bitcoins. Users are advised not to authorize the API key if they don’t need it, but if an account has been compromised, hackers may decide to authorize it themselves.”

FireEye did suggest that the company itself does not seem responsible for the attacks, which were not aimed at its infrastructure. Further, they suggested that Coinbase’s user agreement clearly states that individuals are responsible for the safety of their private keys.

By using the wallet provider’s two-factor authentication, the report suggested, Jeff could have prevented the loss of his API key, which once compromised may have been reactivated by the hackers.

Coinbase reacts

The San Francisco-based company downplayed the thefts, stating that “phishing is unfortunately a common across the Internet”, and noting that it affects banking institutions, payment processors and retailers in the traditional financial system as well.

Further, the company indicated that, because of the concern over phishing attacks, it has implemented enhanced security measures, that when used with best practices for web surfing, can help limit these occurrences:

“We’ve implemented a number of increased security measures, including expanded two-factor authentication measures designed to help lessen the likelihood of successful phishing incidents in the future. We’ve also added an email verification step for key actions, such as when an API key is enabled.”

Coinbase representatives denied further requests for comment, stating that the blog post represented their official position on the attacks.

[UPDATED on Feb.06 17:45 GMT with information on the technical error]

[UPDATE 2 Feb.07 07:48 GMT : Mt.Gox has released a more detailed statement saying all withdrawals are halted to be able to fix the problem, promising further updates on Feb.10th.]

[UPDATE 3 Feb 07 11:17 GMT: The details of the bug have been explained by Bitcoin developer Gregory Maxwell on Reddit. In essence it is a combination of a design flaw in the Bitcoin protocol coupled with the way the custom Mt.Gox software handles transactions.]

Withdrawing USD from Bitcoin Exchange Mt.Gox already used to take anything from weeks to months, but it is now becoming similarly difficult to withdraw Bitcoins.

As of Feb.06, over 50.000 (50k) Bitcoins ( ~40 MIO USD) are “stuck” inside of Mt.Gox according to their own data, collected by Coinsight and “The Gox Report”, and this number is growing fast. While being inflated due to the “change” of transactions, and possibly being closer to 20-30k, just the rate at which this amount is rising is a cause for concern.

The problem became apparent around the 25th of January, when a rapidly growing number of users started voicing their concerns on Bitcointalk , Reddit and Twitter. Some users report waiting over a week to be refunded for failed withdrawals, only to have the transaction fail again on the next attempt.

While some withdrawals seem to go through, the overall success rate as stated by users, and backed up by data from Mt.Gox and IRC support, seems to be below 30%.

The official statement by Mt.Gox is that they are aware of the problem and are working hard to fix it, but is providing no further information.

[UPDATE: Sources close to Mark Karpeles claim progress has been made on finding the cause of the problem, pointing to a misinterpretation of the wallet software as to which outputs are already spent. It is further claimed that he has personally confirmed this error, and progress is being made in fixing it. Due to security concerns the details cannot be disclosed here, as other wallets might be affected.]

This has lead to speculation about the situation of Mt.Gox, with even members of the Bitcoin Foundation asking for clarification and for Gox’ CEO, Mark Karpeles, to step forward.

Karpeles has so far not commented on the issue, and is apparently not even in touch with fellow members of the Foundation, of which Mt.Gox is one of the two only “Gold” members.

Looking at the transactions inside of Mt.Gox wallets via the “Skanner” website reveals a tangled mess of interdependent double spends, causing whole chains of transactions to fail over time.

According to Bitcoin Developer Mike Hearn, Mt.Gox is running a customized version of the Bitcoin software which is maintained by Karpeles himself, and the ongoing problems are leading to the assumption that for some reason he is currently unable to fix it.

With support tickets not being answered, their Twitter & Reddit support sending out prefabricated messages, and their IRC support being overloaded, speculation is running wild about the true nature of their problems, including that the technical problems might be intentional to mask underlying problems. However, support in IRC keeps stating that the problem is being worked on, that Mt.Gox is running a full-reserve operation, and all coins are safe and will be paid out.

Even if these are just errors in the software, Mt.Gox’ failure to properly communicate the issues is alarming in itself, and is already showing to be eroding trust in the exchange, as an increasing number of customers is trying to leave.

At the time of writing Bitcoin prices have been tumbling, with Mt.Gox rates dropping up to 15% in what seems to be Bitcoins first Bank run.

With Bitcoin slowly gaining legitimacy around the world, one stands to question the way Mt.Gox is handling this problem, and whether the Bitcoin Foundation is watching their members to uphold the standards and level of professionalism they have ascribed to themselves.

The current situation can only be defused by either fixing the problems within the next days, or by Mt.Gox stepping up and providing evidence of having enough funds, and giving clear information about the exact nature of the technical problem. It would be in the best interest of Mt.Gox, as well as the Bitcoin Foundation, to step up and address this problem openly and transparently, as the speculation alone might prove detrimental to the further evolution of the emerging Bitcoin economy.

Following Mt. Gox Sell-Off, Cyprus Warns of Bitcoin’s Volatility

The Central Bank of Cyprus (CBC) issued a warning on 7th February to its 1.1 million residents advising them that virtual currencies such as bitcoin are not legal tender and should be treated with caution because of their perceived volatility.

The CBC further noted in its statements that it does not condone any activity that falls under its jurisdiction, “unless it can ensure the legality of that activity”. The agency added:

“Activities without the necessary licensing are in breach of legislation.”

Elsewhere, the CBC reminded its citizens to be cautions about virtual currency investments, and to “examine all aspects of the use of virtual currencies” before electing to invest.

The announcement is particularly noteworthy as it comes less a day after Mt. Gox halted withdrawals, causing the price of bitcoin to experience its largest fluctuations in weeks. Further, the Cyprus banking crisis is largely credited with the spike in interest in bitcoin in March of 2013, and the nation is often cited as being a market where a solution such as virtual currency might become widespread.

Lack of regulatory safeguards

The CBC used the release to remind citizens about the volatility of virtual currency, perhaps in response to the decision by major Japan-based exchange Mt. Gox to abruptly suspend services this week. The release included references to the posibility that virtual currency “platforms or exchanges” could collapse, putting citizens at risk.

“In particular, the public should be aware that there are no regulatory safeguards to cover losses from using virtual currency,” the release stated.

The statement went on to name four major risks associated with virtual currencies:

There are no consumer protections for those invested in virtual currencies

The value of virtual currencies may rise, fall or be eliminated

The trade of virtual currencies helps facilitate criminal activities

The acceptance of virtual currencies can be revoked at any time.

Fertile ground for bitcoin

The Cyprus government was at the center of international controversy in 2013 after it decided to adopt a “bail-in” strategy to deal with its struggling banks. As part of this initiative, authorities transferred all assets under €100,000 to the CBC and instituted 47.5% losses on deposits exceeding this benchmark.

However, bitcoin and virtual currencies soon emerged as a potential solution.

“The most fertile ground for bitcoin is in places like Cyprus, Argentina, Iceland, China and other countries which have experienced significant financial disruptions and/or maintain strict financial controls,” Garrick Hileman, economic historian at the London School of Economics, told CoinDesk this November.

Those with more conservative and libertarian financial ideologies responded as well.

“Bitcoins were growing slowly until Cyprus. Cyprus was the catalyst for the big increase in the price. The price started trading at about $40 and then doubled within a couple of days.”

Whether this announcement will have any affect on bitcoin’s growth in the country, remains to be seen.

Mt. Gox Halts ALL Bitcoin Withdrawals, Price Drop Follows

UPDATE (7th February, 11:25 GMT): Users with bitcoin withdrawals in limbo have reported that the amounts are being returned to their Mt. Gox wallet balances.

Japan-based bitcoin exchange Mt. Gox, the third-largest for trading the US dollar for bitcoin by 30-day volume, has announced it is temporarily pausing bitcoin withdrawals.

During our efforts to resolve the issue being encountered by some bitcoin withdrawals it was determined that the increase in withdrawal traffic is hindering our efforts on a technical level. As to get a better look at the process the system needs to be in a static state.

In order for our team to resolve the withdrawal issue it is necessary to temporarily pause all withdrawal traffic to obtain a clear technical view of the current processes.

We apologize for the extremely short notice, but as of now all bitcoin withdrawals will be paused, and withdrawals in the queue will returned to your MtGox wallet and can be re-initiated once the issue is resolved. Customers can still use the trading platform as usual.

Our team will be working hard through the weekend and will provide an update on Monday, February 10, 2014 (JST).

Again, we apologize for the inconvenience, and ask for your continued patience and support while we work to resolve this issue.

Best regards,

The MtGox Team

Mt. Gox has been suffering from lengthy delays transferring bitcoin to USD and transferring to US bank accounts for some time now, but similar issues recently extended to those looking to withdraw fiat values in other major currencies like euro and Japanese yen.

The Bitcoin Price Index, which currently includes Mt. Gox (as well as Bitstampand BTC-e) shows the bitcoin price starting to drop last night, and falling a further $75 from today’s open down to $709 at the time of writing.

Bitcoin-specific withdrawal problems

Most recently Mt. Gox’s issues with getting money out of the exchange have extended even to withdrawals in actual bitcoin.

Reports of sporadic difficulties withdrawing BTC from Mt. Gox began to trickle in as early as late December, but increased in the 72 hours leading up to this announcement.

At first, users reported getting an erroneous “Invalid Bitcoin Address” error message when attempting to transfer – something that has happened several times in the past and is said to be due to the exchange’s ‘hot wallet’ running dry in times of great demand.

Even supposedly successful transactions, which the Mt. Gox website will have claimed to have occurred, often do not register on bitcoin’s public block chain. One user, who tried this morning to withdraw a substantial amount of bitcoin, told this story:

I had BTC sitting in my Gox account for a few weeks then decided to transfer to my home PC wallet. I had transferred BTC to and from Mt Gox several times since November last year without any problems. On Feb 4th at 2:15pm I made the transfer unaware that others were already experiencing problems with ‘stuck’ transactions. After I committed the transfer, the Gox website immediately issued a transaction hash and deducted the BTC plus a fee from my account. When I checked several hours later that transaction hash was not found on the blockchain. Needless to say, nothing has appeared in my wallet.

I raised three support tickets but none have yet been assigned to an agent. When I search google for “Mt. Gox BTC withdrawal problem” I find there are hundreds of people with the same or similar issues.

Even smaller withdrawals were affected, with other users reporting similar stories when attempting to withdraw amounts of less than 1 BTC.

Graphs on Bitcoincharts.com showed bitcoin trading volume increasing markedly over the past 24 hours or so. At the time of writing, since midnight on the 6th February UTC, over 45,084 BTC has been traded on Mt. Gox – compared to only 11,348 in the entire 48 hour period before that.

source: bitcoincharts.com

Coinsight.org, which tracks data based on each exchange’s public API, showed an hourly increase in Mt. Gox’s BTC withdrawal volumes and ‘stuck’ withdrawals until 13:00 Japan time, when there was a vertical drop. Numbers began rising again almost immediately after.

Many users had thought their bitcoin balances were relatively secure, at least compared to national currency amounts, and could be transferred to a local wallet at a moment’s notice. Mt. Gox has not indicated there will be any difficulty doing that once its technical problems are ironed out.

This was the expectation, given bitcoin is considered ‘sound money’ by its fans and that Mt. Gox is not a fractional reserve bank subject to problems with a ‘bank run‘ in digital currency. If a bitcoin is listed in a wallet, users presume it may be transferred or withdrawn without delay.

Were Mt. Gox to collapse, or even render itself unreliable as a platform, a large portion of bitcoin trade would either scramble for a new home or disappear altogether, which could have a dramatic effect on bitcoin’s value.

Founded originally by serial tech innovator Jed McCaleb in 2009 as an exchange for Magic: The Gathering Online players, Mt. Gox was turned into a bitcoin-only exchange in 2010 before being sold to Mark Karpeles and his company Tibanne Ltd., the current owner.

Mt. Gox was the largest and, for many, the only bitcoin-fiat currency exchange from bitcoin’s introduction until last year.

While it had endured hacks, price crashes and double-spend crises in the past, it was the most well-known and used exchange for large-scale bitcoin traders until competitors such as Bitstamp, BTC China and BTC-e began to usurp its power.

It accounted for over 70% of global trading volume in April 2013 and its price has traditionally been the highest, apart from certain times in 2013 when BTC China held the record or when Bitstamp managed to overtake it.

A series of misfortunes since April have seen Mt. Gox’s USD trading fall to an 18% market share, just behind Europe’s Bitstamp and BTC-e with 30% and 25% respectively.

Criticism

Although criticisms have often been leveled at Mt. Gox throughout its history and reached a crescendo by the end of 2013, the company has also suffered from external forces.

Following that, in August a Mt. Gox subsidiary in the US, Mutum Sigillum LLC, lost $2.9m in a seizure of its Dwolla account by the DHS. That deparment of the federal government claimed that the company had concealed its business as a money transmitter and failed to register as such with FinCEN.

The DHS seized a further $2.1m from Mt. Gox’s two Wells Fargo accounts in the US, one of them under Mutum Sigillum’s name and one in CEO Karpeles’ own name. Federal testimonies have since revealed the seizures had more to do with users’ Silk Road related activities than FinCEN’s rules.

With $5m in reserves gone, and with US banks and payment processors alike refusing to engage in further business with them, Mt. Gox has since struggled to transfer funds into the US and to its many American customers.

A dispute with another US partner, bitcoin incubator CoinLab, saw Mt. Gox sued for $75m in September 2013. Mt. Gox countersued for $5.5m, claiming CoinLab had also failed to register as a money transmitter and jeopardized the business. The case is still ongoing.

In our efforts to resolve the issue being encountered by various bitcoin withdrawals, it was determined that the increase in the flow of withdrawal requests has hindered our efforts on a technical level. To understand the issue thoroughly, the system needs to be in a static state.

In order for our team to resolve the withdrawal issue it is necessary for a temporarily pause on all withdrawal requests to obtain a clear technical view of the current processes.

We apologize for the sudden short notice. All bitcoin withdrawal requests will be on pause, and the withdrawals in the system will be returned to your MtGox wallet and can be reinitiated once the issue is resolved. The trading platform will perform as usual for the needs of our customers.

Our team will resolve this problem as soon as possible and will provide an update on Monday, February 10, 2014 (JST).

We deeply apologize for the inconvenience caused, and thank you for your kind support and considerations.

Sincerely,

The MtGox Team

Meanwhile, the price of Bitcoin tanked this morning.

Security First International Holdings, Inc. Capitalizing on the Widespread Adoption of Crypto-Currency by Converting Bitcoin to USD through Cryptsbids.com

LAS VEGAS, NV – Security First International Holdings, Inc. a leading provider of mobile financial products and services for consumers, is pleased to provide a trouble-free means to convert Bitcoin to USD through, Cryptsybids.com. Cryptsybids.com, the company’s penny auction auction environment allows players to purchase bids with eligible crypto-currency such as Bitcoin to participate in live auctions and win selected offers and get USD cash back rewards. "With some of the challenges converting Bitcoin into USD through the traditional exchanges, I see this as a great alternative to converting Bitcoin into cash” said Brian Fowler, President. In effort to recognize the issue being encountered by various Bitcoin exchanges, Security First International Holdings, Inc. intends to provide full user control and flexibility for converting Bitcoin to USD cash back rewards with Cryptsbids.com, the first-of-its-kind penny auction environment. Visit Cryptsybids.com to learn more.

Working in conjunction with the Miami Beach Police Department and the Miami-Dade State Attorney’s office, undercover officers and agents from theU.S. Secret Service’s Miami Electronic Crimes Task Force contacted several individuals who were facilitating high-dollar transactions via localbitcoins.com, a site that helps match buyers and sellers of the virtual currency so that transactions can be completed face-to-face.

Working in conjunction with the Miami Beach Police Department and the Miami-Dade State Attorney’s office, undercover officers and agents from theU.S. Secret Service’s Miami Electronic Crimes Task Force contacted several individuals who were facilitating high-dollar transactions via localbitcoins.com, a site that helps match buyers and sellers of the virtual currency so that transactions can be completed face-to-face.

Roger Ver

Roger Ver

Working in conjunction with the Miami Beach Police Department and the Miami-Dade State Attorney’s office, undercover officers and agents from theU.S. Secret Service’s Miami Electronic Crimes Task Force contacted several individuals who were facilitating high-dollar transactions via localbitcoins.com, a site that helps match buyers and sellers of the virtual currency so that transactions can be completed face-to-face.

Working in conjunction with the Miami Beach Police Department and the Miami-Dade State Attorney’s office, undercover officers and agents from theU.S. Secret Service’s Miami Electronic Crimes Task Force contacted several individuals who were facilitating high-dollar transactions via localbitcoins.com, a site that helps match buyers and sellers of the virtual currency so that transactions can be completed face-to-face.

Security First International Holdings, Inc. Capitalizing on the Widespread Adoption of Crypto-Currency by Converting Bitcoin to USD through Cryptsbids.com

ReplyDeleteLAS VEGAS, NV – Security First International Holdings, Inc. a leading provider of mobile financial products and services for consumers, is pleased to provide a trouble-free means to convert Bitcoin to USD through, Cryptsybids.com.

Cryptsybids.com, the company’s penny auction auction environment allows players to purchase bids with eligible crypto-currency such as Bitcoin to participate in live auctions and win selected offers and get USD cash back rewards.

"With some of the challenges converting Bitcoin into USD through the traditional exchanges, I see this as a great alternative to converting Bitcoin into cash” said Brian Fowler, President.

In effort to recognize the issue being encountered by various Bitcoin exchanges, Security First International Holdings, Inc. intends to provide full user control and flexibility for converting Bitcoin to USD cash back rewards with Cryptsbids.com, the first-of-its-kind penny auction environment.

Visit Cryptsybids.com to learn more.