One of the nation’s leading banks wants Congress to amend federal law adopted in the wake of the 2008 financial crisis so it and other Wall Street institutions can go back to gambling with risky investments and have taxpayers cover the losses again if they bet wrong.

Under the Dodd-Frank Act of 2010 (pdf), banks can no longer use monies backed by the Federal Deposit Insurance Corporation (FDIC) to invest in high-risk derivatives, such as “swaps.” This prohibition was adopted because derivatives crippled numerous key players on Wall Street five years ago, including Countrywide Mortgages, Bear Stearns, AIG, Lehman Brothers, Washington Mutual, Wachovia and others.

One of those “others” was Citigroup, which had to be bailed out by the federal government to the tune of $45 billion. A Citigroup lobbyist, though, was primarily responsible for authoring theSwaps Regulatory Improvement Act, which was approved by the U.S. House of Representativestwo weeks ago.

The bill would wipe out Section 716 (pdf) of Dodd-Frank that requires banks to use a non-bank entity for trading commodity, energy and other swaps. In other words, if the legislation becomes law, financial institutions could return to conducting high-risk trading with funds that are backed by the FDIC (i.e. the taxpayer).

Dennis Anderson, who’s running for Congress from Illinois, says “to propose an easing of the controls on such behavior is irresponsible.”

“The behavior of these large banks and financial institutions cost all of us in loss of value in our retirement accounts, in lowered property values and, most importantly, in the general and deep recession that followed the failure of their gambling,” Anderson wrote at Daily Kos. “The idea of ‘too big to fail’ is still with us, and has grown even more threatening as these institutions have continued to grow.”

Citigroup was responsible for recommendations made in 70 lines of the 85-line bill, according to Eric Lipton and Ben Protess of The New York Times. In fact, reported the writers, a couple key paragraphs in the bill had been copied word for word from Citigroup’s submitted draft, which it had developed in conjunction with other Wall Street banks.

The legislation cleared the House on a 292-122 vote that saw 70 Democrats join all but three Republicans. Republicans voting against the measure were Representatives John Duncan of Tennessee, Walter Jones of North Carolina and Thomas Massie of Kentucky.

One of the Democrats supporting the change was Representative Carolyn Maloney of New York, the second-ranking Democrat on the House Financial Services Committee. She told The Hill that the bill would “protect safety and soundness,” per Federal Reserve Chairman Ben Bernanke.

“Even Federal Reserve Chairman Ben Bernanke opposed Section 716 as written, stating that the way it forces these activities out of insured depository institutions ‘would weaken both the financial stability and strong regulation of the derivatives activities,’” she said.

Bernanke has supported certain changes to the law, but never backed the Citigroup bill, according to the Times.

The White House said it opposes the bill, noting that the law is still being implemented by regulators. Legislation to amend it is “premature and could be disruptive and harmful to the implementation of these reforms,” it added.

Only about 40% of the rules required by the law have been implemented to date. Whether the Citigroup bill passes or not, such attempted legislation has “a chilling effect on regulators,” according to the Times.

“After inflicting so much pain and suffering on the American people, now is not the time to let the largest banks back into the casino,” Representative Maxine Waters (D-California) said in a statement.

Why are so many other Democrats supporting a bill that the Obama administration opposes? House aides interviewed by the Timestheorized that “Republicans have enough votes to pass it themselves, so vulnerable House Democrats might as well join them, and collect industry money for their campaigns,” wrote Lipton and Protess.

Indeed, lawmakers who currently support bills advocated by big banks have, this month, received double the amount of donations from Wall Street firms as those who opposed such bills, according to MapLight, a nonprofit group that analyzes campaign financial records.

Additionally, Wall Street has, in the past few weeks, hosted special fundraisers for the bills’ co-sponsors.

A Democrat who supports the industry bills and is a top cash recipient of Wall Street—Representative Jim Himes of Connecticut, who was once a Goldman Sachs banker—confessed that the “system” has “problems.” “It’s appalling, it’s disgusting, it’s wasteful and it opens the possibility of conflicts of interest and corruption,” he told the Times. “It’s unfortunately the world we live in.”

-Noel Brinkerhoff, Danny Biederman

How JP Morgan Bribed The Chinese Prime Minister's Daughter Using A Fake Name

Submitted by Michael Krieger of Liberty Blitzkrieg blog,

Allegations of JP Morgan’s use of clever tactics to bribe Chinese officials recently received mainstream attention when Salon journalist Alex Pareene mentioned it in a comical and classic interview on CNBC (you need to watch the video before reading this) with presstitute Maria Bartiromo. When Mr.Pareene mentioned these claims against the TBTF bank, CNBC mocked him for the fact that his information had come from the New York Times. Well it appears the paper has now given CNBC a taste of its own medicine; with some actual real reporting, something the clownish financial-tv channel drowning in a zero ratings death spiral doesn’t seem all that interested in doing.

This article from the New York Times details how JP Morgan paid $75,000 a month to an obscure consulting firm called Fullmark Consultants, which had only two employees. The firm was run by a woman named Lily Chang, which in reality was the alias used by Wen Jiabao’s only daughter Wen Ruchun. Wen Jiabao was the Prime Minister of China at the time.

Unsurprisingly, many lucrative deals followed for the JP Morgan in China. How about we#AskJPM about that.

More from the NY Times:

To promote its standing in China, JPMorgan Chase turned to a seemingly obscure consulting firm run by a 32-year-old executive named Lily Chang.Ms. Chang’s firm, which received a $75,000-a-month contract from JPMorgan, appeared to have only two employees. And on the surface, Ms. Chang lacked the influence and public name recognition needed to unlock business for the bank.But what was known to JPMorgan executives in Hong Kong, and some executives at other major companies, was that “Lily Chang” was not her real name. It was an alias for Wen Ruchun, the only daughter of Wen Jiabao, who at the time was China’s prime minister, with oversight of the economy and its financial institutions.JPMorgan’s link to Ms. Wen — which came during a time when the bank also invested in companies tied to the Wen family — has not been previously reported. Yet a review by The New York Times of confidential documents, Chinese public records and interviews with people briefed on the contract shows that the relationship pointed to a broader strategy for accumulating influence in China: Put the relatives of the nation’s ruling elite on the payroll.Now, United States authorities are scrutinizing JPMorgan’s ties to Ms. Wen, whose alias was government approved, as part of a wider bribery investigation into whether the bank swapped contracts and jobs for business deals with state-owned Chinese companies, according to the documents and interviews. The bank, which is cooperating with the inquiries and conducting its own internal review, has not been accused of any wrongdoing.

Of course not, don’t be ridiculous!

For Ms. Wen’s consulting firm, Fullmark Consultants, the JPMorgan deal was lucrative. While many Hong Kong investment bankers were earning as much as $250,000 a year, JPMorgan paid Ms. Wen’s firm $900,000 annually from 2006 to 2008, records show, for a total of $1.8 million.A spokesman for JPMorgan declined to comment. In a previous regulatory filing, the bank disclosed that authorities were examining “its business relationships with certain related clients in the Asia Pacific region and its engagement of consultants.”The children of China’s ruling elite, according to experts, have occasionally used government-approved aliases to protect their privacy while studying or traveling abroad. Ms. Wen used her alias for both schooling and business. According to government records, Ms. Wen holds two national identity cards with matching birth dates, one issued in Beijing under the name Wen Ruchun and a second issued in the northeastern city of Dalian, as Chang Lily.JPMorgan’s contract with Fullmark called for the consultant to “to promote the activities and standing” of the bank in China. According to Fullmark’s letter to JPMorgan, the consulting firm had three main tasks. One, it helped JPMorgan secure the underwriting job on the China Railway deal. It also advised JPMorgan about forming a joint venture with a Chinese securities firm and provided counsel on the “macroeconomics policy in mainland China.”The letter, sent around the time of the financial crisis, struck an optimistic tone. “We hope JPMorgan Chase will grasp the opportunities and become to be the winner in the financial crisis,” it read.

Well we all know how that turned out…

Full article here.

Federal Reserve Whistleblower Tells America The REAL Reason For Quantitative Easing

Michael SnyderEconomic Collapse

November 13, 2013

November 13, 2013

A banker named Andrew Huszar that helped manage the Federal Reserve’s quantitative easing program during 2009 and 2010 is publicly apologizing for what he has done. He says that quantitative easing has accomplished next to nothing for the average person on the street. Instead, he says that it has been “the greatest backdoor Wall Street bailout of all time.” And of course the cold, hard economic numbers support what Huszar is saying.

Image: Wikimedia Commons

The percentage of working age Americans with a job has not improved at all during the quantitative easing era, and median household income has actually steadily declined during that time frame. Meanwhile, U.S. stock prices have doubled overall, and the stock prices of the big Wall Street banks have tripled. So who benefits from quantitative easing? It doesn’t take a genius to figure it out, and now Andrew Huszar is blowing the whistle on the whole thing.

From 2009 to 2010, Huszar was responsible for managing the Fed’s purchase of approximately $1.25 trillion worth of mortgage-backed securities. At the time, he thought that it was a dream job, but now he is apologizing to the rest of the country for what happened…

I can only say: I’m sorry, America. As a former Federal Reserve official, I was responsible for executing the centerpiece program of the Fed’s first plunge into the bond-buying experiment known as quantitative easing. The central bank continues to spin QE as a tool for helping Main Street. But I’ve come to recognize the program for what it really is: the greatest backdoor Wall Street bailout of all time.

When the first round of quantitative easing ended, Huszar says that it was incredibly obvious that QE had done very little to benefit average Americans but that it had been “an absolute coup for Wall Street”…

Trading for the first round of QE ended on March 31, 2010. The final results confirmed that, while there had been only trivial relief for Main Street, the U.S. central bank’s bond purchases had been an absolute coup for Wall Street. The banks hadn’t just benefited from the lower cost of making loans. They’d also enjoyed huge capital gains on the rising values of their securities holdings and fat commissions from brokering most of the Fed’s QE transactions. Wall Street had experienced its most profitable year ever in 2009, and 2010 was starting off in much the same way.You’d think the Fed would have finally stopped to question the wisdom of QE. Think again. Only a few months later—after a 14% drop in the U.S. stock market and renewed weakening in the banking sector—the Fed announced a new round of bond buying: QE2. Germany’s finance minister, Wolfgang Schäuble, immediately called the decision “clueless.”That was when I realized the Fed had lost any remaining ability to think independently from Wall Street.

Of course the fact that the Fed cannot think independently from Wall Street should not be a surprise to any of my regular readers. As I have written about repeatedly, the Federal Reserve was created by the Wall Street bankers for the benefit of the Wall Street bankers. When the Federal Reserve serves the interests of Wall Street, it is simply doing what it was designed to do. And according to Huszar, quantitative easing has been one giant “subsidy” for Wall Street banks…

Having racked up hundreds of billions of dollars in opaque Fed subsidies, U.S. banks have seen their collective stock price triple since March 2009. The biggest ones have only become more of a cartel: 0.2% of them now control more than 70% of the U.S. bank assets.

But Huszar is certainly not the only one on Wall Street that acknowledges these things. For example, just check out what billionaire hedge fund manager Stanley Druckenmiller told CNBC about quantitative easing…

“This is fantastic for every rich person,” he said Thursday, a day after the Fed’s stunning decision to delay tightening its monetary policy. “This is the biggest redistribution of wealth from the middle class and the poor to the rich ever.”“Who owns assets—the rich, the billionaires. You think Warren Buffett hates this stuff? You think I hate this stuff? I had a very good day yesterday.”Druckenmiller, whose net worth is estimated at more than $2 billion, said that the implication of the Fed’s policy is that the rich will spend their wealth and create jobs—essentially betting on “trickle-down economics.”“I mean, maybe this trickle-down monetary policy that gives money to billionaires and hopefully we go spend it is going to work,” he said. “But it hasn’t worked for five years.”

And Donald Trump said essentially the same thing when he made the following statement on CNBC about quantitative easing…

“People like me will benefit from this.”

The American people are still being told that quantitative easing is “economic stimulus” which will make the lives of average Americans better.

That is a flat out lie and the folks over at the Federal Reserve know this.

In fact, a very interesting study conducted for the Bank of England shows that quantitative easing actually increases the gap between the wealthy and the poor…

It said that the Bank of England’s policies of quantitative easing – similar to the Fed’s – had benefited mainly the wealthy.Specifically, it said that its QE program had boosted the value of stocks and bonds by 26 percent, or about $970 billion. It said that about 40 percent of those gains went to the richest 5 percent of British households.Many said the BOE’s easing added to social anger and unrest. Dhaval Joshi, of BCA Research wrote that “QE cash ends up overwhelmingly in profits, thereby exacerbating already extreme income inequality and the consequent social tensions that arise from it.”

And this is exactly what has happened in the United States as well.

U.S. stocks have risen 108% while Barack Obama has been in the White House.

And who owns stocks?

The wealthy do. In fact, 82 percent of all individually held stocks are owned by the wealthiest 5 percent of all Americans.

Meanwhile, things have continued to get even tougher for ordinary Americans.

While Obama has been in the White House, the percentage of working age Americans with a job has declined from 60.6% to 58.3%, median household income has declined for five years in a row, and poverty has been absolutely exploding.

But the fact that it has been very good for Wall Street while doing essentially nothing for ordinary Americans is not the biggest problem with quantitative easing.

The biggest problem with quantitative easing is that it is destroying worldwide faith in the U.S. dollar and in the U.S. financial system.

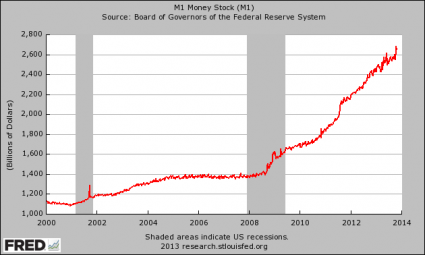

In recent years, the Federal Reserve has started to behave like the Weimar Republic. Just check out the chart below…

The rest of the world is watching the Fed go crazy, and they are beginning to openly wonder why they should continue to use the U.S. dollar as the de facto reserve currency of the planet.

Right now, most global trade involves the use of U.S. dollars. In fact, far more U.S. dollars are actually used outside of the United States than are used inside the country. This creates a tremendous demand for U.S. dollars around the planet, and it keeps the value of the U.S. dollar at a level that is far higher than it otherwise would be.

If the rest of the world decides to start moving away from the U.S. dollar (and this is already starting to happen), then the demand for the U.S. dollar will fall and we will not be able to import oil from the Middle East and cheap plastic trinkets from China so inexpensively anymore.

In addition, major exporting nations such as China and Saudi Arabia end up with giant piles of U.S. dollars due to their trading activities. Instead of just sitting on all of that cash, they tend to reinvest much of it back into U.S. Treasury securities. This increases demand for U.S. debt and drives down interest rates.

If the Federal Reserve continues to wildly create money out of thin air with no end in sight, the rest of the world may decide to stop lending us trillions of dollars at ultra-low interest rates.

When we get to that point, it is going to be absolutely disastrous for the U.S. economy and the U.S. financial system. If you doubt this, just read this article.

The only way that the game can continue is for the rest of the world to continue to be irrational and to continue to ignore the reckless behavior of the Federal Reserve.

We desperately need the rest of the planet “to ignore the man behind the curtain”. We desperately need them to keep using our dollars that are rapidly being devalued and to keep loaning us money at rates that are far below the real rate of inflation.

If the rest of the globe starts behaving rationally at some point, and they eventually will, then the game will be over.

Let us hope and pray that we still have a bit more time until that happens.

JP Morgan said on Friday it has agreed to pay $4.5bn (£2.8bn) to settle claims by investors who lost money on mortgage-backed securities before the collapse of the US housing market.

The bank reached the agreement with 21 institutional investors in 330 residential mortgage-backed securities (RMBS) trusts issued by JP Morgan and Bear Stearns, which it took over during the financial crisis, according to the bank and lawyers for the investors.

The deal still has to be accepted by seven trustees overseeing the securities holdings, the parties said.

The settlement does not include trusts issued by Washington Mutual, which JP Morgan also acquired.

The deal is separate from the preliminary $13bn settlement JP Morgan has reached with the US government that would resolve a raft of actions over mortgage-backed securities.

Read More...

JP Morgan to pay $4.5bn to settle claims by investors: The bank has reached agreement with 21 institutional investors in 330 residential mortgage-backed securities trusts

November 16, 2013

Source: The Guardian

JP Morgan said on Friday it has agreed to pay $4.5bn (£2.8bn) to settle claims by investors who lost money on mortgage-backed securities before the collapse of the US housing market.

The bank reached the agreement with 21 institutional investors in 330 residential mortgage-backed securities (RMBS) trusts issued by JP Morgan and Bear Stearns, which it took over during the financial crisis, according to the bank and lawyers for the investors.

The deal still has to be accepted by seven trustees overseeing the securities holdings, the parties said.

The settlement does not include trusts issued by Washington Mutual, which JP Morgan also acquired.

The deal is separate from the preliminary $13bn settlement JP Morgan has reached with the US government that would resolve a raft of actions over mortgage-backed securities.

Read More...

These guys make the mafia look like campfire girls makin smores singin wohelo.

ReplyDeletehttp://www.zerohedge.com/news/2013-11-15/unspoken-toxic-secret-heart-shadow-banking-self-securitization-central-banks#comments

It's so far beyond diabolical..

NW

Morning NW - the term " Above The Law " comes to mind , right ?

ReplyDelete