http://www.zerohedge.com/news/2013-09-22/marc-faber-feds-neo-keynesian-clowns-are-holding-world-hostage

Submitted by Tyler Durden on 09/22/2013 18:16 -0400

Submitted by Tyler Durden on 09/22/2013 18:16 -0400

http://www.zerohedge.com/news/2013-09-23/qe-worked-weimar-republic-little-while-too

( Bernanke learned from Greenspan - get out of the job before everything falls down around your ears - then let the next guy / gal take the blame ! )

Submitted by Tyler Durden on 09/23/2013 20:09 -0400

http://www.zerohedge.com/news/2013-09-22/what-shadow-banking-can-tell-us-about-feds-exit-path-dead-end

http://www.zerohedge.com/news/2013-09-23/fed-soaks-118-billion-liquidity-first-fixed-rate-reverse-repo-test

Submitted by Tyler Durden on 09/23/2013 14:02 -0400

Submitted by Tyler Durden on 09/23/2013 14:57 -0400

Submitted by Tyler Durden on 09/23/2013 13:23 -0400

Marc Faber: "Fed's Neo-Keynesian Clowns... Are Holding The World Hostage"

- Bond

- Central Banks

- China

- Federal Reserve

- Global Economy

- Housing Market

- keynesianism

- Marc Faber

- Market Conditions

- Monetary Policy

- NASDAQ

- Neo-Keynesian

- Real estate

"There is nothing safe anymore, because the money-printing distorts all asset prices," is the uncomfortable response Marc Faber gives to Thai TV during this interview when asked for investment ideas. Faber explains how we got here "massive money-printing and ZIRP creates a huge pool of liquidity that does not flow evenly," as it washes from Nasdaq stocks to real estate to emerging markets and so on. Each time, "the bubble inflates and then is deflated as the capital (liquidity) floods out." The Fed, based on the doubling of interest rates since they began QE3 "has lost control of the bond market," Faber warns; adding that while he expects some "cosmetic tapering," the Fed members and other neo-Keynesian clowns will react to a "weakening US and global economy," and we will be a $150 billion QE by the end of next year, as the world is held hostage to US monetary policy.

The interview is interspersed with Thai translation but is well worth the time (starting at 1:25):

How did we get here (1:25):

"What we've had in the world is acrisis in 2008 that was caused by excessive leverage and excessive debt brought about by excessively low interest rates.For the last 4 years the Fed Funds rate has been essentially at zero and we have massive money printing - monetary inflation. This creates a huge pool of liquidity.The problem is that this liquidity will not flow evenly. It can flow first into NASDAQ stocks until March 2000, then in the US housing market, then in commodities, and gold, and then in emerging marketsYou have one bubble after the other. The bubble goes up and then is deflated when the capital (liquidity) moves out. That is the problem of money-printing by central banks."

On China (3:25)

"For the global economy, what happens in China is more important than what happens in the US."

On the Fed's Failure (3:43)

"QE3 and QE4 - the Fed's bond purchase program - began in September 2012. The goal of the Fed was to lower long-term interest rates... but they have gone up! The Fed has already lost control over long-term interest rates."

So we should do moar!!! (06:10)

Rates have doubled since QE3 began. It is annoying the way the Fed thinks. Some Fed members believe the Fed didn't buy enough. (they buy $85 a month - almost the entire issuance of the US government).

On The Taper (07:10)

They will probably announce some cosmetic tapering - not much...

The Fed has no clue (07:25)

They have no clue, the Fed academics are clueless (they have never worked in a real business)... but what they will do is: they will cut asset purchases by $10-20 billion but they will say "depending on economic and market conditions, we will reassess"... in a year's time they will buy $150 billion...

On The US Economy (08:10)

"The economy in the US is weakening.. and the global economy is weakening"

On Neo-Keynesian clowns (10:00)

"I know some of these clowns at the Federal Reserve, they think the Fed didn't do enough. The other clowns - the so-called Neo-Keynesians (which he describes a turbo-charged Keynesianism) think the deficits should not be $1 trillion but $5 trillion"

On the world held hostage (11:40)

If you are a relatively small country within the global economy. you are held hostage to US monetary policy.If the Fed has zero interest rates, it means depositors get practically zero interest rates. If the Thai central bank (or any other) would increase interest rates (conscious of speculation in real estate and stocks for instance) to cool down the speculation... but if they do that, the foreigners will pile in to the Thai Baht because they get maybe 4%; the Baht soars in value... which is not a bad thing in and of itself - but the Thai businessmen will cry "we cannot export"

On what investments are safe (14:45)

Gold, government bonds in the short-term (though long-term no because the US government is bankrupt, but they can postpone the problem for now)"There is nothing safe anymore, because the money-printing distorts all asset prices,"

On Inflation (15:30),

"I don't look at government statistics because all governments around the world lie."

http://www.zerohedge.com/news/2013-09-23/qe-worked-weimar-republic-little-while-too

( Bernanke learned from Greenspan - get out of the job before everything falls down around your ears - then let the next guy / gal take the blame ! )

QE Worked For The Weimar Republic For A Little While Too

Submitted by Michael Snyder of The Economic Collapse blog,

There is a reason why every fiat currency in the history of the world has eventually failed.

At some point, those issuing fiat currencies always find themselves giving in to the temptation to wildly print more money. Sometimes, the motivation for doing this is good. When an economy is really struggling, those that have been entrusted with the management of that economy can easily fall for the lie that things would be better if people just had "more money". Today, the Federal Reserve finds itself faced with a scenario that is very similar to what the Weimar Republic was facing nearly 100 years ago.

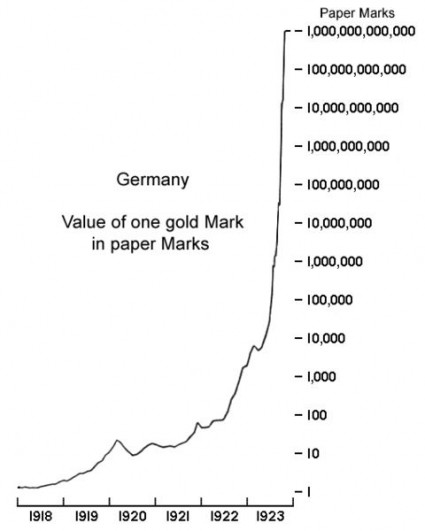

Like the Weimar Republic, the U.S. economy is also struggling and like the Weimar Republic, the U.S. government is absolutely drowning in debt. Unfortunately, the Federal Reserve has decided to adopt the same solution that the Weimar Republic chose. The Federal Reserve is recklessly printing money out of thin air, and in the short-term some positive things have come out of it. But quantitative easing worked for the Weimar Republic for a little while too.

At first, more money caused economic activity to increase and unemployment was low. But all of that money printing destroyed faith in German currency and in the German financial system and ultimately Germany experienced an economic meltdown that the world is still talking about today. This is the path that the Federal Reserve is taking America down, but most Americans have absolutely no idea what is happening.

It is really easy to start printing money, but it is incredibly hard to stop. Like any addict, the Fed is promising that they can quit at any time, but this month they refused to even start tapering their money printing a little bit. The behavior of the Fed is so shameful that even CNBC is comparing it to a drug addict at this point...

The danger with addictions is they tend to become increasingly compulsive. That might be one moral of this week's events.A few days ago, expectations were sky-high that the Federal Reserve was about to reduce its current $85 billion monthly bond purchases. But then the Fed blinked, partly because it is worried that markets have already over-reacted to the mere thought of a policy shift.Faced with a choice of curbing the addiction or providing more hits of the QE drug, in other words, it chose the latter.

So why won't the Fed cut back on the reckless money printing?

Well, as Peter Schiff recently noted, Fed officials seem to be convinced that any "tapering" could result in the bursting of the massive financial bubbles that they have created...

The Fed understands, as the market seems not to, that the current "recovery" could not survive without continuation of massive monetary stimulus. Mainstream economists have mistaken the symptoms of the Fed's monetary expansion, most notably rising stock and real estate prices, as signs of real and sustainable growth. But the current asset price bubbles have nothing to do with the real economy. To the contrary, they are setting up for a painful correction that will likely be worse than the one we experienced five years ago.

As I have written about previously, the Federal Reserve is usually very careful not to do anything which will hurt the short-term interests of the financial markets and the big banks.

But at this point the Fed is caught in a trap. If it continues to pump, the financial bubbles that it has created will get even worse. If it stops, those bubbles will burst. But as Doug Kassnoted recently, it is inevitable that these financial bubbles will burst at some point one way or another...

"Getting in was easy. Getting out—not so much. The Fed is trapped and can't end tapering or else the bond and stock markets will blow up. The longer this continues the bigger the inevitable burst."

In essence, we can have disaster now or disaster later.

But most Americans don't care much about what is happening on Wall Street. They just want economic conditions to get better for them and for those around them. And to this day, the mainstream media continues to sell quantitative easing to the American people as an "economic stimulus" program by the Federal Reserve.

So has quantitative easing actually been good for the U.S. economy?

Not really.

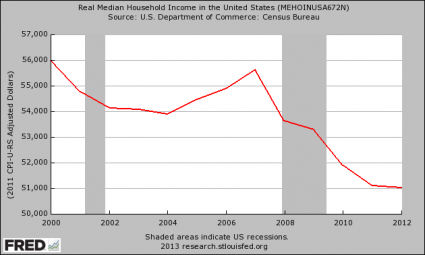

For example, while the Fed has been recklessly printing money out of thin air, household incomes have actually been going down for five years in a row...

What about employment?

Don't more Americans have jobs now?

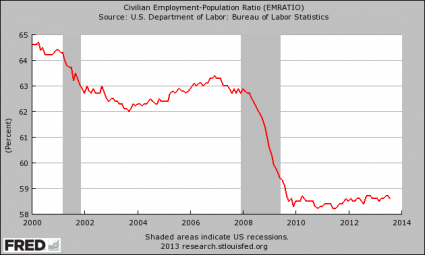

Actually, that is not the case at all. Posted below is a chart that shows how the percentage of working age Americans with a job has changed since the year 2000. As you can see, the employment to population ratio fell from about 63 percent before the last recession down to underneath 59 percent at the end of 2009 and it has stayed there ever since...

So where is the "employment recovery"?

Can you point it out to me? Because I have been staring at this chart for a long time and I still can't find it.

So if quantitative easing has not been good for average Americans, who has it been good for?

The wealthy, of course.

Just check out what billionaire hedge fund manager Stanley Druckenmiller told CNBCabout quantitative easing the other day...

"This is fantastic for every rich person," he said Thursday, a day after the Fed's stunning decision to delay tightening its monetary policy. "This is the biggest redistribution of wealth from the middle class and the poor to the rich ever.""Who owns assets—the rich, the billionaires. You think Warren Buffett hates this stuff? You think I hate this stuff? I had a very good day yesterday."Druckenmiller, whose net worth is estimated at more than $2 billion, said that the implication of the Fed's policy is that the rich will spend their wealth and create jobs—essentially betting on "trickle-down economics.""I mean, maybe this trickle-down monetary policy that gives money to billionaires and hopefully we go spend it is going to work," he said. "But it hasn't worked for five years."

Sadly, Druckenmiller is exactly correct.

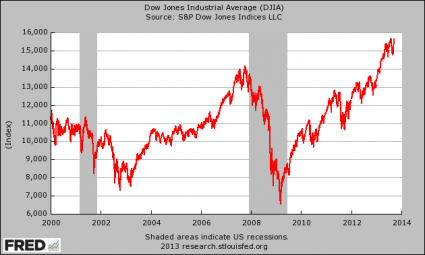

Since the end of the last recession, the Dow has been on an unprecedented tear...

Of course these stock prices have nothing to do with economic reality at this point, but for the moment those that are making giant piles of cash on Wall Street don't really care.

Sadly, what very few people seem to understand is that what the Fed is doing is going to absolutely destroy confidence in our currency and in our financial system in the long-term. Yeah, many investors have been raking in huge gobs of cash right now, but in the long run this is going to be bad for everybody.

We have now entered a money printing spiral from which there is no easy exit. According to Graham Summers, the Fed has "crossed the Rubicon" and we are now "in the End Game"...

If tapering even $10-15 billion per month from $85 billion month QE programs would damage the economy, then we’re all up you know what creek without a paddle.Put it this way… here we are, five years after 2008, and the Fed is stating point blank that the economy would absolutely collapse if it spent any less than $85 billion per month. This admission has proven just how long ago we crossed the Rubicon. We’re already in the End Game. Period.

Most Americans don't really understand what quantitative easing is, and most don't really try to understand it because "quantitative easing" sounds very complicated.

But it really isn't that complicated.

The Federal Reserve is creating gigantic mountains of money out of thin air every month, and the Fed is using all of that newly created money to buy government debt and mortgage-backed securities. Over the past several years, the value of the financial securities that the Fed has accumulated is greater than the total amount of publicly held debt that the U.S. government accumulated from the presidency of George Washington though the end of the presidency of Bill Clinton...

The same day that the Federal Reserve's Federal Open Market Committee announced last week that the Fed would continue to buy $40 billion in mortgage-backed securities (MBS) and $45 billion in U.S. Treasury securities per month, the Fed also released its latest weekly accounting sheet indicating that it had already accumulated more Treasuries and MBS than the total value of the publicly held U.S. government debt amassed by all U.S. presidents from George Washington though Bill Clinton.

To say that this is a desperate move by the Fed would be a massive understatement. We have never seen anything like this before in U.S. history.

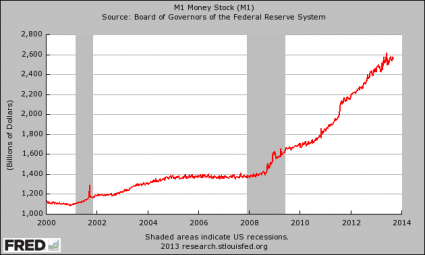

And look at what all of this wild money printing has done to our money supply...

In many ways, the chart above is reminiscent of what the Weimar Republic did during the early years of their hyperinflationary spiral...

Just like the Weimar Republic, our money supply is beginning to grow at an exponential pace.

So far, complete and total disaster has not struck, so most people think that everything must be okay.

But it is not.

In a previous article, I included an outstanding illustration from Simon Black that I think would be extremely helpful here as well…

Let’s say you’re at a party in a small apartment that’s about 500 square feet in size. Then suddenly, at 11pm, a pipe bursts, starting a trickle into the living room.Aside from the petty annoyance, would you feel like you were in danger? Probably not. This is a linear problem– the rate at which the water is leaking is more or less constant, so the guests can keep partying through the night without worry.But let’s assume that it’s an exponential leak.At first, there’s just one drop of water. But each minute, the rate doubles. So by 11:01pm, there’s 2 drops. By 11:02, 4 drops. And so forth.By 11:27pm, there’s only six inches of standing water. Yet by 11:31pm, just four minutes later, the entire room is under nearly 8 feet of water. And the party’s over.For nearly half an hour, it all seemed safe and manageable.People had all the time in the world to leave, right up until the bitter end. 11:27, 11:28, 11:29. Then it all went from benign to deadly in a matter of minutes.

Are you starting to get the picture?

What the Federal Reserve is doing is systematically destroying the U.S. dollar, and the rest of the world is starting to take notice.

Why should they continue to lend us trillions of dollars at super low interest rates when we are exploding the size of our money supply?

It is simply not rational for other nations to continue to lend us money at less than 3 percent a year when the real rate of inflation is somewhere around 8 to 10 percent and reckless money printing by the Fed threatens to greatly accelerate the devaluation of our currency.

When QE first started, the added demand for U.S. government debt by the Federal Reserve helped drive long-term interest rates down to record low levels.

But in the long-term, the only rational response by all other buyers of U.S. government debt will be to demand a much higher rate of return because of the rapid devaluation of U.S. currency.

So QE drives down long-term interest rates in the short-term, but in the long-term the only rational direction for long-term interest rates to go is much, much higher and in recent months we have already started to see this.

The only way that the Fed can stop this is by increasing the amount of quantitative easing.

Right now, the Fed is buying roughly half a trillion dollars worth of U.S. Treasuries a year, but the U.S. government issues close to a trillion dollars of new debt and must roll over about 3 trillion dollars of existing debt each year.

If the Federal Reserve eventually decides to buyall of the debt, then interest rates won't be a major problem. But if the Fed goes that far our financial system would be regarded as a total joke by the remainder of the globe and we would reach hyperinflation much more rapidly.

If the Federal Reserve stops buying debt completely, the financial bubbles that they have created will burst and we will rapidly be facing a financial crisis even worse than what we experienced back in 2008.

But almost whatever the Fed does at this point, the rest of the world will probably continue to start to move away from the U.S. dollar as the de facto reserve currency of the planet. This move is just beginning, but it is going to havemajor implications for us in the years ahead. This is a topic that I will be addressing extensively in future articles.

Most of the debate about quantitative easing has focused on the impact that it will have on the U.S. economy in the short-term.

That is a huge mistake.

Of much greatest importance is what quantitative easing means for the long-term.

The rest of the world is losing confidence in the U.S. dollar and in U.S. debt because of the reckless money printing that the Fed has been doing.

But we desperately need the rest of the world to use "the petrodollar" and to lend us the money that we need to pay our bills.

As the rest of the planet starts to reject the U.S. dollar and starts to demand a much higher rate of return to lend us money, the U.S. economy is going to experience a tremendous amount of pain.

It is hard to put into words how foolish the Federal Reserve has been. The Fed is systematically destroying what was once the strongest financial system in the world, and in the end we are all going to pay the price.

http://www.zerohedge.com/news/2013-09-22/what-shadow-banking-can-tell-us-about-feds-exit-path-dead-end

What Shadow Banking Can Tell Us About The Fed's "Exit-Path" Dead End

Submitted by Tyler Durden on 09/22/2013 20:08 -0400

- Asset-Backed Securities

- Ben Bernanke

- Capital Markets

- Central Banks

- ETC

- Excess Reserves

- Federal Reserve

- Federal Reserve Bank

- Housing Bubble

- Hyperinflation

- Lehman

- M2

- Monetary Base

- Monetary Policy

- None

- Prop Trading

- recovery

- Reflexivity

- Reserve Currency

- Reverse Repo

- Shadow Banking

- System Open Market Account

- Treasury Borrowing Advisory Committee

Over four years ago, in "Chasing the Shadow of Money", Zero Hedge first presented a curious if perverse aspect of the Fed's QE experiment in the context of the modern monetary system: the extraction of "quality" collateral by the Fed's daily purchases of Treasury (and MBS) securities, and it replacement with reserves - a transformation which while boosting asset prices, results in an ongoing deleveraging of shadow liabilities, as well as a persistent slowdown in the velocity of collateral (due to both its increasing degradation and increasing counterparty risk). Our concurrent investigation into the properties of shadow banking led us to the correction conclusion back in March 2012, and explanation why, the Fed would have to do at least another $3.6 trillion in QE. We are now $1 trillion in, and rapidly rising even as the 10 Year equivalents held by the Fed now represents almost one third of the entire Treasury market: an unprecedented collapse in available private-sector collateral.

And while there has been a small if vocal subset of voices warning about the problems of collateral scarcity, and the implications for the global financial balance sheet if and when renormalization is attempted, for the most part, this remains a very much misunderstood process. Perhaps the main reason for this is that, as Peter Stella summarizes, "When it comes to reducing excess reserves, the ‘how’ matters as much as the ‘when’ and ‘how much’.Understanding this point requires mastery of the brave new world of shadow banks and re-hypothecation – a world that either did not exist or was truly in the shadows when most of us were taught about money and credit creation."

Over the past 5 years we have attempted to provide a glimpse into how modern shadow banking (with a world in which rehypothecation is the "source" of tens of trillions in deposit-free credit money), however, the vast majority of modern economists and those espousing modern "magic money tree" theories, still view the world through the lens of a 1980s textbook, which is absolutely insufficient when attempting to explain marginal credit creation amounting to tens of trillions in the shadow banking system. Ironically, it was precisely the collapse in collateral chains and the freeze in shadow counterparty derivative exposure just before the failure of Lehman, captured with stunning precisions by Matt King's "Are the Brokers Broken?" report issued a week before the Lehman bankruptcy, that explained more about the perilous nature of modern finance, than any other paper written before or after (p.s. Yes, the brokers were, and still are, broken).

Not surprisingly, the topic of "high quality collateral" and specifically, its disappearance, has been the topic of not one but both of the last Treasury Borrowing Advisory Committee refunding presentations (here and here). And since Tapering was fundamentally, all about slowing down the rate of high quality collateral extraction, one can expect the next TBAC refunding presentation be a veritable screamfest of warnings from the likes of Citi's Matt King and CS' James Sweeney (sadly it seems they will fall on increasing more deaf ears). That said, if and when the Fed is compelled by the JPM/Goldman-chaired TBAC to finally slow down and/or halt the pace of collateral extraction, the question is what will happen then, especially as pertains to the all important shadow banking system.

About a month ago, the IMF's Manmohan Singh wrote a White Paper titled simply enough "Collateral and Monetary Policy" where in 17 pages, which dealt precisely with this issue, which among other things did a great job of explaining the logic behind the Fed's proposal to commence a reverse repo program which would be expanded to include non-bank participants, in effect expanding the eligibility of the Fed's "reserves as collateral" away from pure-play bank institutions. However, more than anything, Singh was lamenting the ongoing collapse in the velocity of collateral, as follows: "The economy needs the collateral services that these securities can offer,which transfers with possession, not ownership. Securities in the market domain have a velocity; those at the central bank do not. So, D (excess reserves) does not substitute for C1 (good collateral) and thus there is a net reduction in overall financial lubrication."

That also suggests that a perfectly centrally-planned market should be oblivious of counterparty (ownership less important than possession) risk, in order to preserve financial "lubrication" - a commandment which so far markets have failed to comply with. In fact the more Bernanke absorbs quality collateral, the lower the velocity of existing collateral. This is also one of the main difficulties facing the Fed. Recall slide 30 of the TBAC's Q1 presentation appendix on liquid private collateral:

Here again is the punchline:

- "the more restricted the private sector's ability to create safe, liquid, and moneylike collateral, the harder the public sector must work to supply it through deficits and easy monetary policy"

In other words, until such time as the housing bubble has been reflated enough and yield-chasing through RMBS and CMBS securitization is once again a staple of the daily "financial innovation" (which makes housing a Treasury-equivalent HQC), there is little the Fed can do to truly pull away, and the Treasury will be forced to come up with any and every excuse to "supply collateral through deficits." Hence the need for acute regional conflicts such as Syriaet al.

But going back to the original topic, namely what are the (increasingly more limited) options for the Fed as it seeks to unwind QE from a shadow banking perspective, we go to the abovementioned Peter Stella, who over the weekend wrote an excellent article in VoxEU titled "Exit-path implications for collateral chains" dealing with just this. His summary:

QE is still on, but central banks are pondering exit pathways. Exit requires vacuuming up excess reserves, winding down massive securities holdings, and restoring normal interest rates – all without killing the recovery. This column points to the importance of a seemingly technical issue – the impact of the exit on the supply of high-quality collateral. This matters since collateral plays a critical role in today’s credit and money creation processes. When reducing excess reserves, the ‘how’ matters as much as the ‘when’ and ‘how much’.

First, here is what according to Stella "needs exiting"

The Federal Reserve balance sheet is much simpler than at the height of the crisis.

- If Rip Van Winkle awoke today after a five-year nap, he would see only one key development in the Fed’s balance sheet – securities holdings higher by $2.9 trillion and deposits of depository institutions (banks) higher by $ 2.2 trillion.2

If he asked how this happened, Rip would be given a very simple answer.

- The Fed bought securities to lower interest rates; it paid for them by creating bank reserves.

That is, the Fed credited the securities seller’s commercial bank with a deposit at one of the 12 Federal Reserve Banks, and the commercial bank then credited the seller’s account. On net, privately held securities were exchanged for Fed deposits.If pressed further as to why banks are holding enormous reserves at the Fed, Rip would get an equally simple answer: Banks have no choice.

- It is – for all intents and purposes – technically and legally impossible for a bank to transfer deposits at a Federal Reserve Bank to a nonbank.

Reserves in the US are defined to comprise bank deposits held at one of the 12 Federal Reserve Banks (plus qualifying vault cash).

- Fed deposits may be transferred only to entities entitled to hold Fed accounts.

This is a key point when thinking about the various exit paths ahead. Fed deposits are not fungible outside the banking system, but Treasuries are.

Bullet point three is not exactly correct, but we'll get into the nuances shortly. For the most part, this is an accurate and comprehensive summary of the bind the Fed-cum-Commercial Banking monetary creation mechanism has found itself in.

Stella goes on to explain the impact of the "portfolio effect" on collateral:

Large Scale Asset Purchases (LSAPs) have inadvertently caused a significant change in the composition of assets available in the open market.

- The stock of marketable, highly liquid, AA+ collateral fell by trillions (disappearing into the Fed’s portfolio, i.e. System Open Market Account).

- The stock of assets available only for interbank trade (bank reserve deposits at the Fed) rose by trillions.

The essence of this change has nothing to do with credit risk. Treasuries and Fed deposits are equally safe. But they differ significantly in their marketability.Anyone can trade Treasury securities; only banks can exchange Fed deposits. The massive importance nonbanks play in today’s markets means that this portfolio effect can be important. To understand why marketability beyond banks matters, it is necessary to understand the modern money and credit creation process.

The bolded above is also the reason why the Fed is currently considering ways to expand its reverse repo pathways (when the time comes to unwind liquidity) to non-bank actors as we explained before.

Stella then proceeds into a useful historical lesson, explaining why those who don't or can't grasp the nuances of shadow banking and modern money creation, are completely clueless as they approach the Fed's action from the perspective of finance as it existed in the 1980s.

One cannot think straight about the future impact of different exit strategies without understanding of the role of bank reserves in today’s financial markets.

- Banking and money creation has not worked for at least two decades in the way that most people learned in school.

The old system was rather simple in the textbooks. The basic assumptions were (i) all credit was provided by banks; (ii) all bank credit (assets) were funded by the issuance, or creation, of depository liabilities (money) subject to a reserve requirement; and (iii) central banks controlled credit/money/inflation by rationing bank reserves. A stable 'money multiplier' was hypothesised to allow central banks to accurately predict the eventual impact of changes in bank reserves on money and credit.The problem with the old theory of monetary operations is that none of the three assumptions has been true for at least a generation.Most credit in the US is created by nonbanks; virtually all bank lending is funded by the creation of liabilities that are not subject to reserve requirements, and central banks do not ration reserves. In fact they take great pains to provide banks with the amount of reserves they desire. Central banks influence credit not by rationing the quantity of reserves but by altering the interest rate that banks must pay to obtain the quantity of reserves they desire.

- Today, credit creation in general and money creation in particular are no longer tied to the stock of reserves (i.e. the stock of banks’ deposits at the Fed).

Today, bank deposits at the Fed have only one real role – to facilitate management of the payments system. They are used to settle transactions among banks. Thus:

- The old notion that the quantity of bank reserves constrains lending in a fiat money world is completely erroneous.

- Traditional monetary policy has virtually nothing to do with money.

This is clearly seen in the long-term evolution of reserves and credit.

- In 1951, total commercial bank deposits at the Fed were $20 billion larger than they were at the end of 2006.

- Over the same period, total US credit-market assets rose by over 10,000%.5

Plainly the stock of reserves is no longer connected to credit or meaningful measures of “money” via the old-notion of a reserve-ratio-based money multiplier.

Here, Stella gets into a tangent that while accurate is not comprehensive. He believes that "One of the unintended consequences of Fed LSAPs has been the withdrawal of high quality liquid collateral such as US Treasuries from the financial markets paid for by crediting commercial bank reserve accounts. As discussed above, the banking system as a whole cannot dispose of these assets (reserves). At the same time, banks are under massive pressure world-wide to deleverage. This can take place either by increasing capital (a bank liability), which is costly to shareholders, or by reducing assets. Thus banks’ massive holdings of reserves at the Fed are ‘deadwood’ as far as the banks and their credit-creation capacity are concerned. They may crowd out credit. The deadwood problem will get worse if the US tightens regulatory leverage ratios – that is, reduces the maximum ratio permitted between a bank’s total assets and capital." This is correct, but there is more as we will shortly show.

Which brings us to what we believe is Stella's punchline:

There is a great irony in the journalistic history of monetary policy. What many are calling central bank “money creation” “helicopter money” or “rolling the printing presses” may – in combination with tighter leverage ratios – lead to a tightening of bank credit and deflationary pressures. And all this is occurring while the spectre of uncontrolled credit expansion and monetary debasement are being decried countless times by those who have not recognized that yesteryear’s monetary paradigm is defunct.

Well, no. While indeed forced deleveraging and crowding out of "assets" with reserves may result in lower asset prices (if Basel III were to actually be implemented that is, instead of constantly postponed to some point in the indefinite future), the bigger question is how the Fed would respond to such a deflationary phenomenon. The answer: is simple - more of the same, resulting in such a deluge of nominal dollars in the monetary base that inevitably the reserve status of the US currency becomes questioned (especially if preceded by such Fed-confidence shaking events as the Non-taper debacle of last week). So while there may well be a nominal deflation problem in the future, the offset will be one and the same not only in the US but all developed world central banks (as the BOJ has recently shown can imitate the Fed so well when necessary). From there, the distance to a wholesale refutation of a broken fiat-monetarist-Keynesian paradigm is progressively shorter. And keep in mind, hyperinflation is not lots of inflation: it is an outright loss of faith in a currency (and/or loss of reserve currency status), for political or monetary reasons.

At this point Stella touches on a topic we have discussed before, namely the tactical, operational aspects of reserve drainage: whether they should proceed by reverse repo or term deposits. Needless to say, Stella is, correctly, a fan of the repo extraction route, and is why the Fed is also recently contemplating just this. In an ideal world, where the Fed actually gets to a point where it can implement not only a tapering without destroying Emerging Markets, but actually commence to withdraw liquidity from the market without the most epic market tantrum ever, this is the so called "exit pathways."

Term deposits and reverse repos might appear very similar reserve draining tools to the proverbial Rip Van Winkle who slept through the radical changes in credit creation, collateral chains, and expansion of the shadow banking system.

- To Rip Van Winkle, term deposits and reverse repos are both simple transformations of overnight deposits into 7, 14 or 28 day “term” deposits, or to 7-, 14-, or 28-day reverse repos.

Well informed observers, however, will immediately see the critical difference (a good start on getting informed is to read Singh and Stella 2012).

- A reverse-repo has a portfolio effect that term deposits do not.

The reverse-repo takes cash out of the market and replaces it with high-quality collateral. Thus a key difference is the enlargement of the market supply of good collateral that banks and nonbanks would posses and thereby be able to use to fund their asset positions and create credit via ‘collateral chains’. (Technically this re-lending of collateral is called re-hypothecation.) Thus reverse repos add to financial lubrication in a way term deposits do not.This 'sweetener' would soften the bitter medicine of rising interest rates and alleviate the so-called ‘high quality collateral shortage’ pointed out by Treasury Borrowing Advisory Committee members (US Treasury 2013).

The magnitude of the task would be substantial: somewhere in the neighborhood $3 trillion (or more) in reserve reduction.

What is the rough magnitude of the task if the Fed balance sheet were to remain at its current size?

- In the two weeks ending 27 August 2008, average daily reserves held by depository institutions (banks) were $46.1 billion; required reserves were $ 44.1 billion.12 Of this, vault-cash used to satisfy required reserves was $36.4 billion and reserve balances held at FRB were $9.7 billion.

- In the two weeks ending 21 August 2013, average daily reserves held by banks were $2.2 trillion – that’s trillion with a ‘t’; required reserves were $115 billion – that’s billion with a ‘b’. Of this, vault cash used to satisfy required reserves was $53.4 billion and reserve balances held at FRB were $2.1 trillion.

- Thus bank excess reserves rose by $2.123 trillion during the last five years.

Of course, the Lehman bankruptcy convinced banks that they want more excess reserves than before, so the Fed will not need to drain the full $2.123 trillion. Let us say the task is to eliminate about $2 trillion in excess reserves. But of course the world does not stand still. The number could be closer to $3 trillion by the time LSAPs end.What this means is that the change in the availability of good collateral could be quite significant.

So to summarize Stella's take on the Fed's exit pathways, when contemplating such an event on broader structural collateral limitations:

Many major central banks are thinking strategically about exit pathways – how best to return to normal central banking. The main point of this column is to point to a key issue – the role of collateral – that has been under appreciated by many economists who are not in daily contact with financial markets.When economies strengthen and central banks begin to drain reserves from the system, they will inevitably alter the composition of private sector asset portfolios.

- If good collateral is swapped for reserves, banks and nonbanks can use the collateral to fund create credition via what are known as collateral chains.

- If only term deposits are swapped for reserves, or if interest rates are raised only through IOR, the opportunity to lengthen collateral chains will be missed.

In today’s financial world, these chains are critical sources of money and credit creation – the days of textbook money-multipliers are long gone.When it comes to reducing excess reserves, the ‘how’ matters as much as the ‘when’ and ‘how much’. Understanding this point requires mastery of the brave new world of shadow banks and re-hypothecation – a world that either did not exist or was truly in the shadows when most of us were taught about money and credit creation.

All of the above deserves a careful re-reading in its original VoxEU format (found here).

* * *

And now for a quick, and important, tangent. Stella's key contention is that Fed reserves parked with commercial banks are inert: that is, the securities (assets) they replace on bank balance sheets, could have participated in collateral chains and generally increasing the velocity of collateral, which by the way as Singhshowed a month ago, has dropped to the lowest, 2.2, since 2007 and probably long prior:

This is correct, and through second-order effects (i.e., reflexivity) is forcing the continued deleveraging in shadow banking credit-money (ABS, repos, GSEs, etc), as we show every quarter following the release of the Fed's Flow of Funds statement.

However, there is a very key trade-off to the banks, and perhaps this goes to the heart of the argument of just how the Fed engages in goosing risk assets, a topic which many still are confused by.

To make it all crystal clear, we present Exhibit A: a chart showing total loans and deposits at US commercial banks (local and foreign) just after the failure of Lehman, compared to their balance sheet as of the most recent week (as reported by the Fed's H.8 statement).

What it shows is the following:

This is perhaps the one chart that explains not only all that is wrong with US banks currently, but also why the US stock market is where it is.

It shows, among other things, that while over the past five years, total loans and leases in US commercial banks have not increased by one dollar, total deposits have risen by $2.2 trillion to $9.5 trillion. Why is this important? This is what Singh had to say about deposits:

When central banks buy securities,one of the immediate effects is to increase bank deposits, which adds to M2 (in the U.S., practically the Fed has bought from nonbanks, not banks). Whether banks maintain those added deposits as deposits, or convert them into other liabilities (or, by calling in loans, reducing or moderating the growth of their balance sheets), is an open question.

Sure enough, as the chart above shows, the total loan hole resulting from the increase in deposits was plugged by none other than the Fed, which over the past 5 years has injected $2.2 trillion in securities into commercial banks, leading to the observed increase in total deposits to nearly $10 trillion.

Furthermore, we, or rather, JPMorgan is happy to respond to Singh's "open question", courtesy of none other than the London Whale fiasco, which "closed" said question quickly and effectively.

Presenting Exhibit B, which comes directly from page 24 of JP Morgan's June 13, 2012 Financial Results appendix, in which the firm laid out, for all to see, just how it is that the Firm generated over $5 billion in prop trading losses in its Chief Investment Office unit - a department which had previously been tasked with "hedging" trades but as it turned out, was nothing but a glorified, and blessed from the very top, internal hedge fund, one with $323 billion in Assets Under Management! To wit:

The chart above shows the snapshot - from the horse's mouth - of how a major "legacy" bank, one engaged in both deposits and lending, decided to use the "deposit to loan gap" which had swelled to $423 billion at just JPM (blue box in middle), and led to $323 billion in CIO "Available For Sale securities."

What happened next is well-known to all: JPM's Bruno Iksil, together with Ina Drew and the rest of the CIO group, decided to put on a massive bet amounting to hundreds of billions in notional across the credit spectrum (the one place where a position of this size could be established without becoming the entire market, although by the time it imploded Bruno Iksil was the market in IG9 and various other indices and tranches). The loss was just as staggering, and amounts to what is one of the largest prop bets gone horribly wrong in history.

The aftermath for JPM is well-known, and as was disclosed last week, the "tempest in a teapot" would cost JPM $950 million to settle everything.

However, what is more important for those concerned by goings on in the Shadow banking system, JPM revealed just how those supposedly "inert" reserves end up being transformed on a bank's balance sheet into an ROI, without them ever leaving the bank.

As the London Whale showed without a shadow of a doubt, the key steps are as follows:

- Excess reserves (assets) are represented as cash deposits (liability)

- The excess cash is then used as collateral for margined securities - futures, swaps, options, and any other derivatives - that express a risky position, such as IG9 (long or short), or for that matter any security that simply needs initial margin, and better yet, allows massive leverage. For example the ES, aka E-mini contract, which as everyone knows is the main driver of market risk in the US capital markets, and which allows for .

And that's it. We, or rather JPMorgan, demonstrated how excess reserves, without ever leaving a bank's balance sheet and being used to actually purchase securities, can be transformed, via lending and rehypothecation, and thanks to incremental leverage on the underlying cash, are able to generate far greater returns to commercial banks (or rather their prop trading groups, such as JPM's CIO) than simply lending out said cash. This shows that for as long as the Fed is engaged in withdrawing quality collateral (via QE), a bank's liquidity preference will always be to using reserve cash as collateral instead of lending it out (in the process further lowering the velocity of money, but who cares as long as the bank's ROI is the highest possible). All of this, of course, is made possible thanks to Glass-Steagall which allows banks to take deposit, reserve or any other sources of funds, and lever them up via prop trading desks and generate outsized returns.

Which takes us back to Stella's punchline:

There is a great irony in the journalistic history of monetary policy. What many are calling central bank “money creation” “helicopter money” or “rolling the printing presses” may – in combination with tighter leverage ratios – lead to a tightening of bank credit and deflationary pressures. And all this is occurring while the spectre of uncontrolled credit expansion and monetary debasement are being decried countless times by those who have not recognized that yesteryear’s monetary paradigm is defunct.

Ah yes, the spectre of uncontrolled credit expansion may be defunct, but that does not mean that the "helicopter money" created by the Fed is not re-entering capital markets. As shown above, and as anyone can see when looking at daily record highs in the S&P500, it most certainly is.

For that matter, banks couldn't care one bit if the underlying reserves are inert and excluded from non-bank participants: what is far more important is that its margined equivalent in the capital markets, is perfectly fungible, and that the cash collateral supporting it can and will result in much higher asset prices with every day that Bernanke injects more liquidity into bank reserves and thus, deposits.

Of course, the flipside is the inverse: once bank liquidity preference inverts, if and when the Fed were to finally engage in exiting its current policy, one effect would be the immediate collapse of the stock market (and any other marginable) bubble.

However, the resulting monetary expansion via far more conventional lending channels would then promptly, and long-overdue, re-enter the broader economy. The paradox is that for the Fed to finally start "fixing" the economy, instead of the brokerage accounts of a few billionaires, it has to finally stop QE, because as long as it is running, the only "inflationary" sink hole will be global risk markets, and the only thing levitating are all asset prices enveloped in this bubble.

The far bigger problem is that once all those risky positions which have found a price-clearing manifestation through capital markets, and are leveraged exponentially more than the mere $2.2 trillion in reserves injected to date by the Fed, begin to unwind, the "flow" exodus away from paper and into physical assets of all shapes and sizes (i.e., BLS-measured inflation) will be precisely the long-deferred advent of all that inflation which the Fed had so far been able to redirect into market asset bubbles.

At that point, when faced with a liquidity tsunami in full reverse mode away from asset bubbles, the last thing on anyone's mind unfortunately will be whether the proper liquidity extraction mechanism will be Reverse Repos or Term Deposits.

But for things to get there, the US banking system has to be ready and willing to allow the great asset bubble deleveraging, which also means having bought sufficient amounts of hard assets in advance, mostly from their clients, ahead of the great "paper asset" unrotation. Keep a close watch for even more aggressive "sell" recommendations for gold, silver, and everything else that can be nailed down...

On the subject of reverse repos , the Fed is " testing " them now .....

Fed Soaks Up $11.8 Billion In Liquidity In First Fixed-Rate Reverse Repo Test

As further explained (confounded) by Bill Dudley as part of his speech earlier today, the Fed is pushing on with its Fixed-Rate Reverse Repo test, which while supposedly is meant to assist the Fed in extracting liquidity from the market once the mythical balance sheet unwind begins, what it really does is set a level the playing field for banks and non-banks, by disintermediating their collateral eligibility, and in the process collapsing the spread between the IOER and General Collateral rates. It will likely have many more side effects, now that non-banks can compete with banks for the Fed's IOER, all of which will be largely unexpected and as the impact on collateral bifurcation moves from the purely theoretical to the real world.

As noted below, in the first Fixed-Rate RRP test, the Fed soaked up $11.8 billion in cash in exchange for Treasury collateral at a stop out rate of 0.01%, largely in line with G/C.

Source: NY Fed

Fisher comments today.....

http://www.zerohedge.com/news/2013-09-23/bernankus-maximus-richard-fisher-exposes-chairman-dictator

Bernankus Maximus: Richard Fisher Exposes The Chairman Dictator

Perhaps no sentence sums up the dismal reality investors face with the 'communications' strategy, the credibility, and the actions of the Federal Reserve, better than the following statement from Dallas Fed's Fisher:

- FED'S FISHER SAYS VOTE LAST WEEK NOT TO TAPER DID NOT REFLECT THE DISCUSSION AT THE POLICY-SETTING TABLE

It seems that we should therefore ignore each and every Fed whisperer and President (voting or non-voting) as only man counts... Et Tu Yellen...

and....

http://www.zerohedge.com/news/2013-09-23/another-fed-president-confirms-fed-credibility-undermined

Another Fed President Confirms Fed Credibility Undermined

We have heard from the doves, now the hawks. Dallas Fed's Fisher (a non-voting member) pulls no punches in his speech this morning. Confirming Esther George's comments last week, and our views on the same:

- *FISHER SAYS HE TRIED LAST WEEK TO PERSUADE FOMC TO TAPER QE

- *FISHER SAYS DECISION NOT TO TAPER QE UNDERMINED FED CREDIBILITY

But that was not it. The well-known hawk went to warn that:

- *FISHER: BIGGEST BANKS ARE `DAGGER POINTED' AT ECONOMY'S HEART

- *FISHER SAYS NO QE TAPER ADDS TO `UNCERTAINTY' ABOUT FED POLICY

None of this should come as a surprise asFisher told Santelli earlier in the year that "this cannot go on forever!"

when doves cry for QE.......

The Doves Hit The Tape: Dudley, Lockart Plead For More QE

Submitted by Tyler Durden on 09/23/2013 - 09:34

As expected, here come the first two doves "explaining" the reasons behind Bernanke's taper surprise last week:

- DUDLEY SAYS FED MUST ACT ‘FORCEFULLY’ TO PUSH AGAINST HEADWINDS

- DUDLEY: MAY TAKE CONSIDERABLE TIME TO REACH 6.5% JOBLESS LEVEL

- DUDLEY SAYS ECONOMY STILL NEEDS `VERY ACCOMMODATIVE' POLICY

And Lockhart adds to the chorus:

- LOCKHART SAYS FED FOCUS SHOULD BE FASTER U.S. ECONOMIC GROWTH

- LOCKHART HAS BACKED FED'S ASSET PURCHASE PROGRAM

- LOCKHART SEES `SOME SLOWING' IN U.S. PAYROLL GROWTH

Translation: much more "high-quality collateral" to be extracted from the system.

Good morning Fred,

ReplyDeleteI'm with you, I wouldn't care who rescued me, I just found that odd.

It's nice to know that Merkel's life is probably going to be more difficult, I really don't like that lady.

And I love the graph in this article, makes my confusion of PM prices all the more confused though.

http://www.zerohedge.com/news/2013-09-22/guest-post-gold-and-monetary-inflation-prospects

Have a great day

Morning Kev - SDP already signaling it's on Merkel to try to form a government , not going to rollover for her this time !

ReplyDeletePMs are captive to manipulations ( there are no markets , just manipulations . )