http://www.blacklistednews.com/What_Is_Going_To_Happen_If_Interest_Rates_Continue_To_Rise_Rapidly%3F/28164/0/38/38/Y/M.html

( Keep your eyes on the ten year bond - what happens if we get to 3.50 percent ? some say a disorderly unwind could be in store ! )

If you want to track how close we are to the next financial collapse, there is one number that you need to be watching above all others. The number that I am talking about is the yield on 10 year U.S. Treasuries, because it affects thousands of other interest rates in our financial system. When the yield on 10 year U.S. Treasuries goes up, that is bad for the U.S. economy because it pushes long-term interest rates up. When interest rates rise, it constricts the flow of credit, and a healthy flow of credit is absolutely essential to the debt-based system that we live in. Just imagine someone squeezing a tube that has water flowing through it. The higher interest rates go, the more economic activity will be squeezed. If interest rates continue to rise rapidly, it will be more expensive for the U.S. government to borrow money, it will be more expensive for state and local governments to borrow money, the housing market may crash again, consumer debt will become more expensive, junk bond investors will be in for a world of hurt, the stock market will experience a tremendous amount of pain and there is a good chance that we could see the 441 trillion dollar interest rate derivatives bubbleimplode. And that is just for starters.

If you want to track how close we are to the next financial collapse, there is one number that you need to be watching above all others. The number that I am talking about is the yield on 10 year U.S. Treasuries, because it affects thousands of other interest rates in our financial system. When the yield on 10 year U.S. Treasuries goes up, that is bad for the U.S. economy because it pushes long-term interest rates up. When interest rates rise, it constricts the flow of credit, and a healthy flow of credit is absolutely essential to the debt-based system that we live in. Just imagine someone squeezing a tube that has water flowing through it. The higher interest rates go, the more economic activity will be squeezed. If interest rates continue to rise rapidly, it will be more expensive for the U.S. government to borrow money, it will be more expensive for state and local governments to borrow money, the housing market may crash again, consumer debt will become more expensive, junk bond investors will be in for a world of hurt, the stock market will experience a tremendous amount of pain and there is a good chance that we could see the 441 trillion dollar interest rate derivatives bubbleimplode. And that is just for starters.

http://www.zerohedge.com/news/2013-08-15/good-luck-unwinding

( Benjy in the box ? )

Submitted by Tyler Durden on 08/15/2013 20:08 -0400

Submitted by Tyler Durden on 08/15/2013 20:08 -0400

http://hat4uk.wordpress.com/2013/08/15/bond-wars-shock-as-stats-reveal-wests-creditors-out-to-protect-their-assets/

http://www.zerohedge.com/news/2013-08-15/10y-yield-jumps-new-2-year-high

( based on the chart , things will get nuts if we cross 3.00 on the ten year - expect a big effort to try pin the ten year at 2.75 percent ! Update after 8:30 data - ten year at 2.80 ! ! Stocks , bonds gold selling off as data supports sept taper ! )

Submitted by Tyler Durden on 08/15/2013 08:24 -0400

http://hat4uk.wordpress.com/2013/08/15/interest-rates-more-signs-that-they-cant-be-controlled/

For those who think this article is repost of our May recap of Wal-Mart's Q1 earnings, you are forgiven: after all it was almost a carbon copy: "Wal-Mart Misses Revenue, Guides Below Expectations: Weather Among Factors Blamed." Well, as we expected, Wal-Mart just missed, and guided lower, although at least the company appears not to have blamed the weather for the second quarter in a row. Of course, that does not mean WMT didn't find spacegoats, and while it blamed the usual suspects of consumer spending and FX headwinds, it also accused the payroll tax of being the reason for a 0.5% drop in comp store sales. But didn't economists everywhere say the payroll tax' impact is now neligible? Finally, WMT blames the lack of grocery inflation. Really? Maybe stop cutting the price-equivalent size of your portions and the inflation will materialize.

For those who think this article is repost of our May recap of Wal-Mart's Q1 earnings, you are forgiven: after all it was almost a carbon copy: "Wal-Mart Misses Revenue, Guides Below Expectations: Weather Among Factors Blamed." Well, as we expected, Wal-Mart just missed, and guided lower, although at least the company appears not to have blamed the weather for the second quarter in a row. Of course, that does not mean WMT didn't find spacegoats, and while it blamed the usual suspects of consumer spending and FX headwinds, it also accused the payroll tax of being the reason for a 0.5% drop in comp store sales. But didn't economists everywhere say the payroll tax' impact is now neligible? Finally, WMT blames the lack of grocery inflation. Really? Maybe stop cutting the price-equivalent size of your portions and the inflation will materialize.

Something funny happened on the road to the epic consumer balance sheet cleansing and subsequent releveraging (without which there can be noactual non-Fed sugar high fueled recovery):the second quarter. And specifically, as the Fed just disclosed in its quarterly Household Debt and Credit Report, the number of consumer bankruptcies during the second quarter, just jumped by 71K, to 380K from 309K in Q1, the biggest quarterly jump in precisely three years - on both an absolute and relative basis - and the most since the 158K jump recorded in Q2 2010. It appears that when the "releveraging" US consumer isn't busy buying stuff on credit, they are just as busy filing for bankruptcy. Healthy consumer-led recovery and all that.

Something funny happened on the road to the epic consumer balance sheet cleansing and subsequent releveraging (without which there can be noactual non-Fed sugar high fueled recovery):the second quarter. And specifically, as the Fed just disclosed in its quarterly Household Debt and Credit Report, the number of consumer bankruptcies during the second quarter, just jumped by 71K, to 380K from 309K in Q1, the biggest quarterly jump in precisely three years - on both an absolute and relative basis - and the most since the 158K jump recorded in Q2 2010. It appears that when the "releveraging" US consumer isn't busy buying stuff on credit, they are just as busy filing for bankruptcy. Healthy consumer-led recovery and all that.

( Keep your eyes on the ten year bond - what happens if we get to 3.50 percent ? some say a disorderly unwind could be in store ! )

What Is Going To Happen If Interest Rates Continue To Rise Rapidly?

August 16, 2013If you want to track how close we are to the next financial collapse, there is one number that you need to be watching above all others. The number that I am talking about is the yield on 10 year U.S. Treasuries, because it affects thousands of other interest rates in our financial system. When the yield on 10 year U.S. Treasuries goes up, that is bad for the U.S. economy because it pushes long-term interest rates up. When interest rates rise, it constricts the flow of credit, and a healthy flow of credit is absolutely essential to the debt-based system that we live in. Just imagine someone squeezing a tube that has water flowing through it. The higher interest rates go, the more economic activity will be squeezed. If interest rates continue to rise rapidly, it will be more expensive for the U.S. government to borrow money, it will be more expensive for state and local governments to borrow money, the housing market may crash again, consumer debt will become more expensive, junk bond investors will be in for a world of hurt, the stock market will experience a tremendous amount of pain and there is a good chance that we could see the 441 trillion dollar interest rate derivatives bubbleimplode. And that is just for starters.

So yes, we all need to be carefully watching the yield on 10 year U.S. Treasuries. On Friday, it opened at 2.76% and hit a high of 2.86% before closing at 2.83%. The yield on 10 year U.S. Treasuries is up nearly 120 basis points since the beginning of May, and almost everyone on Wall Street seems convinced that it is going to go much higher.

We are truly moving into unprecedented territory, because we have been in a bull market for U.S. Treasuries for the last 30 years. Many investors don't even know that it is possible to lose money on U.S. Treasuries. They have been described as "risk-free" investments, but that is far from the truth.

In fact, we could see bond investors of all types end up losing trillions of dollars before it is all said and done.

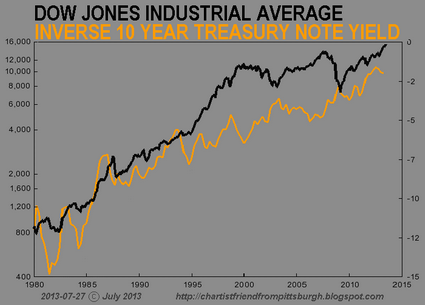

And those in the stock market will lose lots of money too. Low interest rates are good for economic activity which is good for the stock market. The chart posted below was created byChartist Friend from Pittsburgh, and it shows that stock prices have generally risen as the yield on 10 year U.S. Treasuries has steadily declined over the past 30 years...

When interest rates rise, that is bad for economic activity and bad for stocks. That is why so many stock analysts are alarmed that interest rates are going up so rapidly right now.

And as I wrote about the other day, we have just witnessed the largest cluster of Hindenburg Omens that we have seen since before the last financial crisis. The stock market already seems ripe for a huge "adjustment", and rising interest rates could give it a huge extra push in a negative direction.

By the time it is all said and done, stock market investors could end up losing trillions of dollars in the next stock market crash.

In addition, rising interest rates could easily precipitate another housing crash. As the Wall Street Journal discussed on Friday, as the yield on 10 year U.S. Treasuries goes up it will also cause mortgage rates to rise...

Yes, of course it will be much harder. In fact, there is a good chance that you will have to reduce your selling price significantly so that prospective buyers can afford the payments.

Let us hope that the yield on 10 year U.S. Treasuries levels off for a while. If it says at this current level, the damage will probably not be too bad.

But if it crosses the 3 percent mark and keeps soaring, things could get messy pretty quickly. In fact, according to a Bank of America Merrill Lynch investor survey, the 3.5 percent mark is when the collapse of the bond market is likely to become "disorderly"...

Well, there are a number of factors of course, but one very disturbing sign is that foreigners are selling off U.S. Treasuries at a pace that we have not seen since 2007...

Well, it looks like it may be starting to happen.

Unfortunately, there is no way that the party that the U.S. government has been throwing can continue without foreigners buying our debt. We have added more than 11 trillion dollars to the national debt since the year 2000, and according to Boston University economist Laurence Kotlikoff we are facing unfunded liabilities in future years that are in excess of 200 trillion dollars.

Even with foreigners continuing to loan us gigantic mountains of super cheap money, it would still take a doubling of our taxes to put us on a fiscally sustainable course...

Very few Americans could.

But that is how serious the financial problems of the federal government are.

And all of the above assumes that interest payments on U.S. government debt will remain at current levels. If the average rate of interest on U.S. government debt rises to just 6 percent, the U.S. government will be paying out a trillion dollars a year just in interest on the national debt.

Also, all of the above assumes that we will have a healthy financial system that does not need to be bailed out again.

But if rapidly rising interest rates cause the 441 trillion dollar interest rate derivatives bubble to implode, the bailout that the "too big to fail" banks will need will likely be far, far larger than last time.

In fact, once that bubble bursts there probably will not be enough money in the entire world to fix it.

If the picture that I have painted above sounds bleak, that is because it is bleak.

Sometimes I get frustrated with myself because I don't feel I am communicating the tremendous danger that we are facing accurately enough.

We are heading for the worst financial crisis in modern human history, and the debt-fueled prosperity that we are enjoying today is going to go away and it is never going to come back.

You can dismiss that as "doom and gloom" and stick your head in the sand if you want, but that isn't going to help anything. Instead of ignoring reality you should be working hard to prepare your family for what is coming and warning others that they should be getting prepared too.

When a hurricane is approaching landfall, you don't take your family out for a picnic at the beach. That would be foolish. Unfortunately, way too many Americans are acting as if nothing like the financial crisis of 2008 could ever possibly happen again.

If you deceive yourself into thinking that all of this is going to have a happy ending somehow, you are going to get blindsided by the coming storm.

But if you make preparations now, you might just be okay.

There is hope in understanding what is happening and there is hope in getting prepared.

We are truly moving into unprecedented territory, because we have been in a bull market for U.S. Treasuries for the last 30 years. Many investors don't even know that it is possible to lose money on U.S. Treasuries. They have been described as "risk-free" investments, but that is far from the truth.

In fact, we could see bond investors of all types end up losing trillions of dollars before it is all said and done.

And those in the stock market will lose lots of money too. Low interest rates are good for economic activity which is good for the stock market. The chart posted below was created byChartist Friend from Pittsburgh, and it shows that stock prices have generally risen as the yield on 10 year U.S. Treasuries has steadily declined over the past 30 years...

When interest rates rise, that is bad for economic activity and bad for stocks. That is why so many stock analysts are alarmed that interest rates are going up so rapidly right now.

And as I wrote about the other day, we have just witnessed the largest cluster of Hindenburg Omens that we have seen since before the last financial crisis. The stock market already seems ripe for a huge "adjustment", and rising interest rates could give it a huge extra push in a negative direction.

By the time it is all said and done, stock market investors could end up losing trillions of dollars in the next stock market crash.

In addition, rising interest rates could easily precipitate another housing crash. As the Wall Street Journal discussed on Friday, as the yield on 10 year U.S. Treasuries goes up it will also cause mortgage rates to rise...

Higher yields will push up long-term borrowing cost for U.S. consumers and businesses. Mortgage rates will rise, and investors are keeping a close eye on whether this may derail the recovery of the housing market, which has shown signs of turning a corner this year.In one of my previous articles, I included an example that shows just how powerful rising mortgage rates can be...

A year ago, the 30 year rate was sitting at 3.66 percent. The monthly payment on a 30 year, $300,000 mortgage at that rate would be $1374.07.If you own a $300,000 house today, do you think it will be easier to sell it or harder to sell it if mortgage rates skyrocket?

If the 30 year rate rises to 8 percent, the monthly payment on a 30 year, $300,000 mortgage at that rate would be $2201.29.

Does 8 percent sound crazy to you?

It shouldn't. 8 percent was considered to be normal back in the year 2000.

Yes, of course it will be much harder. In fact, there is a good chance that you will have to reduce your selling price significantly so that prospective buyers can afford the payments.

Let us hope that the yield on 10 year U.S. Treasuries levels off for a while. If it says at this current level, the damage will probably not be too bad.

But if it crosses the 3 percent mark and keeps soaring, things could get messy pretty quickly. In fact, according to a Bank of America Merrill Lynch investor survey, the 3.5 percent mark is when the collapse of the bond market is likely to become "disorderly"...

Our latest Credit Investor Survey, conducted July 8-11, showed that 3.5% on the 10-year is most commonly thought of as the trigger of a disorderly rotation – i.e. higher interest rates leading to outflows and wider credit spreads – among high grade investors.So what is causing this?

Put differently, 3.0% on the 10-year will not lead to overall wider credit spreads if there is enough buying interest from institutional investors (though note that the 10s/30s spread curve would flatten further, as mutual fund/ETF holdings are concentrated in the belly of the curve, whereas institutional demand is disproportional in the long end of the curve). However, if the probability of a further move higher in interest rates to 3.5% is high – which will be the perception if interest rate volatility is high – certain institutional investors will choose to remain on the sidelines.

Thus there may not be enough institutional buying interest to mitigate retail fund outflows and contain overall high grade spread levels.

Well, there are a number of factors of course, but one very disturbing sign is that foreigners are selling off U.S. Treasuries at a pace that we have not seen since 2007...

One of the biggest fears in the financial markets is that foreign investors will stop buying U.S. Treasury securities, causing borrowing rates to surge.Do you remember all of the warnings that we have received over the years about what would take place when foreign countries started dumping U.S. debt?

Not that this is the beginning of a frightening trend, but new data from the Treasury Department shows that foreigners were net sellers in June. In fact, this is the largest net sale of U.S. securities since August 2007.

Well, it looks like it may be starting to happen.

Unfortunately, there is no way that the party that the U.S. government has been throwing can continue without foreigners buying our debt. We have added more than 11 trillion dollars to the national debt since the year 2000, and according to Boston University economist Laurence Kotlikoff we are facing unfunded liabilities in future years that are in excess of 200 trillion dollars.

Even with foreigners continuing to loan us gigantic mountains of super cheap money, it would still take a doubling of our taxes to put us on a fiscally sustainable course...

Writing in the September issue of Finance and Development, a journal of the International Monetary Fund, Prof. Kotlikoff says the IMF itself has quietly confirmed that the U.S. is in terrible fiscal trouble - far worse than the Washington-based lender of last resort has previously acknowledged. "The U.S. fiscal gap is huge," the IMF asserted in a June report. "Closing the fiscal gap requires a permanent annual fiscal adjustment equal to about 14 per cent of U.S. GDP."Can you afford to pay twice as much in taxes to the federal government?

This sum is equal to all current U.S. federal taxes combined. The consequences of the IMF's fiscal fix, a doubling of federal taxes in perpetuity, would be appalling - and possibly worse than appalling.

Prof. Kotlikoff says: "The IMF is saying that, to close this fiscal gap [by taxation] would require an immediate and permanent doubling of our personal income taxes, our corporate taxes and all other federal taxes.

"America's fiscal gap is enormous - so massive that closing it appears impossible without immediate and radical reforms to its health care, tax and Social Security systems - as well as military and other discretionary spending cuts."

Very few Americans could.

But that is how serious the financial problems of the federal government are.

And all of the above assumes that interest payments on U.S. government debt will remain at current levels. If the average rate of interest on U.S. government debt rises to just 6 percent, the U.S. government will be paying out a trillion dollars a year just in interest on the national debt.

Also, all of the above assumes that we will have a healthy financial system that does not need to be bailed out again.

But if rapidly rising interest rates cause the 441 trillion dollar interest rate derivatives bubble to implode, the bailout that the "too big to fail" banks will need will likely be far, far larger than last time.

In fact, once that bubble bursts there probably will not be enough money in the entire world to fix it.

If the picture that I have painted above sounds bleak, that is because it is bleak.

Sometimes I get frustrated with myself because I don't feel I am communicating the tremendous danger that we are facing accurately enough.

We are heading for the worst financial crisis in modern human history, and the debt-fueled prosperity that we are enjoying today is going to go away and it is never going to come back.

You can dismiss that as "doom and gloom" and stick your head in the sand if you want, but that isn't going to help anything. Instead of ignoring reality you should be working hard to prepare your family for what is coming and warning others that they should be getting prepared too.

When a hurricane is approaching landfall, you don't take your family out for a picnic at the beach. That would be foolish. Unfortunately, way too many Americans are acting as if nothing like the financial crisis of 2008 could ever possibly happen again.

If you deceive yourself into thinking that all of this is going to have a happy ending somehow, you are going to get blindsided by the coming storm.

But if you make preparations now, you might just be okay.

There is hope in understanding what is happening and there is hope in getting prepared.

So watch the yield on 10 year U.S. Treasuries. The higher it goes, the later in the game we are.

http://www.zerohedge.com/news/2013-08-15/good-luck-unwinding

( Benjy in the box ? )

Good Luck Unwinding That

A few months ago, when discussing the most pertinent topic for Bernanke and his merry central-planning men we said that "with every passing week, the Fed's creeping takeover of the US bond market absorbs just under 0.3% of all TSY bonds outstanding: a pace which means the Fed will own 45% of all in 2014, 60% in 2015, 75% in 2016 and 90% or so by the end of 2017 (and if the US budget deficit is indeed contracting, these targets will be hit far sooner). By the end of 2018 there would be no privately held US treasury paper. Still think QE can go on for ever?" What followed was 3 months of heated debate on whether the Fed will or will not taper which for some reason were focusing on the wrong thing - the economy. Ironically, how the economy is doing has nothing to do with the Fed's decision, which is entirely decided by the increasing shortage of private sector "quality collateral" i.e., bonds.

How big is this shortage? As noted above, the Fed's literally absorbs ~0.3% of the bond market each week. And according to the most recently released Fed balance sheet data, this is indeed the case. According to SMRA calculations, the Fed owned about 31.47% of the total outstanding ten year equivalents. This is above the 31.24% from the prior week, and higher than the 30.99% from the week before - a rate of increase almost in line with what we predicted.Inversely this means that the percentage of ten-year equivalents available to the private sector decreased to 68.53% from 68.76% in the prior week. Long story short, the Fed just soaked up 0.23% of the bond market in one week and half a percent in two weeks, a ratio that will only increase in time, and unless there is a taper, may reach 0.5% per week.

At that level of bond market "takeover", the liquidity in what was once the world's most liquidity bond market, already lamented by the TBAC as we showed earlier this week, will evaporate entirely and the daily bond halts that were a norm in Japan in April and May will promptly come to the US. Only at that point, unlike the BOJ which had the Fed to fall back on, there will be no Plan B, as the opportunity cost of an illiquid bond market is the reserve currency status of the dollar and the credibility of the Fed - the two are interchangeable. Which also means the future of the entire global fiat system will be on the brink.

Which brings us to the point of this post.

Clueless economists and pundits are happy to trot out every now and then a chart showing the ratio of the Fed's balance sheet to GDP, which supposedly is meant to indicate that the Fed owning 20% of US GDP on its books is normal.

What said clueless economists never seem to grasp is that a Fed whose balance sheet is full of 3 month bills is completely different than a Fed whose balance sheet is full of 30 Year bonds. And the best way to represent that is by showing the 10 Year equivalent holdings of the Fed.

Presenting Exhibit A: the Fed's balance sheet represented in the form of 10 Year equivalent holdings.

The long-term average is ~4%. As noted above, it just hit 31.47% this week. And even with a taper (especially since the untaper will be just around the corner once the market crashes and the Fed has no choice but to jump right in), we fully expect that the Fed will hit its current SOMA limit of 70% of any and every CUSIP across the curve by 2016.

Take one look at the chart above, and extrapolate it reaching twice as high.

And then imagine how this Mt. Everest of 10 Year equivalents will be unwound.

Good luck with that.

http://hat4uk.wordpress.com/2013/08/15/bond-wars-shock-as-stats-reveal-wests-creditors-out-to-protect-their-assets/

BOND WARS: Shock as stats reveal West’s creditors out to protect their assets

China, Japan big sellers of T-Bonds

Further to this morning’s post here, the point I’m making – that nobody, no matter how smart, can manipulate borrowing rates down if some folks would rather row in the opposite direction – has been hammered home by some new data to hand.

I wrote ten hours ago, ‘The entire shtick about ‘interest rates’ is really largely significant in terms of what it costs big Sovereign debtors to borrow’. What now emerges is that the lastest T-Bond figures show very clearly how the biggest selling came from America’s two largest creditors, China and Japan. The more the creditors sell, the more supply exceeds demand, so the higher the yield the US (and us, and the EU) have to offer. Ergo, just as Bernanke gives the ‘tapering off’ hint – and the US deficit resolutely refuses to get any smaller – the Other Side starts hiking up the borrowing cost.

This has been spotted quickly – and resulted in something of a Dow sell-off: less than a quarter of the way through the Wall Street day, the DJIA has fallen more than it did in the three preceding days. Uncle Ben is in a corner, and the markets know it.

Looking at this for a second in the bigger context of just how wonderful and unalternatived this fabbo Globalist financial form of capitalism is, let’s just summarise how well the world – this mythical, risible Global Village of Ted Leveragitt – is pulling together.

First we have the Japanese, those ever-popular people in Asia, screwing the arse off all their neighbours by trying to become a low-cost producer through QE and currency manipulation. So the Chinese and Koreans are buying the Japanese Yen. Then we have the tricksy, overborrowing US employing QE to pump the stock market and devalue the currency, but with China and Japan buying the Dollar to keep it strong, and selling US Bonds to make it tough for them to just keep borrowing and inflate away the debt.

Every time Mario Draghi tries to force down the euro for competitive reasons, the Swiss sell billions of SFr to keep their currency competitive. Every time the UK buys the euro to keep the Pound competitive, the ECB buys the Pound; and when the ECB buys its own currency for confidence-boosting reasons, the BoE flogs it to get the eunatics back to the negotiating table about British EU rights outside the eurozone.

Am I the only one who sees this is a disastrous, unproductive and thus utterly pointless waste of talent and effort? Surely it could be put to far better use designing a communitarian, non-dependent form of self-supporting capitalism with trade in the excess…..rather than this mercantilist war-game? And who is to say, as things get more desperate, it is going to remain a game?

All over my little blogosphere niche, I can hear the scratching of pencils on pigeon coops, as people write “The Slog…idealistic fluffy Red tree-hugger”. Well, please yourselves as Frankie Howerd used to say.

http://www.zerohedge.com/news/2013-08-15/10y-yield-jumps-new-2-year-high

( based on the chart , things will get nuts if we cross 3.00 on the ten year - expect a big effort to try pin the ten year at 2.75 percent ! Update after 8:30 data - ten year at 2.80 ! ! Stocks , bonds gold selling off as data supports sept taper ! )

Trifecta Of CPI, Initial Claims And Empire Manufacturing All In Line, And All Pushing The Market Lower

Submitted by Tyler Durden on 08/15/2013 - 08:46

If there was one thing the bulls did not want this morning, it was a goldilocks report in the trifecta of economic data, which included CPI, Initial Claims and the Empire Fed. Sadly, Goldilocks is precisely what they got with CPI printing just as expected, up 0.2% from June, and up 2.0% from a year ago (ex food and energy also in line at 0.2%), claims coming modestly better than expected at 320K vs Expectations of 325K, and finally the Empire Fed offsetting the slight claims beat by printing at 8.24 on expectations of 10.00, down from 9.46 in July. As a reminder, only a big economic shock could have derailed the Fed's September taper intentions. So far it is not coming, which means only the August NFP report is left.

10Y Yield Jumps To New 2 Year High

Up 115bps in 3 months, the 10Y Treasury bond yield just broke above 2.7535% - a level not seen since August 2011. The 3.5% 'disorderly rotation' level remains the next 'target' but we can't help but notice the similarity to the Oct 2010 to Feb 2011 move...

http://hat4uk.wordpress.com/2013/08/15/interest-rates-more-signs-that-they-cant-be-controlled/

INTEREST RATES: More signs that they can’t be controlled.

Whether they like it or not, debtor nation borrowing rates are rising

I get a terrible feeling some days that nobody at the top is paying attention 95% of the time; and on those rare occasions when the MoUs are awake, they plump with clinical accuracy for the route that is doomed. Alongside this more or less continual train wreck are 56 million people clearly so busy doing something, they don’t have time to notice the trackside strewn with wrecked carriages and horribly twisted bodies as they race by on a TGV towards the cliff.

Two years ago, I posted this piece bluntly pointing out that the Lloyds branches sale would end in tears. It certainly did for the Co-op, which – following the Britannia marriage from Hell and the exposure of undercapitalisation – now faces the UK’s first bailin. Nobody seems to have noticed that between them, Ministerial dating agencies, the EU, reckless Co-Op management and banking insanity have done for a huge mutual concern…and that we’re going to be paying for it. So when the neoliberals rewrite yet more history, there won’t be any outcry.

Six months ago I devoted the second half of this Saturday Essay to pointing out why, come what may, interest rates must rise….whatever Fred Karno at the Bank of England says. Yesterday the interbank mortgage rates were reported to be on the rise. “It shows that while Carney says one thing, the markets think another with at least one base rate rise priced in,” according to Mark Harris of mortgage broker SPF Private Clients. “Can he really keep a lid on rates until 2016?” To which the obvious answer is, no. The piece about this at the Telegraph yesterday afternoon has thus far garnered…just 19 comments.

Yesterday, the yield on the 10-year German Bund was, at 1.81%, just a rice-paper off a 16-month high it hit two months ago. And this despite the “eurozone out of recession” bollocks of earlier in the week. Across the pond, 10-year US Treasury bond yields at 2.71% are in turn very close indeed to a two year high.

On Tuesday, The yield on 10-year UK gilts rose above 2.6% – the highest since October 2011.

What we’re seeing here is the markets beginning to ignore the bollocks. Take the EU’s “great news” of earlier this week:

“It is, of course, appropriate to temper any euphoria about today’s upside news with a reminder that, in our view, the recovery in the euro area will be protracted and somewhat underwhelming,” said James Ashley, senior economist at RBC Capital Markets, “We see little prospect that this positive second-quarter reading will serve as a launch-pad to a strong resurgence across the region over the next few quarters.”

Or, in a word, phuuurrrt.

Last month, interest rates rose in India, but at the end of the month they were kept on hold by the Government. This made little difference to the country’s banks: within a day of the RBI’s status-quo policy, private sector Bank ‘Yes’ raised lending and fixed deposit rates by 0.5%.

Anyway, here we are on August 15th, a couple of weeks from Labor Day and the end of the European holidays. The entire shtick about ‘interest rates’ is really largely significant in terms of what it costs big Sovereign debtors to borrow. Whether the clowns at the top want it or not, those costs are rising. My view remains that it’s only a matter of time before the markets analyse the corner into which everyone in the West is now painted, and respond. I think they will vote “No Confidence”.

Just watch the sparks fly when they do.

Rising rates as leading companies report disappointing earning results , US consumer bankruptcy filings at a three year high , full time jobs fading away like mist ..... flashing red lights , folks !

Wal-Mart Misses, Guides Below Expectations; Blames Weak Consumer Spending, Payroll Tax, FX And Lack Of Inflation

Submitted by Tyler Durden on 08/15/2013 - 07:20For those who think this article is repost of our May recap of Wal-Mart's Q1 earnings, you are forgiven: after all it was almost a carbon copy: "Wal-Mart Misses Revenue, Guides Below Expectations: Weather Among Factors Blamed." Well, as we expected, Wal-Mart just missed, and guided lower, although at least the company appears not to have blamed the weather for the second quarter in a row. Of course, that does not mean WMT didn't find spacegoats, and while it blamed the usual suspects of consumer spending and FX headwinds, it also accused the payroll tax of being the reason for a 0.5% drop in comp store sales. But didn't economists everywhere say the payroll tax' impact is now neligible? Finally, WMT blames the lack of grocery inflation. Really? Maybe stop cutting the price-equivalent size of your portions and the inflation will materialize.CSCO Crashes 10% After-Hours, Laying Off 4000 Staff, Sees Weak Q4

Submitted by Tyler Durden on 08/14/2013 - 17:32

It seems like it was just yesterday when CSCOannounced it would fire 10,000 people. And then another 1,300. And then another 500. Fast forward to today when the "one-time, non-recurring" termination charges are back, as the "recovery", now in its 5th year, progresses a little differently than expected, this time with another 4,000 FTE told to pack their bags.

CISCO TO CUT 4,000 JOBS OR 5% OF WORKFORCE

CISCO SAYS IT REMAINS 'VERY MUCH A COMPANY ON THE OFFENSIVE'

CISCO SAYS IT REMAINS 'VERY MUCH A COMPANY ON THE OFFENSIVE'

Nobody can blame the company, however: why keep full-time workers, when switching over to part-timers will do just as fine, and generate significant benefits to the bottom line and shareholders.

US Consumer Bankruptcies Jump By Most In Three Years; Third-Party Collections At All Time High

Submitted by Tyler Durden on 08/14/2013 - 16:36Something funny happened on the road to the epic consumer balance sheet cleansing and subsequent releveraging (without which there can be noactual non-Fed sugar high fueled recovery):the second quarter. And specifically, as the Fed just disclosed in its quarterly Household Debt and Credit Report, the number of consumer bankruptcies during the second quarter, just jumped by 71K, to 380K from 309K in Q1, the biggest quarterly jump in precisely three years - on both an absolute and relative basis - and the most since the 158K jump recorded in Q2 2010. It appears that when the "releveraging" US consumer isn't busy buying stuff on credit, they are just as busy filing for bankruptcy. Healthy consumer-led recovery and all that.The "Obamacare Part-Time Jobs" Effect Goes Mainstream

Submitted by Tyler Durden on 08/14/2013 - 21:50

While many Wall Street economists and strategists shrugged in the face of tin-foil-hat-wearing bloggers who suggested the disaster that is the part-time jobs receovery was due to The Affordable Care Act - of 953,000 jobs created In 2013, 77%, or 731,000 are part-time - epitomized best by Larry Kudlow and Deutsche Bank's ever-smiling Joe Lavorgna; it seems the drag on employers' hiring has now hit the mainstream media. As NBC Nightly News reports in this succinct clip, things are not going according to plan for the President's better bargain even as Fed's Bullard proclaims "clear improvement in labor markets." Perhaps he should watch TV this evening?

http://blogs.wsj.com/economics/2013/08/09/food-stamp-use-rises-some-15-of-u-s-gets-benefits/

( How can there be an " real " job growth when food stamp use grows every month ! )

Food-stamp use rose 2.4% in the U.S. in May from a year earlier, with more than 15% of the U.S. population receiving benefits. (See an interactive map with data on use since 1990.)

One of the federal government’s biggest social welfare programs, which expanded when the economy convulsed, isn’t shrinking back alongside the recovery.

Food stamp rolls were up 0.2% from the prior month, the U.S. Department of Agriculture reported in data that aren’t adjusted for seasonal variations. Though annual growth continues, the pace has slowed since the depths of the recession.

The number of recipients in the food stamp program, formally known as the Supplemental Nutrition Assistance Program (SNAP), is at 47.6 million, or nearly one in six Americans.

Illinois and Wyoming registered double-digit year-over-year jumps in use, while Alaska, Arizona, Idaho, Maine, Michigan, Missouri, New Hampshire, North Dakota, Oregon, Pennsylvania, Utah and Washington state all posted annual drops.

Mississippi was the state with the largest share of its population relying on food stamps — 22% — though Washington, DC was a bit higher overall at 23%. One in five residents in Oregon, New Mexico, Louisiana, Tennessee, Georgia and Kentucky also were food-stamp recipients. Wyoming had the smallest share of its population on food stamps — 7%.

No comments:

Post a Comment