http://srsroccoreport.com/is-jp-morgan-getting-nervous-about-its-silver-inventories/is-jp-morgan-getting-nervous-about-its-silver-inventories/

Submitted by Tyler Durden on 07/26/2013 15:18 -0400

Submitted by Tyler Durden on 07/26/2013 15:18 -0400

Is JP Morgan Getting Nervous about its Silver Inventories?

Something interesting has been going on in the Comex silver warehouse inventories this week. Not only have large amounts of silver been removed from the Comex since Monday, but there also have been some large transfers that seem quite peculiar.

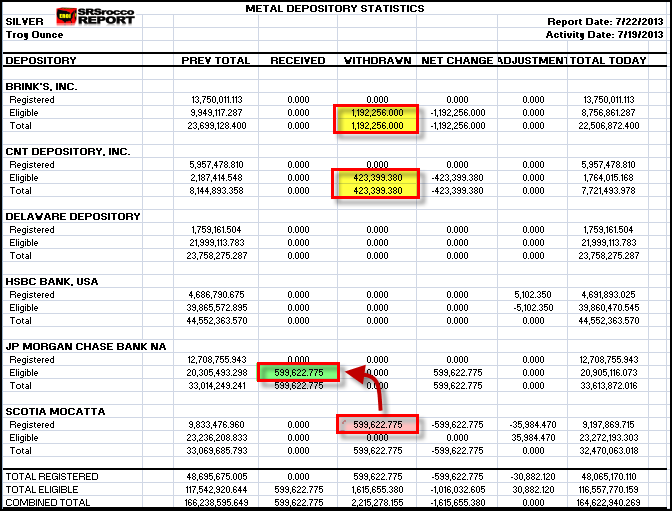

In the beginning of the week, there was a large 2.2 million oz withdrawal of silver from the Comex. However, part of this amount was transferred to JP Morgan:

Here we can see that Scotia Mocatta transferred nearly 600,000 oz of silver from its Registered inventory to JP Morgan’s Eligible. Basically, the registered category is silver that is available for delivery and is also labeled as the dealer inventory. The eligible category is silver owned by an individual or party that is not available for delivery and is known as the customer inventory.

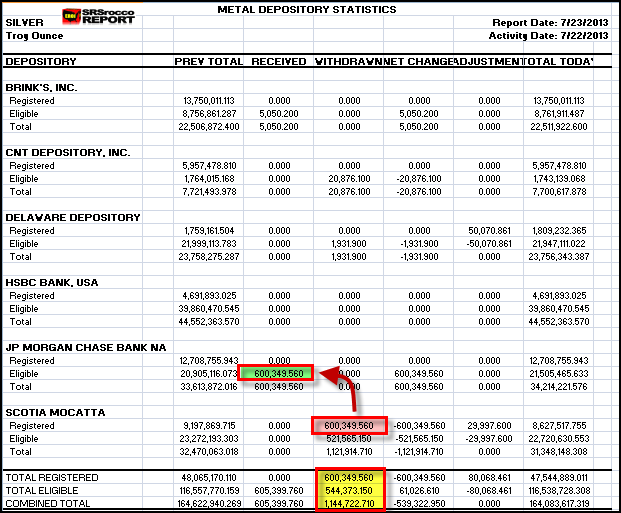

Now, on Tuesday we had another large withdrawal of silver from the Comex but the majority of it came from Scotia Mocatta’s warehouse. And again, if we look at the spreadsheet below, we can see another large transfer of silver from Scotia’s registered inventory to JP Morgan’s eligible:

So, we had 600,000 oz transferred on Monday and another 600,350 oz on Wednesday for a total of 1.2+ million oz in just two days. I find this quite interesting because JP Morgan has a substantial amount of silver in its eligible inventories of over 20 million oz.

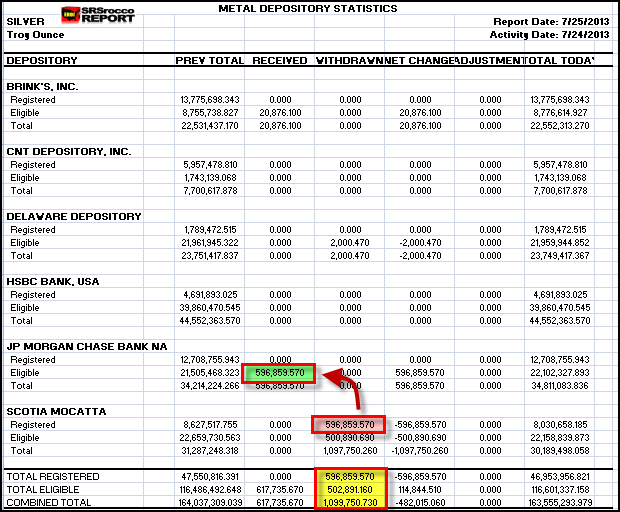

Then on Thursday, there was another large transfer of silver from Scotia to JP Morgan:

In three days, Scotia Mocatta transferred 1.8 million oz of silver from its registered inventories to JP Morgan’s eligible inventories. Furthermore, a total of 2.7 million oz of silver were withdrawn from the Comex (net of transfers) and Scotia Mocatta saw its registered silver inventories decline nearly 20%.

The real question is… what’s going on here. Could this be just a typical transfer of metal from one bank to another? Or could it be that an individual or party has transferred their silver from Canada to the U.S.? Those are all probable answers.

However, we really don’t know what is going on here as everything in the Banking Industry is a big secret. All we can do is speculate. I wrote Harvey Organ and asked him what he thought of these transfers. He replied be saying it could be that JP Morgan is building physical supplies to hand in against delivery notices.

While the more professional traders and Wall Street analysts would blow off these silver transfers as part of doing a honest days business… there really isn’t much honesty left in the banking community. For example, we just learned of new govt. probe into Goldman and JP Morgan’s warehouse industry via ZeroHedge:

Goldman And JP Morgan Probed Over Metals Warehouse Manipulations

Following our initial uncovering of the manipulation and monopolization of the metals warehousing business two years ago, the last few days have seen the public’s attention grabbed by the reality of what the banks are actually doing. Following this week’s hearing, as the Fed reconsiders banks roles in non-banking businesses (and the ‘societal benefit’), it seems the CFTC has woken up. As the WSJ reports, the Department of Justice has opened an initial probe into the metals warehousing industry and the Commodity Futures Trading Commission has also sent letters to some firms telling them to preserve documents, in what is likely the beginning stages of an investigation.

With this and all the other conspiracies and frauds taking place such as the LIBOR scandal and etc, I actually believe something is AMISS and there is probably something STRANGE taking place in JP Morgan’s silver warehouse. I wish I could shed more light, but at least I can reveal what is taking place and we will have to see how this unfolds in the future.

http://www.zerohedge.com/news/2013-07-26/jpmorgan-exit-physical-commodity-business

JPMorgan To Exit Physical Commodity Business

After weeks of emptying of their Gold vaults and making headlines in recent days over their oligolopolization of commodity warehousing, it seems the threat of a probe has excited Blythe and her colleagues to dump while the dumping is good:

- JP. MORGAN TO EXPLORE STRATEGIC ALTERNATIVES FOR ITS PHYSICAL COMMODITIES BUSINESS

Options include sale, spin-off, or strategic partnership as they re-confirm that they are"fully committed to traditional banking activities," as they look to drop the holdings of commodities assets and the physical trading business. We can only assume that "physical commodities" include the company's extensive inventories of tungsten (as well as the vault housing it), and not so extensive stores of gold and silver. That said, we are confident that the collapse in represented (but not warranted) JPM Comex gold vault holdings to a record low, and this news is completely unrelated.

From JPM:

J.P. Morgan to Explore Strategic Alternatives for its Physical Commodities BusinessNew York, July 26, 2013 - JPMorgan Chase & Co. (NYSE: JPM) announced today that it has concluded an internal review and is pursuing strategic alternatives for its physical commodities business, including its remaining holdings of commodities assets and its physical trading operations.To maximize value, the firm will explore a full range of options over time including, but not limited to: a sale, spin off or strategic partnership of its physical commodities business. During the process, the firm will continue to run its physical commodities business as a going concern and fully support ongoing client activities.J.P. Morgan has built a leading commodities franchise in recent years, achieving a top-ranked revenue position. The business has been consistently named as a top client business in Greenwich Associates' annual client surveys and was recently named Derivatives House of the Year by Energy Risk magazine.Following the internal review, J.P. Morgan has also reaffirmed that it will remain fully committed to its traditional banking activities in the commodity markets, including financial derivatives and the vaulting and trading of precious metals. The firm will continue to make markets, provide liquidity and offer advice to global companies and institutions that have, for years, relied on J.P. Morgan's global risk management expertise.

And then the question: which Fed-backed bank will "buy" JPM's commodity exposure? Or maybe this time Bernanke will cut away the middlemen and make the tunnel between its gold vault and that of JPM across Liberty Street, official ?

JP Morgan exiting physical metals - GATA says they will not exit gold ? What about silver ?

Morgan considers exiting commodities business but will stick with gold

Submitted by cpowell on Fri, 2013-07-26 21:12. Section: Daily Dispatches

JPMorgan Eyes Sale of Commodity Unit

By Gregory Meyer

Financial Times, London

Friday, July 26, 2013

Financial Times, London

Friday, July 26, 2013

NEW YORK -- JPMorgan Chase revealed on Friday that it was considering a sale of its physical commodities business, signalling the potential exit of one of Wall Street's biggest traders of cargoes of oil, coal and industrial metals.

The announcement capped a week of intensifying scrutiny of banks' role in the raw materials supply chain. The Federal Reserve said on July 19 it was reviewing a landmark decision to permit banks to own physical commodities, not only paper derivatives. On Tuesday witnesses at a Senate hearing raised questions about metal warehouses, power plants and tanker vessels owned by banks.

JPMorgan said, "We considered many different factors, including the impact of potential new rules and regulations," in arriving at its decision to pursue strategic alternatives for the commodities business.

The announcement comes only three years after JPMorgan, led by commodities chief Blythe Masters, spent $1.6 billion to plunge into physical commodities with the purchase of the global oil, metals, and coal divisions of RBS Sempra Commodities, a trading house.

A year ago JPMorgan was instrumental in salvaging a troubled oil refinery in Philadelphia by agreeing to finance and supply it with crude.

Higher capital requirements, a looming ban on proprietary trading, and the Fed's review have put the viability of acting as a physical commodities merchant under question. Morgan Stanley, the bank with the largest commodities footprint, has said it will look at options that make sense for the business. Last year it engaged in inconclusive talks to sell a stake to Qatar's sovereign wealth fund.

JPMorgan's physical commodities business includes trading in energy markets such as oil, gas, coal and emissions, and base metals. Its longstanding precious metals vaulting and commodity derivatives businesses are not part of the strategic review.

The Financial Times reported this month that JPMorgan was seeking a buyer for Henry Bath, the metals warehousing unit acquired as part of the Sempra deal.

And Kid Dynamite throws a few sticks of dynamite at Harvey Organ's analysis of what's happening with COMEX......

Precious Metals Charlatans – Freaks of the Industry

- Posted by kid dynamite on July 22nd, 2013 at 11:06 am

- Comments: 41 Comments

warning – this post consists of a ruthless exposition and deconstruction of several precious metals bloggers. If you read this post, you will be unable to avoid the conclusion that these bloggers are charlatans who do not know what they are talking about.

I have a confession to make, dear readers: I lied to you. I told you a mere 4 weeks ago that I was done correcting gross ignorance in the precious metals space for free. Fortunately for you, I have a compulsion – a disorder of some sort: I cannot stand to read gross factual inaccuracies, especially when propagated by those trying to sell you something.

There’s yet another nonsense meme going around the precious metals blogosphere, spread by charlatans who have absolutely no idea what they are talking about. This is not my opinion: I will show you the facts that prove beyond the shadow of a doubt that your favorite metals bloggers simply do not understand the market they are trying to analyze. What’s important is that this will make it very easy for you to understand that you are being misled by charlatans who do not know what they are talking about.

It all starts with Harvey Organ – a Canadian pharmacist who writes a daily “report” about the gold and silver markets where he cuts and pastes information from different publicly available sources. Harvey Organ then puts his own “interpretation” on the information, based on his complete lack of understanding of the mechanics of the market. His recent meme is related to JP Morgan’s COMEX gold inventories with respect to the delivery notices detailed in the COMEX reports. Unfortunately, Harvey doesn’t understand 1) the difference between the warehouse inventories and the delivery reports, 2) the difference between registered and eligible gold and house/customer accounts, or 3) the mechanics of the COMEX delivery process. Let me explain how Harvey (and all the other charlatans who read him) think it works.

On a daily basis, the COMEX publishes a delivery report (in pdf form) and a warehouse report (in spreadsheet form). The delivery report – available for daily, monthly, and year to date – shows which shorts issued delivery notices. Shorts issue delivery notices, and longs “stop” the notices. The report looks like this:

COMEX delivery report

Again – the issued column represents the shorts, and the stopped column is the longs. You’ll notice that to the left of the firm name, there is a “C” or an “H.” This represents “Customer” or “House” accounts. However, House account trades can be related to customer activity also, via swaps and other structured trades. We’ll come back to that in a moment.

The warehouse inventory report shows each depository’s inventory of registered metal and eligible metal. It looks like this:

Depository Report

The COMEX rulebook explains the difference between registered and eligible metal:

“Eligible” shall mean, with respect to any metal, that such metal is acceptable for delivery against the applicable metal futures contract for which a Warrant has not been issued”“Registered” shall mean an Eligible metal for which a Warrant has been issued.“Warrant” shall mean a document of title issued by a Licensed Facility, meeting the requirements of Article 7 of the Uniform Commercial Code (“UCC”), and demonstrating that the referenced quantity of the covered metal , stored in the Licensed Facility referenced thereon, meets the specifications of the applicable metal futures contract”Are you with me so far? OK – now here’s where Harvey Organ just starts making stuff up: he looks at the total delivery notices issued by JP Morgan’s House (H) and Customer (C) accounts, and tries to compare them to the warehouse inventories of eligible and registered metal. This is an apples to oranges comparison which is invalid, and it’s why Harvey gets the wrong conclusion. Harvey thinks that eligible metal is “customer” metal and registered metal is “house” metal. This is false. This is not debatable – it’s wrong. All deliveries are made with warrants for registered metal. Customer (C) deliveries are not made from eligible metal. However, in the delivery process, the metal need not move. Let me explain: the delivery process consists of the issuer (short) delivering a valid warrant to the stopper (long). That’s it. It doesn’t mean that the short drops metal off at the long’s door. It means that short gives the long a warrant which is valid title to the underlying contract metal.Now, after the long takes delivery, the long can do whatever he wants to with the warrant. He may 1) detach the warrant (converting the metal from registered to eligible), he may 2) take the metal out, bring it home, and bury it in his backyard, or he may 3) simply hold it as is and sell his warrant next month. What will we see in the depository inventory spreadsheet in each of those scenarios? 1) registered metal decreases while eligible metal increases. 2) registered metal decreases. 3) no change in either category.If you want to read an example of Harvey’s misunderstanding in his own words, you can read this old post of his (which happens to be a good one, since a commenter – Fred – on Harvey’s own post explained the reality of the process to Harvey yet again, and Harvey refused to acknowledge reality). Or, if you like, you can read Harvey’s blog for any day since that June 3rd post I just linked to. He repeats the same bad analysis *daily*.So what happened is Harvey Organ made up his own reality and came up with false conclusions. That’s nothing new in precious metals-land: it happens all the time. But what’s great about this nonsensical fantasy is that it exposes many *other* metals prognosticators who clearly do not understand what they are talking about. We know that they don’t understand what they’re talking about because they regurgitate Harvey’s falsehoods without correcting them.This post arose because I, as a result of my “inability to withstand gross ignorance” compulsion, tried to explain the situation to Bill Holter of Miles Franklin, who sells precious metals for a living. Since the guy sells precious metals for a living, one might expect him not to spout falsehoods in an effort to further those sales, which is why I explained it to him. One would, of course, be mistaken. Our conversation, in the comments of Holter’s own blog with moderated comments, went like this:“P.S. I will give it one more day to see if JP Morgan delivers from both their dealer inventory and from the customer side. They are contracted to deliver roughly 100,000 ounces more gold IN JUNE than they had in their inventories as of Friday afternoon. As I see it, they need to completely empty their inventory AND deliver another 100,000 ounces to honor contracts. It is still not even clear that delivery was made on the 1,000 call options from May. This is a very big deal if you believe in contract law, if not…oh well, there’s always Dancing with the Stars or the America’s Got Talent to watch.”I commented:“Mr. Holter –the postscript of this post makes it quite clear that you have absolutely no understanding of how the COMEX delivery process works. I would suggest that you seek out sources other than Harvey Organ to explain it to you.If you don’t wish to seek out the facts/reality, I beg you to stop misinforming your readers with charlatan nonsense.warmest regards,

KD”Holter replied with simple regurgitations of Harvey Organ’s inaccuracies, in typical metals-charlatan fashion:“vault inventory has moved very little in the last month, nothing has entered the dealer side and 217,000 ounces exited the customer side. They have issued almost 6,000 contracts or about 600,000 ounces of Gold for June delivery…where is it? Did it move? Was it delivered? How was it accounted for? Did “settle” in cash…that would be illegal. Or did it settle in GLD shares?”I explained it politely:“Bill –there is no “Dealer” side or “customer” side. Again – if you “learn” about the COMEX from Harvey Organ, everything you know will be inaccurate.there is “registered” metal and “eligible” metal.and there is no reason why the numbers in the COMEX warehouse inventory spreadsheet need to change when deliveries are made – that is NOT what COMEX deliveries mean. Several people have tried to explain this to Harvey Organ in the past. This is my first and last effort to try to explain it to you. You can re-quote nonsense from Harvey all you want – it will not get any less false.so to answer your questions:the 6000 delivery notices issued from June: yes, they were settled. what happens is that the warehouse receipt is given (From the short, the “issuer”) to the new owner (the long – the “stopper”). No metal moves in this transaction. It’s like a coat check – the claim tag has been given from one party to another. IF and only if the new owner decides to move or reclassify the metal, you will see the warehouse inventories change.No, it did not “Settle in cash” or “in GLD shares”.I suggest you familiarize yourself with what an EFP (Exchange for Physical) is, and with the concept that JP Morgan and their customers can hold metal at other COMEX vaults (don’t forget: JPM’s vault didn’t even exist until a few years ago, yet they still traded on the COMEX before then, right?). Then you’ll understand how these delivery notices are issued month after month.”Holter, like most charlatans, simply wanted to perpetuate his fantasy, and tried to change the subject to other memes:“of course it is registered and eligible but easier for people to understand “dealer and customer”. Yes I understand that receipts are issued, however those receipts are presented and metal either has to move between custodians, be adjusted between the eligible and registered sides or withdrawn. We have not seen anywhere near this for June. GLD and SLV shares have in the past been used in “settlement” and are now “allowed”. I did see your response to Dave Kranzler regarding the audit process of GLD…you forgot to mention the sub custodians …sub sub sub custodians and how JP Morgan cannot be held responsible. Also the CME now has a disclaimer on their website regarding inventory numbers and how they cannot be held responsible, gives you a warm and kinda fuzzy feeling”I explained it again, including a link to a previous post I’ve written debunking other charlatan memes:“Bill –when you start with a false thesis, you arrive at false conclusions. In this case, your false thesis is:“however those receipts are presented and metal either has to move between custodians, be adjusted between the eligible and registered sides or withdrawn. ”no. false. that’s factually incorrect. that is simply not how it works. it’s not something we can debate – your understanding of the COMEX process is flawed, which is understandable, because you learned it from Harvey Organ. You ignored the coat check analogy, which should help you understand. If I deliver COMEX warehouse receipts to you, there is no change in registered metal, eligible metal, or total metal. The warehouse receipts are just in different hands now (yours, instead of mine).and yes, it’s “easier” for people to say “dealer and customer” but it’s wrong, and it leads to people who don’t understand the process, like Harvey, and then you, and then all of your readers.and no, GLD shares cannot be used to settle COMEX contracts. that’s false. I’ve already debunked that nonsense:Bill Holter replied again with another misconception, which I again politely corrected, but he refused to publish my final comment. I would have hoped that Holter had understood my very simple explanations, but he continues to spout this nonsense in subsequent posts:“Unless someone can show me where JP Morgan has concluded their May deliveries or delivered anything at all on their June deliveries I will assume that I have read their reports correctly and are in serious arrears. Please, send me data that illustrates the movement of gold from JP Morgan to those contractually entitled to receive it.”Charlatan, folks – CHARLATAN.Charlatan definitionThe question is: is Bill Holter misinforming you out of ignorance? or out of malice? And which is worse? I’ll leave that to you to debate… let’s move on, since Holter is not the only one exposing himself by re-quoting Harvey Organ’s ignorance.Let’s look at who else clearly doesn’t understand what they are talking about:Turd Ferguson – in a post today – demonstrates that he doesn’t understand the process, but rather is a Harvey Organ regurgitator.Jim Willie – via Turd Ferguson’s comments – is in the same boat.Russ Winter – does not understand the COMEX markets – note that Russ also refused to acknowledge reality when a commenter (Kohala Kid, who is not me) tried to explain it to him clearly.Even your favorite – Zerohedge – alludes to this false meme: “For over a month, JPMorgan managed to mysteriously avoid matching up the gold held in its (world’s largest) vault with the Comex delivery notice update.” (KD: no – no they have not…)Of course, we already know that Jesse of Jesse’s Cafe is a charlatan, as is Dave In Denver. There are a plethora of others – this post is giving you the tools to recognize nonsense when you see it. ANYONE who is repeating Harvey Organ’s false analysis and conclusions lacks an understanding of the COMEX metals markets.I’m sure that someone will falsely accuse me of ad-hominem attacks on these poor misinformed bloggers. Nothing could be further from the truth: these bloggers are DEMONSTRATING (and I am explaining…) a gross lack of understanding of the markets they are purporting to be able to explain to you. This is a gift to you, dear reader, as you can clearly see that they do not know what they are talking about. Again, theSophie’s Choice lose-lose question you have to ask yourself is:Are they misinforming their readers out of ignorance? Or out of malice?And oh by the way – despite the fact that the analysis of JP Morgan’s vault inventories with respect to delivery receipts is blatantly inaccurate, JP Morgan’s gold inventories at the COMEX are indeed decreasing. Is this a sign of impending doom for the bullion banks? I will point out a few *facts* for you:1) JP Morgan’s depository accounts for only 6 percent of the COMEX stocks.2) JP Morgan opened their COMEX depository a few years ago (in 2010 I think)… Do you think that they didn’t trade gold on the COMEX before they had their own depository? Do you think that only firms with their own depository can trade gold?Perhaps JP Morgan is winding down their vault/warehousing business? Perhaps related to this recent story?This post would be incomplete if I didn’t explain the title. I was listening to the Digital Underground classic “Freaks of the Industry” this weekend, and a line resonated with me:“Now if there’s a cure for this, We don’t want it, we’ll run from it.”The precious metals charlatans, as evidenced by the comment thread discussions I pointed to above on their own posts (mine with Holter, Fred’s with Harvey Organ, and KohalaKid’s with Russ Winter) don’t WANT to know the truth – they just want to spread a story like financial herpes… There’s a cure for their gross ignorance, but they don’t want it – they run from it.and so it goes…In closing, I’d like to quote myself:“I will simply repeat this fact: when your theses are based in false foundations, you can only be “correct” out of dumb luck. One shouldn’t be surprised when the predictions made by charlatans who rely on nonsense themselves turn out to be nonsense.”