Commentary on the economic , geopolitical and simply fascinating things going on. Served occasionally with a side of snark.

Monday, May 20, 2013

Global equities continue to be meaningless barometers as credit markets struggle to remain meaningful - despite ham handed Central Bank manipulations.... silver liquidation , a rumor of a silver liquidation , rumors of questionable PM trading in Barrons - PM struggle to be meaningful despite ongoing manipulations.....

Submitted by Mark Grant, author of Out of the Box,

One of the primary focuses of "Out of the Box" is on where you might get hurt and, more importantly, seriously hurt. "Preservation of Capital," the first ten rules of my thinking, has reached epic seriousness in a world with interest rates at unsustainable lows and underlying economic fundamentals that cannot support today's yields. The irrational game goes on based upon one thing and one thing only which is the creation of capital by all of the world's central banks. The money must go somewhere and so it does but the disconnect between the equity markets and bond yields from the real world is frightening.

"Begot of nothing but vain fantasy."

-William Shakespeare

Nowhere on the planet is it scarier than in Europe. Made-up numbers, un-counted liabilities, four years of inaccurate projections from the ECB and the IMF and securitizations parked at the European Central Bank that have all of the credit worthiness of an empanada restaurant in Lisbon. Money flows in, yields go down, the amount of debt increases and few pay any attention to the entire equation which states that what must be paid is the interest rate times the amount of debt as the Draghi bravado overcomes everything. Scant mention these days of the total amount of debt accumulated by the sovereigns as the 3.00% debt limit has become the most elastic of road signs or a trivialized fairy tale by many accounts.

With the banking system in Europe now posting non-performing loans that have reached all-time highs while the recession on the Continent deeps and worsens with the passing of each week I have cast a weathered eye at Europe.Most of us are aware of the dangers in Greece, Cyprus, Portugal and Spain but a careful analysis reveals that these are not the most dangerous of countries. They have problems, they are in dire straits but they do not hold the title of the greatest risk in Europe.

That title, in my opinion, belongs to France.

The Germans ballyhoo and point fingers at Cyprus, Luxembourg, Malta and the like as being financial centers where the banks are much larger than the economy. Yet nowhere in Europe is this issue so pointed as in France.The French banking system is 400% bigger than the economy of France and this is the worst ratio in all of Europe. Please compare this to the American situation where our banks are roughly equivalent (100%) with our economy.

The combined tax rates for wealthier people is not the 75% number that we have seen bandied around but more than 100% for the richest of France. Even the Supreme Court of France has declared this not taxation but confiscation. Mr. Hollande does not want any more austerity but wants to increase social programs, add more sovereign debt, raise their equivalent of social security payments and lower the retirement age. Whatever political niceties that have been bandied about it is clear that Germany and France are in diametric opposition.

Then as France slips further into recession and as their non-performing loans increase and as their massive amount of securitizations rapidly decline in value; their banking system will come under extreme pressure. Much is hidden and cloaked in France but bills that must be paid will begin to take their toll and the uncounted liabilities do not disappear just because no one adds them up correctly. France, in my view, is a powder keg waiting for some fuse to be lit and it will not be a Belle Epoch Ball at Versailles when it does. There will be fireworks aplenty but no cheering crowd to accompany them.

If there is any good news here it may be thatChateau Petrus may once again be affordable.

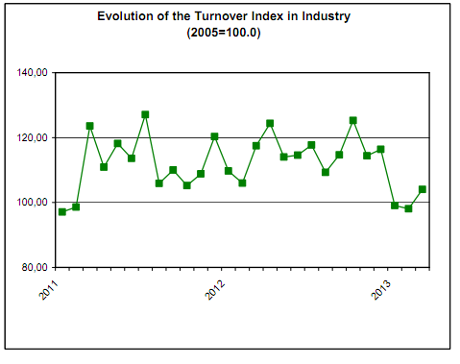

Reeling from its long recession, Greek industry suffered a 12.7% slump in new orders in March, compared with a year ago.

Data just released by the Hellenic Statistical Authority showed that orders for electrical equipment are down by 27% year-on-year.

And capital goods orders, for substantial pieces of machinery and factory equipment, suffered a dramatic 30% decline. (more details here).

With Italy also reporting a big drop in new orders (see 9.12am), the picture in the eurozone's weaker countries is a sharp contract with the upbeat stock markets.

The Hellenic Statistical Authority also reported that turnover across Greek industrial firms was down by 11.5%, year-on-year, in March.

It's a slight improvement on February, as this graph shows:

Hellenic Statistics Authority

This morning's Italian industrial data shows that the domestic market it particularly weak. New orders from within Italy slumped by 13.2% year-on-year in March, while overseas orders were down by 6.1%.

A quiet day unfolding with just Chicago Fed permadove on the wires today at 1pm, following some early pre-Japan market fireworks in the USDJPY and the silver complex, where a cascade of USDJPY margin calls, sent silver to its lowest in years as someone got carted out feet first following a forced liquidation. This however did not stop the Friday ramp higher in the USDJPY from sending the Nikkei225, in a delayed response, to a level surpassing the Dow Jones Industrial Average for the first time in years. Quiet, however, may be just how the traders at 72 Cummings Point Road like it just in case they can hear the paddy wagons approach, following news that things between the government and SAC Capital are turning from bad to worse and that Stevie Cohen, responsible for up to 10-15% of daily NYSE volume, may be testifying before a grand jury soon. The news itself sent S&P futures briefly lower when it hit last night, showing just how influential the CT hedge fund is for overall market liquidity in a world in which the bulk of market "volume" is algos collecting liquidity rebates and churning liquid stocks back and forth to one another.

In other news, we have a $1.25 - $1.75 billion POMO ending at the usual time of 11 am, which may not be sufficient for the usual 0.1x-0.15x daily S&P500 multiple expansion.

Geopolitical tensions in Syria are getting increasingly more acute, even as North Korea continues to pummel the Eastern Sea, having now fired six missiles in the past three days, in a desperate show of "force." The sea has yet to retaliate.

Key overnight bulletin highlights via Bloomberg:

Treasuries steady, yields holding near highest since March amid Fed tapering speculation; JPY gains vs. USD as Japan’s Economy Minister Amari said a further slide in the yen would have negative effects after its 21% drop over the last six months.

Japan 30Y yields surged after a Cabinet Office official told reporters that BoJ’s Kuroda said it’s natural for yields to increase gradually as the economic outlook improves

Bernanke said in a speech that technological change will remake fields like health care and belie predictions that innovation will fade and economic growth will wane; testifies before Congress on Wednesday

China’s new-home prices rose last month in 68 of 70 cities tracked by the government, indicating Premier Li Keqiang will need to maintain efforts to cool the property market even as economic growth slows

Hedge-fund managers are making the biggest ever bet against gold as Soros sold holdings last quarter and Goldman predicted more declines after the longest slump in four years

EU leaders struggling to find a consensus on how to overcome the debt crisis and revive economic growth will use a summit meeting this week to focus on fighting tax evasion and on the bloc’s energy policy

North Korea fired its sixth missile in three days, demonstrating its military capabilities in defiance of global sanctions and diplomatic efforts to convince the totalitarian state to return to talks

BofAML Corporate Master Index OAS at 142bp, tight for the year, as $44.3b priced last week. Markit IG narrows to 70bps, YTD low 69bps. High Yield Master II OAS at 437bps; $15.27b priced last week. CDX High Yield at 107.13, near record 107.37

Sovereign yields mostly higher. Asian stocks gain, with Nikkei +1.5%, Shanghai Composite +0.8%. European stocks mostly higher, U.S. stock-index futures fall. WTI crude, copper, gold fall

Some comments on Amari's most recent jawboning of the Yen over the weekend: the same jawboning he said previously said would not be appropriate.

A slow start to the week has been animated in Asia by Japanese economy minister Amari comments that JPY strength has largely corrected and that further weakness could be harmful. This briefly knocked JPY crosses back but should not put a permanent dent in bearish JPY sentiment. BoJ governor Kuroda made a separate intervention, referring to the volatility in JGBs by stating that it is only natural for long-term yields to rise as inflation expectations pick-up. He does not expect the long-term yield rise to be sustained and if that's the case, then Amari's statement may prove futile as Japanese investors continue their search for higher returns overseas.

A quiet day for Europe with most markets closed for Whit Monday (only Italy new orders and current account data, French bill sale scheduled) means light positions are likely to be observed. We get a first look at the EU PMIs for May on Thursday and the German IFO is due on Friday, but the big day is Wednesday when Fed chairman Bernanke will testify on the economy and the FOMC minutes may offer further insight on the ongoing ‘stimulus exit' discussions, captured by comments from various voters and non-voters in recent days and weeks. The USD has enjoyed its best start to a calendar year in 2013 since 2005 on speculation that Fed monetary policy is slowly nearing a turning point this year, and further clues that the Fed is planning ahead (even without committing to a timetable as unemployment remains too high, inflation low) would probably convince the market to add to long USD positions and push yields and swaps higher in the process. Commodities have been hit hard as the Fed debate hots up (though Asia/China curbing overcapacity should be apportioned some blame too) and US/EU 10y swaps have widened markedly and are now on the verge of breaking though the 50bp barrier for the first time since April 2010. Our colleagues from Economics preview Bernanke's testimony and the FOMC minutes in the note ‘Never too early to plan'.

DB's Jim Reid recaps the relatively quiet day today

Bernanke’s congressional testimony before the Joint Economic Committee this Wednesday will be the highlight in a week where we may learn more about the Fed’s intentions with regards to potential QE tapering. Indeed, Bernanke’s speech will be made on the same day as the Fed publishes minutes from its Apr30th/May1st policy meeting which may shed some further light on the FOMC’s deliberations with respect to asset purchases. In advance of Wednesday, Chicago Fed president Evans will be speaking today, followed by the NY Fed’s Dudley and St Louis Fed’s Bullard who will speak on Tuesday - all are voting members of the FOMC this year.

Outside of the Fed, there’s also a fair bit going on at other central banks. Wednesday will see the Bank of Japan publish its latest monthly policy statement, following the conclusion of its two-day policy meeting which starts on Tuesday. The BoE will be publishing minutes from its last meeting on Wednesday. On Thursday, Draghi will be speaking at an event in the City of London on the topic of "The future of Europe in the global economy" at an event organised by the Lord Mayor. Rounding out the week ahead in policy, the European Council meets on Wednesday where tax policy and initiatives to promote growth are on the official agenda.

In terms of the data flow, Thursday's global flash PMIs for the Euroarea, US and China will be taking centre stage. The market is broadly looking for a 0.2pt to 0.4pt improvement in the manufacturing and service PMIs across the Euroarea, as well as the individual German and French readings. In China, economic forecasters are expecting the country’s flash manufacturing PMI to be unchanged at 50.4. In the US, the main data releases this week are existing home sales (Wednesday), new home sales and jobless claims (Thursday) and durable goods (Friday). The UK’s retail sales/Q1 GDP revisions and Euroarea consumer confidence numbers are out on Thursday. The German IFO survey is scheduled for Friday.

Returning to markets, precious metals have been making headlines overnight after spot silver prices dropped by as much as 9% at one stage in early Asian trading. Silver prices have since recovered to trade 4% lower on the day as we type. Gold (-1%) has also recovered after being down 2% at one stage in sympathy with the drop in silver prices. There has been chatter suggesting that the outsized move was driven by a margin call and subsequent liquidation by an investor. Notably, gold is poised to close weaker for the tenth time in 11 sessions, and is now trading at similar levels as the April lows ($1345/oz).

The Japanese yen is also in focus overnight after trading below 102 at point during the Asian session. The move followed comments from Japan’s economy minister Mr Amari who said over the weekend that the yen’s excessive strength has been largely “corrected” and that further weakness could be harmful in terms of living costs (Nikkei). USDJPY has pared initial losses, but is still 0.5% lower this morning. Elsewhere in Asia, equities have begun the week on a firmer footing, helped by the S&P500’s performance on Friday when it finished near the day’s highs of +1%.

Asian gains are being led by Hang Seng (+1.7%), ASX200 (+0.9%) and the KOSPI (+0.2%). The Nikkei (+1.3%) has broken through the 15300 level for the first time since late 2007, and is trading higher despite the strengthening in the yen. Asian credit markets are about 2-3bp better overnight.

Returning to last Friday, the European subordinated financials credit index’s 14bp tightening (to 200bp) was amongst the interesting market moves. The result capped a three-day streak which saw the index tighten by a cumulative 24bp, outperforming the senior financials index which tightened 9bp in the same period. The sub-senior financials multiple (1.5x) is at its lowest level since Q4 2010. Partially behind the move were recent announcements from ISDA who are considering adding a “bail-in” credit event to financial CDS contracts in response to the EU’s potential bank resolution rules. Other changes include allowing written down bonds to be delivered into a CDS auction based on the outstanding principal balance before the bail-in occurred. Other instruments that bonds may be converted to in the event of bail-ins, such as equities, may be deliverable into a CDS auction under proposals (IFR).

Turning to the day ahead, it will be relatively quiet start to the week with Monday public holidays in parts of Europe. Economic data will be relatively thin today. The Chicago Fed’s Charles Evans will be speaking at 6pm London time.

Submitted by Tyler Durden on 05/20/2013 08:25 -0400

Submitted by Tyler Durden on 05/20/2013 08:25 -0400

No comments:

Post a Comment