Commentary on the economic , geopolitical and simply fascinating things going on. Served occasionally with a side of snark.

Monday, May 13, 2013

Europe Watch - May 13 , 2013 ... Germany Finance Minister throws cold water on Single Bank Resolution Agency ....Greek Construction collapses 42 percent year over year.....Italian debt auction news .....ECB says negative interest rates would be effective ( but for whom ) ....German Fin Min says Slovenia must accept tough austerity to avoid Troika tough austerity debt hell ....Spain holds big protest rally and Cyprus warns Europe must learn from its Cyprus mistakes.... Greece and Spain to get their welfare payments.....

Germany's Finance minister, Wolfgang Schäuble, has an uncanny ability to tread a very narrow line on formation of an EU banking union. He frequently crosses over the line in both directions but never very far, and never for long.

Every time he gives an inch to solidarity, he quickly takes it back, and vice versa. And here we go again.

Weeks before the European Commission is due to present its plan for a single bank resolution agency and rescue fund, Schäuble threw the plans in doubt with a warning EU bank rescue agency needs treaty changes.

Germany’s finance minister has warned that a single EU bailout agency and rescue fund for ailing banks is legally untenable until the bloc’s treaties have been overhauled.

In today’s Financial Times, Wolfgang Schäuble calls for a “two-step approach” that would leave bank rescues in the hands of “a network of” national authorities until treaty changes can take place.

Mr Schäuble’s declaration comes just weeks before the European Commission is due to present its plan for a single bank resolution agency and rescue fund – widely touted as the second pillar in the eurozone’s much-vaunted “banking union” – throwing the proposal into doubt even before it is unveiled.

“The EU does not have coercive means to enforce decisions. Its historical roots are young. Its democratic legitimacy could be improved upon,” Mr Schäuble writes. “What it has are responsibilities and powers defined by its treaties. To take them lightly, as is sometimes suggested, is to tamper with the rule of law.”

Lawyers for the European Commission and the European Central Bank, which has joined Brussels in pushing for quick adoption of a resolution authority after last month’s creation of a common EU bank supervisor in Frankfurt, have argued that existing treaties allow for centralising powers to shut down or restructure weak banks.

But Mr Schäuble writes that the treaties “do not suffice to anchor beyond doubt a new and strong central resolution authority”. He added that promises to create an authority quickly would cost the EU credibility, saying: “We should not make promises we cannot keep.” Even limited changes to EU treaties can take months if not years.

While he acknowledges his “two-step” plan would lead to “a timber-framed, not a steel-framed, banking union”, Mr Schäuble said it would be adequate until treaties were changed. However, the ECB has expressed concern about keeping resolution at a national level after centralising bank supervision, saying it would undermine Frankfurt’s ability to make independent judgments about a bank’s health.

It's crystal clear the banking union proposal is in violation of both the eurozone treaty and the German Constitution, but such things only seem to matter on an on again off again basis. Most likely this is just another election ploy attempting to hoodwink potential AfD party members into thinking CDU/CSU will not let a full-fledged banking union happen without treaty changes.

Given past wishy-washy politics from both Chancellor Angela Merkel and Schäuble, I would not trust this stance one bit if I was a potential AfD voter.

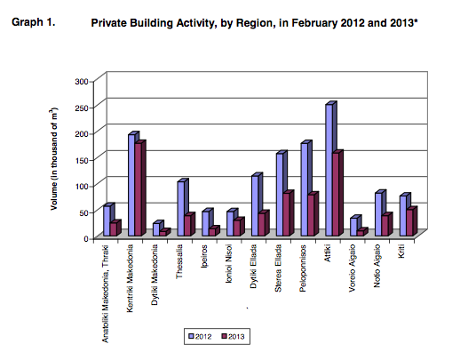

Construction activity in many Greek regions has shrunk drastically. Photograph: ELSTAT

Dire construction data from Greece this morning. The number of permits issued to build new buildings tumbled by 42.9% year-on-year in February.

Just 1,240 new permits were awarded to builders during the month, down from 2,27 in February 2012. In volume terms, activity has almost halved.

It's another sign of the damage caused to Greece's economy, along with record unemployment and steadily shinking retail sales.

Economist Shaun Richards has written a blogpost today, outlining how the Greek economic crisis has been far worse than the Troika anticipated:

We are left three years after the bailout of Greece with shock and awe at the economic destruction that has been inflicted on Greece. Even the rose-tinted forecasts of the European Commission predict that her economy will shrink by 4.2% this year. Every time we see a number which shows a glimmer of hope we find another like todays truly dreadful construction numbers to shatter it.

Again and again we are told that reovery is “just around the corner” as we discover that like on a Roman road there are no corners in sight. I think that those responsible for this should be called to account for their actions. But sadly I see a world where one of them -Christine Lagarde- was elevated to the role of Manging Director of the IMF which can only be a sad indictment of these times.

Please remember this when it is presented as a success later that the Greek people will have another 7.5 billion Euros added to their debts by the end of June.

A successful bond auction for Italy. It just raised €8bn, its maximum target, at lower yields than earlier this year.

Not much sign that investors are losing their appetite for peripheral bonds (although demand was down slightly).

Here's the details:

• €3.5bn of 2016 bonds, at a yield of 1.92%, down from 2.29% in April (lowest yield since January 2013)

• €3bn of 2018 bonds, at a yield of 2.44%, down from 3.030%

• €1.5bn of 2026 bonds, at a yields of 4.07%, down from 4.55% in February

ECB negative rates 'would be effective'

The euro has fallen this morning after Italy's central bank governor said the European Central Bank could cut its deposit rate (paid to banks who stash cash with it) into negative territory.

Ignazio Visco, a member of the ECB's governing council, told CNBC that a negative deposit rate would be effective.

The comments come 10 days after Mario Draghi revealed that the ECB was open to the idea of cutting the deposit rate below its current low of 0.0%.

Visco said:

We all agreed in the council that we have to look with care and in that case we may reduce the [deposit] rate....

We think that - and I personally think that, this is effective – the economy now is capable of taking it on board. Technically, we are equipped and ready to intervene. There may be unintended consequences - we know we may have to work on that - and we know how to work on that.

Just to be clear, we're not talking about hitting depositors with negative savings rates (the ECB cut that rate to a record low of 0.5% this month).

Imposing negative interest rates on bank deposits would be a significant development in the history of the eurozone. Visco's 'unintended consequences' include the possibility that banks buy riskier government bonds, rather than leaving money in the central bank to suffer a small loss each night.

Banks could also actually cut liquidity, rather than pushing more credit out into the eurozone economy.

I don’t question the fact that such a move will persuade banks to search for higher-yielding assets, ie loans but what I’m trying to explain is that the liquidity in the banking system is like a hot potato. The central bank controls how much money there is in the system (using various ways, eg printing money, changing the reserve requirement etc) and the market only needs to decide the price of this money.

The only way that lowering rates to the negative territory impacts the amount of cash in the system is because the central bank will be returning 99% of the money placed in it back to banks.

But then which of the major central banks could even contemplate shrinking its balance sheet at the time when the global economy remains exceptionally fragile?

Germany's finance minister declared this morning that Slovenia must swallow 'painful' measures if it is avoid seeking international help.

Wolfgang Schäuble told Germany's SWR radio station that:

Slovenia can manage [without a bailout programme]. However it must also carry out some painful restructuring [of its economy].

Quotes via Reuters.

Last week the Slovenian government announced a package of state asset sales, a restructuring of its ailing banking sector, and a 2% increase in VAT. The European Commission is expected to give its verdict on the plan by the end of May.

Our economics editor, Larry Elliott, writes today that Spain's leaders are pinning their hopes on banking union, and eventually fiscal union too. But the risk of a "crash landing" remains dangerously real, he warns:

That's not just because unemployment in Spain has risen by three and a half million since the start of the crisis and has now reached 27%, or that the domestic economy has shrunk by a sixth. It is that Spain is up to its eyeballs in debt, with no likely improvement in prospect.

Despite austerity, little progress is being made in reducing the budget deficit and national debt is heading for well over 100% of gross domestic product. In the absence of more rapid growth and a banking union being agreed swiftly, a Greek-style debt restructuring seems eminently possible.

Spain is perhaps the emblematic eurozone country. Its past performance reflects the design flaws in the single currency; it is trapped in a low-growth, high-debt vortex; and it can only recover if a reluctant Germany backs plans for integration.

Cyprus: Europe must learn lessons

Cyprus is hoping to patch up relations with the eurozone during today's Eurogroup meeting, its finance minister has said.

Haris Georgiades (appointed in April) told CNBC that he was eager to repair any damage with relations with Brussels, following March's botched bailout that resulted in capital controls being imposed in Cyprus and heavy losses on larger bank customers.

Georgiades also warned that Europe must learn lessons from the Cyprus debacle and rethink its decision-making process.

Video: Los Indignados hold 'silent scream'

Spains' Los Indignados movement held a 'silent scream' in Madrid's Puerta del Sol square yesterday evening, as part of Sunday's protests.

This video clip shows that the famous square was packed, suggesting thousands of people took part:

Sunday's protests marked two years of Los Indignados (the official anniversary is this Wednesday).

“I’m here because, two years later, things are worse. We demanded social rights, and we’re actually losing them,” said one demonstrator.

Another added: “I think everybody who is really concerned about people and not about other interests, should be here. We’re fighting to make everything fairer and to look after ourselves.

Activists of the Mortgage Victims' Platform (PAH) hold placards which read "Stop evictions" during a demonstration in Valencia on Sunday. Photograph: HEINO KALIS/REUTERSDemonstrators gather in the Puerta del Sol on the second anniversary of the 15M movement in central Madrid May 12, 2013. Photograph: PAUL HANNA/REUTERSDemonstrators marching in Malaga on Sunday. Photograph: JON NAZCA/REUTERS

Ministers to decide on Greek and Cyprus aid payments

Good morning, and welcome to our rolling coverage of the eurozone financial crisis, and other key events across the world economy.

Greece and Cyprus will be under the microscope today when Eurozone finance ministers meet to decide whether to extend bailout payments to both countries.

Ministers are expected to give their approval to Cyprus's first aid tranche, worth €3bn, and also to sign off the latest installment of Greece's own package. If that happens, expect to hear soothing words about Europe making progress...

With Spanish unemployment at a blood-chilling 27%, there were fresh protests against the country's government over the weekend.

Spain's Los Indignados protest movement held marches in scores of cities across Spain on Sunday, under the slogan ""From outrage to rebellion" (more on this shortly)

Something for finance ministers to ponder as they head to the Eurogroup....

No comments:

Post a Comment