Commentary on the economic , geopolitical and simply fascinating things going on. Served occasionally with a side of snark.

Tuesday, April 30, 2013

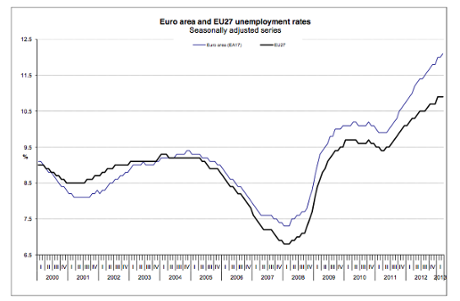

Cyprus Parliament set to vote today on its bailout - slim yes vote anticipated....meanwhile , questions as to why Cyprus continued to buy Greek bonds continue.... Eurozone unemployment data released - new record of 12.1 percent hit ! Spanish recession continues , tough unemployment conditions is spain and Italy continue......

In a little under two minutes, Nigel Farage sums up the utter farce that "the religion" that Europe has become. He explains, his fear is that what will break up the Euro, "is not the economics of it, but wholesale, violent revolution," in the Mediterranean, and that is "all so unnecessary!" Speaking at Simon Black's Offshore Tactics workshop, the so-called modern day Cicero goes on to point out thatFrance's Hollande is "the number 1 among idiots running countries around the world," and worries that Merkel's pending election means there will be more and more 'tough talk and action' as she shows the people she is in charge. Simply put he warns, alongside Ron Paul, that if you have money in European banks,"Get your money out," because, "when the next phase of the disaster comes, they will come for you."

A leaked internal briefing from Angela Merkel's coalition partners refers to President Francois Hollande as "meandering" and draws attention to France's "highly regulated labour market and highly developed social security system".

Details of the briefing note were published alongside an internal assessment from the German economics ministry, which listed the French economy's failings.

The ministry's paper said: "French industry is increasingly losing its competitiveness. The relocation of companies abroad continues. Profitability is meagre."

Relations between France and Germany are chilly after Mr Hollande's Socialist party accused Mrs Merkel of "egotistical intransigence" and called for "democratic confrontation" with Berlin.

The French Socialists' attack on the German chancellor, which was toned down after a draft was leaked to the press, brought accusations from the French centre-right that Mr Hollande's party had been gripped by Germanophobia.

The public response from the German government was muted, with Mrs Merkel's spokesman describing the French denigration of the Chancellor as "background music".

However, the memos – which were leaked to the financial newspaper Handelsblatt – reveal Berlin's harshly critical private view of France's economic woes.

The German economics ministry's briefing draws attention to France's high wage costs.

It points out that France has the "second lowest annual working time" in the European Union, while its "tax and social security burden" is the highest in the eurozone. It also warns that France has made too little investment in research and development.

The briefing by Mrs Merkel's partners, the Free Democrats, which has been circulated within the German government, is likely to cause fresh tension between the European partners by describing Mr Hollande's reform programme as "meandering". The French president's approval ratings have fallen to record lows since he was elected last May.

The divide between the two nations traditionally regarded as the driving force behind European integration was underlined yesterday with new figures showing that French unemployment, at 11 per cent, was double that in Germany. The German jobless rate of 5.4 per cent is the second lowest in Europe.

While France clings to its totemic 35-hour working week, workers in Germany are increasingly discontented at having to endure years of low pay rises.

The Organisation for Economic Cooperation and Development has said it expects the French economy to grow by 0.1 per cent this year, and has criticised "excessive regulation and high levels of taxation". The German economy, meanwhile, is forecast to grow by 0.5 per cent.

German politicians have closed ranks in defence of Mrs Merkel.

Andreas Schockenhoff, foreign affairs spokesman for the Christian Democrat parliamentary party, said: "The attacks by senior French socialists on the Chancellor are unusual for the German-French relationship, and they are inappropriate.

"The Left-wing government cannot divert attention from the fact that France requires deep structural reforms."

While Mr Hollande has kept a low profile since the working paper, several cabinet members have criticised their own Socialist Party for the remarks.

Prime Minister Jean-Marc Ayrault, a former German teacher, tweeted in German calling for calm and said the two countries would not advance "through confrontation and insults but by putting everything on the table – points of convergence but also of divergence".

After a meeting with Mr Hollande on Monday night, Martin Schulz, President of the European Parliament and a member of the Social Democrats, the main German opposition party, said: "Blaming Angela Merkel for all the problems of Europe, I find that unfair. Around the table in Brussels there are 26 other leaders, not just Angela Merkel.

"It is well known that I'm a Social Democrat, so I'm no supporter of Merkel, but she can't be held responsible for everything that goes wrong in Europe."

The French criticisms of Mrs Merkel were made in a working paper prepared ahead of the Socialist Party's convention on Europe in June, which was leaked in the French press last week. The paper's authors claimed that the German chancellor "thinks about nothing except the savings of account holders on the other side of the Rhine, Berlin's trade balance and her electoral future".

Russian shopkeepers, small businesses and middle-class expats are among the victims of the island’s financial meltdown.

Feeling the squeeze: Many in Cyprus took to the streets to protest as banks closed for two weeks and investors took a ‘haircut’ on their savings. Source: Getty Images

Although Russian savers of all descriptions, from private individuals and small businesses to corporations and institutions, have suffered in the Cypriot financial crisis, the effect is seen most starkly among the thousands of Russians actually living on the Mediterranean island. Here, it’s not oligarchs but middle-class entrepreneurs who have been devastated by the crisis, and the EU-imposed “haircut” on deposits of more than $130,000.

“My business is more dead than alive,” says Anton, the 32-year-old owner of a foodstuffs distribution network in Limassol. “I was rash enough to keep all the company’s money in the Bank of Cyprus.”

It’s an all-too-common tale from middle-class Russians living and working in Cyprus, of whom there are 30,000 to 50,000 – mostly businesspeople, executives, and the Russian wives and girlfriends of Cypriot nationals.

A $13 billion bailout was announced last month in return for Cyprus agreeing to close Laiki Bank, the island’s second largest, levying all uninsured deposits there, and possibly around 40 percent of uninsured deposits in the Bank of Cyprus, many held by wealthy citizens of other countries, including many Russians. Insured deposits of $130,000 or less are not affected.

The seizure of deposits has hardly touched Russian oligarchs: Thanks to the intricate structure of holdings registered in Pacific and Caribbean tax havens and ingenious schemes of share distribution, the oligarchs’ money accounted for an insignificant share of deposits held in Cyprus banks. Instead, it’s small and medium-sized businesses that were most often caught out.

Georgy, 52, owner of a Russian goods shop in Limassol, says his business hasn’t been doing well since the last financial crisis in 2008.

"Unjust, unprofessional and dangerous.’’ (Describing the EU’s initial plan to levy a tax on depositors, rejected by the Cypriot parliament)

“The more you squeeze foreign investors in the financial institutions of your countries, the better for us, because the affected, offended and frightened (not all of them, but many) should, as we hope, come to our financial institutions and keep their money in our banks. I am even glad, to some extent, because these events have shown how risky and insecure investments in western financial institutions can be.”

Vladimir Putin, President

“We were thinking of selling our business because it barely paid its way, and we’ve been running at a loss for the last month.”

Like other Russians interviewed, Georgy was reluctant to give his surname, because of suspicions among Russian businesspeople about talking to the media.

“I can’t imagine how I will pay the suppliers, the rent and the bills… we have far fewer customers, and they buy only the bare necessities.”

In this respect, Russians living here have been affected much the same as ordinary Cypriots, and Russian small and medium-size entrepreneurs mostly provide work for Cypriots.

Alexander, 40, managing director of a shipping company, says most of its 80 Cypriot employees – operational staff, logistics specialists and accountants – will probably be fired, or have to take deep pay cuts.

“The company is still operating, our ships continue to carry fertiliser, but the company has no capital left,” says Alexander. “Shock, horror and depression prevail.”

The other emotion, naturally, is anger – that the Cypriot and European authorities could conspire to seize depositors’ money in a way that Russian businesspeople would hardly expect of bankers back home.

“The seizure of deposits is simply expropriation, which I thought only the Bolsheviks were capable of,” says Anton. “To put it simply, this is daylight robbery, gentlemen.”

"Let us talk about what’s happening with Cyprus. The stealing of the stolen is continuing there, I think.” (Reference to a comment by Vladimir Lenin after the 1917 Revolution to condone Bolshevik expropriation of “capitalist” property)

Dmitry Medvedev, Prime Minister

The Cypriot economy has for decades depended on financial services and tourism. Before the Russians came to Cyprus in the 1990s, it was well-heeled expatriates from Beirut, taking refuge from Lebanon’s civil war. And as the Lebanese went home, their place was taken by Russian entrepreneurs seeking a safe haven from the Wild West-style Russian economy of the 1990s, and a more predictable tax regime and business climate.

Since then, Russian business has underpinned the island’s economy, with Russian companies, property owners and tourists becoming indispensable. But now all that is under threat as the island faces up to potentially decades of austerity and economic pain.

Companies providing financial services have been a mainstay, due to the low corporate tax rate and British-style legal system. They are now facing the pinch, as Russian and other investors look for other places to keep their money.

"What is happening is a good signal to those who are ready to return their money, under Russian jurisdiction, into Russian banks. We have very stable banks.”

Igor Shuvalov, First Deputy Prime Minister

Marina, 35, corporate services executive, says that her clients are curtailing their business on Cyprus and moving to other jurisdictions, such as “Dubai and other offshores. We are advising our clients to leave their companies here, but we tell them to keep their money in other countries, preferably outside the EU.”

She adds that her office has been in a state of panic.

“We work late, and often go without lunch breaks,” she says. “Our owner is on the phone day and night, answering calls from clients who ask when they can withdraw their money from local banks. Everyone understands that the first wave of haircuts may be followed by a second one, and so on.”

This view is echoed by Larisa, an accountant at an investment company.

“The possibility of quick direct transactions with Europe and the U.S. was crucial for clients. Cypriot banks are no longer trusted. People will move whatever remains in their deposits to other countries – most probably outside the eurozone, to the Middle East and Asia.”

"I have no doubts about the reasons for the EU’s intention to rob Cypriot depositors. There is a lot of dirty money (mostly Russian) in Cyprus, and European banks want to have this money for themselves. This is not a fight against dirty money, it’s a fight for dirty money.”

Yulia Latynina, Commentator, Novaya Gazeta

She worries that the Cyprus “bail-in”, where depositors’ savings were seized, could become the norm in other European countries.

“Who can guarantee that the next ‘patients’ treated at depositors’ expense will not be the banks of Malta, Luxembourg or Holland?” she says.

“We will [restructure the loan] taking into account our interests, and our interests are that [Russian Commercial Bank, a subsidiary of Russian state-controlled bank VTB] should operate in normal conditions,” Anton Siluanov, Russia’s Finance Minister, said on the sidelines of a G20 meeting of finance officials in Washington.

Experts predict that the Cypriot financial crisis will have long-term consequences on the European Union's economy. Source: Getty Images / Photobank

“It does not require any bailout or financial support. Money of our companies has been frozen there. We would like this money to reach its recipients,” he added.

Not all Russian businesspeople on the island have been affected, as they hold accounts in different locations, but just live in Cyprus.

Vladislav, 47, owner of a pharmaceutical company, says his business is based in Russia.

“I moved my family here because it’s safe and warm, and they are happy here. I kept only a few thousand euros in the Bank of Cyprus.”

But he sees the “heavy blow” the crisis is dealing Cyprus. “The shops and cafés are shutting down one after another,” he says.

Some Russians are on the point of giving up doing business on the island. “I would hate to leave Cyprus, but perhaps there will be no option,” says Alexander.

As for Georgy, he’s thinking of closing. “If the situation doesn’t improve in the next couple of months, we’ll have to abandon the business,” he says. “I’ll have to take any job, just to feed my family.”

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_30/04/2013_496854 ( Cyprus has made its Troikan bed , now they must lie there - no complaining moving forward , Cypriots ! )

Cyprus votes loan agreement through Parliament

Cypriot lawmakers on Tuesday narrowly approved a multi-billion-euro loan agreement with international creditors, with 29 votes in favor and 27 against, following a tense day of debate in Parliament and as hundreds of protesters rallied outside the House with officers forcing back some who sought to break a police cordon.

The vote, which was expected to be close, followed an appeal earlier in the day by President Nicos Anastasiades for MPs to support the loan agreement despite its onerous terms. “What we are being asked to do today is adopt a loan agreement which will allow our country to breathe and give us the chance to overcome whichever problems may arise in this crisis,” he said.

Earlier in the day, government spokesman Christos Stylianides had struck a similar tone in comments to state radio. “We have had enough of delusions. We don't have any other choice,» he said. Whoever knows of one should tell us what it is.”

The first tranche of rescue funding – a 2-billion-euro instalment – is to be disbursed in mid-May with the second instalment of 1 billion euros to be paid out at the end of June. Of the 10 billion euros being lent to Nicosia, 2.5 billion euros is for bank recapitalization, 4.1 billion euros is for paying off debts and 3.4 billion euros for covering fiscal needs.

As part of its deal with the so-called troika of foreign creditors – the European Commission, European Central Bank and International Monetary Fund -- Nicosia committed to closing its second-largest lender, Cyprus Popular Bank (Laiki) and imposing heavy losses on uninsured depositors in Bank of Cyprus.

The main opposition party, Communist AKEL, which had initially applied for financial support in June 2012 when it was in power, suggested in a statement issued yesterday that the terms of the final deal were so painful that leaving the euro zone might be a preferable option. «Cyprus's only option is a solution outside the loan agreement and the Memorandum of Understanding,” it said. “Seeking such a solution is possibly tantamount to a decision to exit the euro.”

http://ransquawk.com/headlines/290296

Cyprus parliament are scheduled to vote on the Cypriot bailout this evening after discussions this morning, although no time has been indicated

Update details:

- Cyprus mail note that approval is likely although it is from a thin majority and against mounting calls for the island to exit the euro. - Lawmakers were meeting in an extraordinary session to ratify the terms of the aid, which is conditional on Cyprus winding down its second-largest bank and imposing heavy losses on uninsured depositors in another.

Cyprus parliament decides on bailout, likely to vote yes

By Michele Kambas

Cyprus's parliament decides on Tuesday whether to back a bailout imposed by its EU partners, with approval likely from a thin majority against mounting calls for the island to exit the euro.

Lawmakers were due to meet in an extraordinary session to ratify the terms of the aid, which is conditional on Cyprus winding down its second-largest bank and imposing heavy losses on uninsured depositors in another. Voting was expected on Tuesday afternoon.

No single party has a majority in the 56-member parliament, and the government is counting on support from members of its three-party centre-right coalition which has 30 seats in total. It needs 29 votes for the bill to pass.

Cyprus, the eurozone's third smallest country, is bracing itself for at least two years of economic misery and record unemployment as terms of the 10 billion euro bailout deal start to bite.

Shut out of financial markets for two years, Cyprus will fall into chaotic default if lawmakers vote down the bill, government officials have warned.

"We have had enough of delusions. We don't have another choice. Whoever has one should tell us what it is,» Cypriot government spokesman Christos Stylianides told state radio.

Communist AKEL, in government until it lost presidential elections in February, said it planned to vote against the bill. It has 19 seats in parliament. The socialist Edek party, with 5 seats, also said it would reject it.

Attempts to agree on a bailout triggered financial chaos on the island last month, when parliament rejected an initial plan to force both insured and uninsured depositors to pay a levy to fund the recapitalisation of two banks heavily exposed to debt-crippled Greece. Insured deposits are those of up to 100,000 euros.

It was followed by a two-week shutdown of banks. The fallback option was to wind down one of the banks, Laiki, and impose losses of up to 60 percent on uninsured deposits in a second, Bank of Cyprus.

AKEL, which had made the initial application for financial aid in June 2012, said onerous terms offered by Cyprus's EU partners were compelling enough for the island to seek alternative sources of funding.

"Cyprus's only option is a solution outside the loan agreement and the Memorandum of Understanding. Seeking such a solution is possibly tantamount to a decision to exit the euro,» it said in a statement.

By Michele Kambas, Stephen Grey and Stelios Orphanides

One day last October, a memory stick containing special software for deleting data was placed into a desktop computer at Bank of Cyprus.

Within minutes, 28,000 files were erased, according to investigators who had wanted to copy the data for an official report into the collapse of the Cypriot banking system.

The deleted files included emails sent and received in a crucial period in late 2009 and early 2010 when Bank of Cyprus, the biggest lender on the island, spent billions of euros buying Greek bonds - at a time when international banks were cutting exposure to the heavily indebted Athens government.

Those Greek bonds lost most of their value in last year's EU-sanctioned bailout, playing a key role in plunging Cyprus into an economic maelstrom. When banks turned to Cyprus's own cash-strapped government for help in plugging holes in their balance sheets, Nicosia too needed an international rescue.

Now people in the small euro zone republic, who have lost money and face years of grim austerity, want to know who decided to plough their savings into the doomed public accounts of their bigger neighbor, and why. But answers are proving elusive, not helped by the mysterious wiping of data at Bank of Cyprus.

There has been public speculation about backroom diplomatic deals or misplaced solidarity with Cypriots' fellow Greek-speakers.

But executives at the failed banks argue that Greek bonds seemed a good investment at the time - though that view is at odds with that of many bankers elsewhere in Europe, who were doing all they could to limit their own exposures to Greece.

The confidential report, prepared for the Cypriot central bank by global consultants Alvarez and Marsal, found that Bank of Cyprus had been willing, from 2009 onwards, to invest in risky, high-yielding Greek debt in a bid to offset an erosion of its balance sheet from rising non-performing loans.

The report, which Reuters has seen, alleges that bank executives may not have revealed details of bond purchases to board directors, avoided showing losses on the bonds, and may later have delayed external investigation of the bond purchases.

In December 2009, managers told media and their own board that most of the bank's Greek bondholdings had been sold - but the bank did not then disclose that it had almost immediately bought more.

Bank of Cyprus has declined to comment on the report. Petros Clerides, the Cypriot attorney-general to whom a copy of the report was delivered, declined any comment on the matter.

Much attention in the crisis has hitherto focused on allegations of poor management at Cyprus's other big lender, Laiki Bank, formerly Marfin Popular. But the Alvarez and Marsal report, whose broad findings emerged earlier this month, raises questions, too, about the former management of Bank of Cyprus.

The report noted «a culture whereby senior management decisions were not challenged».

Michael Olympios, who heads an investors' association, Pasexa, that has complained of mismanagement, said: «There was clear corporate governance failure here, and a lack of disclosure to shareholders."

More broadly, he added: «If one wants to summaries the mess in our banking system, Lord Acton sums it up; power tends to corrupt, and absolute power corrupts absolutely."

Under last month's bailout deal for the Cypriot state, Laiki is being closed and Bank of Cyprus is being recapitalized. Large depositors at Bank of Cyprus have seen virtually all of their deposits over an insured 100,000-euro ($131,000) threshold frozen and stand to see up to 60 percent of those converted into equity.

Many in Cyprus, including hundreds of Russians who placed their faith in its once booming offshore banking products, feel they have been unfairly treated; bank depositors in Greece suffered no losses when that country was bailed out.

"They should have bought from different governments rather than just Greece,» said Demetris Syllouris, who heads the Cyprus parliament's ethics committee which is looking into the affair.

"This caused 80 percent of the problem we are in."

Aside from the wisdom of its investment strategy, it is the communication of this strategy to investors that is in question.

On December 10, 2009, Yiannis Kypri, a general manager at Bank of Cyprus, told a Cypriot website, Stockwatch, that the bank had «minimal exposure to Greek sovereign debt» after reducing its holdings from 1.8 billion euros to 0.1 billion.

The same day, according to the investigators' report, Andreas Eliades, then Bank of Cyprus's group chief executive officer, instructed his treasury department to begin new purchases of such bonds. With these new instructions, that day the bank bought debt worth 150 million euros, and a total of 400 million by the end of 2009, according to the consultants.

There is, the report says, «no evidence» the public comment about «minimal exposure» to Greece was ever «retracted or subsequently corrected by any of the bank's executives».

Kypri told Reuters he could say little while an official inquiry continues, but he was quoted by the investigators saying he had been unaware of the plan to return to buying Greek bonds.

Andreas Eliades, who was chief executive until July 2012, told Reuters Kypri's statement to Stockwatch referred only to a temporary sell-off in response to short-term market fluctuation.

Another member of senior management at the time, Nicolas Karydas, gave investigators and Reuters the same explanation.

On December 11, the day after the bank resumed purchases of Greek bonds, Karydas told the bank's board that most of its Greek bonds had been sold. But, the Alvarez and Marsal investigators, add: «The board was not informed that the repurchase of Greek government bonds had commenced the prior day, after the divesture."

Karydas, group general manager of risk management and markets, who left the bank at the end of August last year, rejected any suggestion the board was unaware of the investment strategy or that he misled the board. He said in an email response to Reuters «all the executives» agreed to a policy that included possible Greek bond purchases at a meeting in November 2009.

"The ... suggestions ... were also approved by the board of directors in their December 11 meeting,» Karydas said. «It seemed to be a consensus view that Greece would overcome the crisis."

By April 2010, the bank had expanded its holding of Greek government bonds to 2.4 billion euros, a third more than the amount Kypri had told Stockwatch had been sold four months before. The investigators said this went beyond the bank's own approved 2-billion-euro limit but was approved retrospectively in May 2010.

Eliades, the former group CEO, said that Greek bonds were still well rated at the time and in demand internationally: «We cannot judge, with today's circumstances, actions which took place at a different time when Greek bonds had very high demand,» he said. «Everyone was buying into Greek bonds."

By comparison, however, data from «stress tests» carried out by EU authorities concerned about the health of their banks, showed that at the end of 2010, most of the 10 biggest banks on the continent, many times larger than the Cypriot lenders, held nothing like as much Greek debt as did Bank of Cyprus and Laiki.

They had 2.2 billion and 3.3 billion euros respectively, outstripped among top 10 banks only by French giants BNP Paribas and Societe Generale. The same EU data showed that Britain's Barclays had only 192 million euros and Lloyds none at all.

As investors' fears over the solvency of Greece grew, the value of the Greek bonds fell. The Bank of Cyprus made changes to the way it accounted for the bond holdings, according to the Alvarez and Marsal report, with the result that the growing potential losses were not spelled out to investors.

In April 2010, it moved about 1.6 billion euros of Greek bonds from its trading account to its «held to maturity» book. This meant the bank did not have to mark down the value of the bonds.

The accounting move was made on the grounds that Greece would redeem the bonds. The report authors said: «The justification provided does not appear to be strong."

Eliades told Reuters: «Nobody could possibly expect that a European country, in the euro, could possibly default."

Last year, however, the EU and IMF bailout terms relieved Greece of the need to repay up to 80 percent on its bonds, leaving the Bank of Cyprus with losses of 1.8 billion euros.

The bank declined to respond to an allegation made in the report that data that could have been relevant to understanding why it bought so much Greek debt may have been deleted.

That data, the authors say, was wiped from the computer of Christakis Patsalides, an executive involved in buying bonds, using special software on October 18 last year. When investigators examined it, there was a 15-month gap in emails in 2009-2010.

There is no suggestion Patsalides himself deleted them. He told investigators that he was unaware of any missing data, according to the report. Patsalides declined comment to Reuters but told investigators for the report that had thought the bank's ceiling for its Greek bond holdings had been set at «too high a limit».

From the moment he was ‘chosen’ (rather than elected) Enrico Letta (left) made it clear: no more austerity for Italy. Just in case anyone in Brussels-am-Berlin might be hard of hearing, yesterday in the Italian assemby, Signor Letta gave everyone a watch-my-lips moment: austerity is dead, time to change course. Despite troll propaganda to the contrary, I’ve been saying for nearly a year now that events in ClubMed and then opposition at home will lead to Germany leaving the euro before Greece does. Yesterday, Enrico Letta turned that strong likelihood into a near-certainty.

The balance of power in the EU changed the minute Francois Hollande was elected President of France. Last week, a suitably well-timed leak from Hollande’s Parti Socialiste berated “German austerity” and the “egoistic intransigence of Mrs Merkel”. For the last six months, Spain has been poking the eurocrats in the eye, and deriding the output of Olli Rehn. Beppo Grillo changed the game in Italy, and with a bit of luck Alekos Alavanos might do the same in Greece. The openly anti-EMU Alternativ für Deutschland (AfD) is already, as of yesterday, the fastest-growing Party in German history.

But for those who would like the EU to return to its Common Market days (minus only Brussels) there is still a long way to go. Lest anyone be in any doubt about this, Enrico is a dyed-in-the-wool pro-EU Leftie of the old school. What he wants is a reconfigured EU in which default is recognised as an option and Nordeurope doesn’t wind up carpetbagging its way across a scorched-earth ClubMed. Given his own way, Wolfgang Schäuble would go merrily carpetbombing his way through Southern Europe until everyone was suitably in line or dead, but that’s not going to happen now. And while Letta might think the euro can be saved, the obvious market reality is that it can’t. It’s all coming to a rather unpleasant boil.

One major unanswered question is what will Italian bond yields now do? The yield on 10-year Italians fell 0.08% to 3.975%, back towards the 3.895% last week’s unlikely low – which was itself the cheapest Italian debt cost since November 2010. Six months ago yields soared above 7%, but today – with the collapse of fiscal consolidation in sight and Italian politics more deadlocked than ever – they’re below 4. Go figure.

Another of my long-running ClubMed hobby-horses (informed by Spanish and Italian contacts rather than guesswork) is that various governments in Rome have been lying for Europe about their true financial state for donkey’s years: they’re just better at it than the Greek elite. More and more of this is coming to light, but still the yields stay lower than a double-jointed anorexic limbo-dancer. Go figure.

Well alright, if you insist, I will. The markets must decide, as rusting iron ladies were wont to remark, but unfortunately markets are often driven by people on the other side of the Pond who don’t understand europolitics…..and couldn’t analyse their way out of a paper bag anyway. For them, any Government is better than none. Then we mustn’t forget the awesome power of Draghula in Frankfurt, who was (you can be certain) keeping the Italian bond sale and subsequent yields on an even keel last week. Don’t try and work out how he does it: I certainly can’t, and neither can anyone else. But just as gold shouldn’t be down at $1465, the Dow shouldn’t be as high as 14,700, Britain didn’t really evade a recession last week and all the West’s unemployment/inflation data is a figment of Billy Bureaucrat’s limited imagination, so too there is no real confidence about Italy’s prospects out there among the smart money. I’d imagine that sooner rather than later, even the suckers must work that out: at which point, it will become a case of Whatever It Takes from SuperMario.

It’s a heady brew is this WIT. Berlin has felt for some time that Draghi should be renamed Mario Dragusdown, and Frankfurt is positively demented about the possibility of another 1923 heading its way. But unlike Enrico Letta, the man atop the ECB paper mountain is his own boss. He cannot be fired, and Germany cannot stay in the eurozone as long as he’s there.

Meanwhile, as I shall expand a little later, Germany is about to face some banking problems of its own. Stay tuned.

Eurostat also reported this morning that inflation across the Eurozone has fallen to just 1.2% in April. That's a sharp fall on March's 1.7%, and a much smaller rise in the cost of living than analysts had expected.

That makes it more likely that the European Central Bank will bow to pressure and cut interest rates at its next monthly meeting on Thursday.

Spanish recession to continue

Looking back at Spain's ongoing recession (see 8.02am onwards), and economists fear that the contraction will be repeated through the year.

Silvio Peruzzo of Nomura doesn't expect to see growth until "some time next year", adding"

We recognize the reforms of the government have been significant, but the problem is the starting position of the Spanish economy was much worse than any other European economies and adjusting in this environment is a lengthy process.

And the latest IMF forecast is for a 1.6% contraction in Spain this year.

However, Reuters flags up that finance minister Luis de Guindos struck an upbeat tone on Spanish radio:

All the indicators which look forward in Spain point to recovery, and a much better economy than one year ago.

Is he right? Well, trade data today showed that Spain's current account deficit came in at €1.3bn in February, down from €5.88bn. Exports rose 4.4% in the month, while imports shrank by 8.2%.

Italian unemployment rate sticks at 11.5%

Italy's jobless data, just released, is better than expected - but still shows a country struggling with a severe youth unemployment problem.

The overall Italian unemployment rate was recorded at 11.5% in March, in line with February (which was revised down from 11.6%).

The jobless rate among under-25s, though, rose to 38.4% from 37.8%

The data also confirmed that Italy faces a major problem getting people into the jobs market at all -- its employment rate was just 56.3% (down 0.1 percentage point).

Spanish recession continues

As feared, Spain's economy has contracted by 0.5% for the seventh quarter in a row.

Data just released confirmed analyst forecasts, with Spanish GDP now 2% smaller than a year ago as the country's austerity programme -- and the wider eurozone recession -- continue to bite.

Good morning, and welcome to our rolling coverage of the latest events in the eurozone crisis and across the global economy.

It could be another morning of bad economic news in Europe, as the ongoing recession hits firms and forces more people out of work.

The latest eurozone unemployment data, due at 10am BST, is expected to show the region's jobless rate has risen to a new record high of 12.1% in March (from 12% last month).

Italy's unemployment rate is also forecast to increase, showing the challenges facing its new government as it strives to drag the country back to growth.

And in Spain, new GDP data will doubtless confirm that the country's economy contracted again in the first three months of 2013 (economists expect a fall of 0.5%).

As Michael Hewson of CMC Markets puts it this morning:

The Spanish economy continues to buckle under record high unemployment of 27% and rapidly declining house price values.

With ratings agency Standard and Poor’s predicting that property prices could fall another 13% by year end the prognosis looks grim not only in Spain but for the rest of Europe as well.

A grim tale indeed, and one which will set the scene for a meeting tonight between the new Italian prime minister, Enrico Letta, and German chancellor Angela Merkel.

Having won hist first confidence vote last night (see Monday's blog), Letta faces a second one in the Italian Senate today. But visit to Berlin this evening will could be more exciting, following his pledge to spare Italy from 'fiscal consolidation alone'.

There could also be drama in Cyprus today, as its parliament votes on the terms of the country's bailout deal. The plan is expected to be passed with a narrow majority, but there could be fiery criticism of the way the deal was (mis)-handled.

Submitted by Tyler Durden on 04/30/2013 21:49 -0400

Submitted by Tyler Durden on 04/30/2013 21:49 -0400

No comments:

Post a Comment