http://globaleconomicanalysis.blogspot.com/2013/02/france-sinks-further-into-gutter-france.html

Thursday, February 21, 2013 2:19 PM

France Sinks Further Into Gutter; PMI Accelerates to 4-Year Low; "Core" of Europe Now Consists of Germany Only

While laughing at the amusing exchange of letters between the CEO of Titan and Arnaud Montebourg, Minister of Industrial Renewal of France, I awaited the latest PMI report on France, expecting findings to be horrific.

The PMI reports are out today, and inquiring minds will note the Markit Flash France PMI shows the decline in French private sector output accelerates further to reach near four-year record.

The PMI reports are out today, and inquiring minds will note the Markit Flash France PMI shows the decline in French private sector output accelerates further to reach near four-year record.

Key points:

- Flash France Composite Output Index drops to 42.3 (42.7 in January), 47-month low

- Flash France Services Activity Index falls to 42.7 (43.6 in January), 48-month low

- Flash France Manufacturing PMI climbs to 43.6 (42.9 in January), 2-month high

- Flash France Manufacturing Output Index rises to 41.2 (40.8 in January), 2-month high

Summary:France Economic Output

Latest Flash PMI data indicated that the downturn in French private sector output deepened in February. January’s Markit Flash France Composite Output Index , based on around 85% of normal monthly survey replies, slipped from 42.7 in January to 42.3, its lowest reading since March 2009.

The steeper fall in overall output was driven by an accelerated decline in the service sector where activity contracted at the fastest pace in four years. Manufacturers signalled a slightly slower decrease in production compared with one month previously, albeit still sharper than signalled in the service sector.

New business placed with private sector companies in France fell again in February, extending the current sequence of contraction to one year. The rate of decline quickened slightly since January and was only marginally slower than December’s 45-month record.

Service providers indicated that new business fell at the sharpest rate for just under four years. Survey respondent s commented that difficult business conditions and intensifying competitive pressures had conspired to depress inflows of new work.

Expect GDP to follow the PMI far more than economists expect.

Eurozone Aggregate PMI

The Markit Flash Eurozone PMI shows steepening downturn in February.

Key Points:

- Flash Eurozone PMI Composite Output Index at 47.3 (48.6 in January). Two-month low.

- Flash Eurozone Services PMI Activity Index at 47.3 (48.6 in January). Three-month low.

- Flash Eurozone Manufacturing PMI at 47.8 (47.9 in January). Two-month low.

- Flash Eurozone Manufacturing PMI Output Index at 47.5 (48.7 in January). Two-month low.

The Markit Eurozone PMI® Composite Output Index fell to 47.3 in February from 48.6 in January, according to the flash estimate. The decline signals a steepening of the economic downturn, contrasting with the easing trend seen in the previous three months. Business activity has now declined throughout the past year-and-a-half, with the exception of a marginal increase in January last year.

Output rose for the third month running in Germany, albeit at a slower rate, contrasting with accelerating, steep rates of decline in both France and across the rest of the Eurozone on average. French businesses were particularly weak, reporting the largest monthly drop in output since March 2009. Outside of France and Germany, the rate of decline was the fastest for three months, though it was weaker than the downturn seen in France.

New orders fell for the nineteenth month running, with the rate of decline gathering pace having eased to the weakest for 11 months in January. However, the overall rate of loss in February remained less steep than that seen throughout much of 2012."Core" of Europe vs. Periphery

Chris Williamson, Chief Economist at Markit said: "A steepening rate of decline in February is a disappointment, and suggests that the eurozone is on course to contract for a fourth consecutive quarter in the first three months of the year. Digging into the data shows increasing schisms within the eurozone. National divergences between France and Germany have widened so far this year to the worst seen since the survey began in 1998. Germany is on course to grow in the first quarter, recovering from the 0.6% GDP fall seen in the fourth quarter, possibly expanding by as much as 0.4%. In contrast, France’s downturn is likely to deepen, bringing the euro area’s second-largest member more in line with the periphery than with the now solitary-looking German ‘core’.”

Recall that the "core" of Europe was once Germany, France, and Italy. Italy went down the tubes long ago and the "core" became Germany and France. The "core" is now Germany.

Rotten to the Core

Last month the eurozone composite PMI rose from 47.2 to 48.6.

Chris Williamson, Chief Economist at Markit offered this interpretation: "The eurozone is showing clear signs of healing, with the downturn easing sharply in January and the region moving closer to stabilisation in the first quarter."

I offered a completely different interpretation on February 7 in Illusions of Stabilization.

No Signs of HealingIllusion of Eurozone Stabilization

I disagree with Williamson. Those divergences show the eurozone is getting sicker, not healing.

If there was any healing, and certainly if there was any rebalancing, manufacturing and export growth would be picking up in Spain, in Italy, and in France at the expense of Germany.

There is no real stabilization and there is no healing. Rather, the policies of Hollande are so disastrous that some output has shifted to Germany and elsewhere, (coupled perhaps with some inventory replenishment and a temporary stimulus-fueled increase in demand in Asia).

Even that cannot last. How can it?

US growth has stalled (at best) and 2% payroll tax cuts will tip the US into recession (assuming it's not there already).

With employment sinking in France, Italy, and Spain, precisely who will buy German exports?

Properly rebalancing will require a shift in production from Germany to the rest of Europe as well as a shift towards more consumption in Germany from the rest of Europe. That cannot and will not happen with the destructive polices of Hollande, and the lack of reforms in Spain and Italy.

Something has to give. And it's something very few people see coming.

Germany Will Pay a Steep Price

One way or another Germany will pay a huge price.

These are the only two eurozone recovery options

- Germany gives (not lends) more bailout money to the rest of Europe

- The eurozone breaks up

Until one of those things happens, signs of stabilization are nothing but an illusion.

There are no other options, and no other choices. Meanwhile, imbalances grow and German taxpayers keep funneling tax dollars to the Southern states to keep them afloat.

How long German citizens are willing to put up with this sorry state of affairs remains to be seen.

http://www.telegraph.co.uk/news/worldnews/europe/italy/9884499/Silvio-Berlusconi-accused-of-trying-to-buy-votes-days-before-election.html

10:22PM GMT 20 Feb 2013

The letters were sent out by the billionaire's centre-Right PDL party as Italians prepare to vote on Sunday and Monday, in one of the country's most important elections for years.

Mr Berlusconi's political rivals said the letters were misleading because at first glance they looked like official rebate notices from the Italian inland revenue.

But they could well produce a last-minute surge in support for Mr Berlusconi – a poll this month found that nearly 40 per cent of voters favoured the idea of being reimbursed for the IMU tax, which was introduced by the caretaker government of Mario Monti, the outgoing prime minister.

Economists, however, have estimated that the tax rebate would cost the cash-strapped country up to eight billion euros, at a time when it is struggling to emerge from one of the deepest recessions since the Second World War.

The letters came in official-looking envelopes which were marked "Important notice: reimbursement of IMU 2012".

and....

http://www.nakedcapitalism.com/2013/02/martin-wolf-misses-the-real-reason-the-eurozones-unhappy-marriage-has-not-broken-up.html

WEDNESDAY, FEBRUARY 20, 2013

Martin Wolf Misses the Real Reason the Eurozone’s Unhappy Marriage Has Not Broken Up Yet

The normally astute and blunt Martin Wolf is either having an uncharacteristic bout of circumspection or is managing to miss an important, arguably determining reason why the Eurozone persists in inflicting destructive austerity on much of its population.

As his current column shows, Wolf is under no illusion as to the success of the Eurozone experiment and reminds readers it could still fail:

The currency union is supposed to be an irrevocable monetary marriage. Even if it is a bad marriage, the union may still survive longer than many thought because the costs of divorce are so high. But a bad romance is still fragile, however large the costs of breaking up. The eurozone is a bad marriage. Can it become a good one?…If all members of the eurozone would rejoin happily today, they would be extreme masochists. It is debatable whether even Germany is really better off inside: yes, it has become a champion exporter and runs large external surpluses, but real wages and incomes have been repressed. Meanwhile, the political fabric frays in crisis-hit countries. Anger at home and friction abroad plague both creditors and debtors.What, then, needs to happen to turn this bad marriage into a good one? The answer has two elements: manage a return to economic health as quickly as possible, and introduce reforms that make a repeat of the disaster improbable. The two are related: the more plausible longer-term health becomes, the quicker should be today’s recovery.

Wolf then proceeds to tell us that the Eurozone continues to be a resolute practitioner of austerity policies. Readers may recall that there was a huge kerfluffle in the economics-related media when the IMF admitted it was all wrong, that the fiscal multipliers in the Eurozone had turned out to be larger than one. In econ-speak that means you can’t starve your way back to health. Cutting fiscal deficits results in an even greater economic contraction, resulting in even worse debt to GDP ratios. But the rest of the European officialdom seems to be in shoot-the-messenger mode. Per Wolf:

In a recent letter to ministers, Olli Rehn, the European Commission’s vice-president in charge of economics and monetary affairs, condemned the International Monetary Fund’s recent doubts on fiscal multipliers as not “helpful”. This, I take it, is an indication of heightened sensitivities. Instead of listening to the advice of a wise marriage counsellor, the authorities have rejected it outright.

Wolf says the way out is more debt writedowns and restructurings, internal rebalancing, and financing national deficits as the rebalancing is in process. At this remove, I don’t see how this happens. Germany still wants to have its cake and eat it too. It does not want to give up running surpluses with the rest of the Eurozone and keep financing its trade partners. The fact that it insists on irreconcilable objectives is putting the periphery into a depression which will eventually infect Germany.

Wolf argues that the reason the Eurozone has not broken up despite pursuing such destructive policies is that a breakup would be worse. The question might be for whom. Greece has been the test case. Even though a Greek departure would not have significant economic ramifications for the rest of the Eurozone, the fear is that it would lead to contagion, since if Greece left, it would demonstrate to other periphery countries that it could be done too.

And one has to wonder why Greece has not left. By all accounts, the country is falling apart. Many medicines are in inadequate supply, sheets in hospitals are being re-used, and barter is becoming common as the economy is breaking down. Things are now so desperate that infrastructure is being damaged as desperate citizens try to pilfer metals. From Greek Reporter:

So why are the periphery countries suffering this level of unproductive pain? Because the countries aren’t making the decisions. It’s powerful local politicians who are selling out their countries, working in cahoots with Eurozone technocrats. And I can assure you none of them are sharing in the suffering of periphery country workers.

This is the plague of our modern social order: detached and corrupt leaders, whether intellectually, monetarily, or both. The old code of noblesse oblige, which at least required the elites to have some concern about what happened to the lower orders, is a dead letter. It’s curious that someone as incisive as Wolf is unwilling to factor the behavior of the ruling classes into his assessment. Perhaps, as Michael Thomas said of Punch Sulzberger, he is dining with people he should be dining on.

Wolf argues that the reason the Eurozone has not broken up despite pursuing such destructive policies is that a breakup would be worse. The question might be for whom. Greece has been the test case. Even though a Greek departure would not have significant economic ramifications for the rest of the Eurozone, the fear is that it would lead to contagion, since if Greece left, it would demonstrate to other periphery countries that it could be done too.

And one has to wonder why Greece has not left. By all accounts, the country is falling apart. Many medicines are in inadequate supply, sheets in hospitals are being re-used, and barter is becoming common as the economy is breaking down. Things are now so desperate that infrastructure is being damaged as desperate citizens try to pilfer metals. From Greek Reporter:

The thieves are accused of stealing industrial cable, power-line transformers and other metal objects – triggering blackouts and massive train delays. The profile of the metal thief is also changing, authorities say, from gypsies and immigrants living on the margins of society to mainstream Greeks who have fallen on hard times. A group of men were caught trying to take apart an entire bridge and droves of immigrants can be seen pushing shopping carts around Greek neighborhoods looking in recycling bins…It is hard to imagine how an exit could make matters any worse. Greece would get the Eurozone boot off its neck, be able to deficit spend to get its idle resources back to work, and depreciate its currency to make its goods more attractive on world markets.

Athens’ nine-year-old light rail system has been a prime magnet for metal robbers, with at least five major disruptions reported in the past six months due to cable theft that forced passengers to hop on and off trains as diesel replacements were needed. The trend has had lethal consequences: In early January, the body of a 35-year-old man was found near Athens beside the tracks of a suburban rail system that services the capital΄s airport. He had been electrocuted while cutting live cables, police said.

So why are the periphery countries suffering this level of unproductive pain? Because the countries aren’t making the decisions. It’s powerful local politicians who are selling out their countries, working in cahoots with Eurozone technocrats. And I can assure you none of them are sharing in the suffering of periphery country workers.

This is the plague of our modern social order: detached and corrupt leaders, whether intellectually, monetarily, or both. The old code of noblesse oblige, which at least required the elites to have some concern about what happened to the lower orders, is a dead letter. It’s curious that someone as incisive as Wolf is unwilling to factor the behavior of the ruling classes into his assessment. Perhaps, as Michael Thomas said of Punch Sulzberger, he is dining with people he should be dining on.

and.....

http://www.guardian.co.uk/business/2013/feb/21/eurozone-crisis-live-french-economy

Eurozone services data dash hopes of recovery

Ouch. Eurozone PMIs do not look good, with services dropping in February, dashing hopes that the region could emerge from a recession soon.

The flash services PMI – one of the earliest monthly indicators of economic activity in the region – dropped from 48.6 to 47.3 in February, a big miss from analyst expectations of a rise to 49.

Chris Williamson of Markit highlighted the growing divide between Germany and France.

Digging into the data shows increasing schisms within the eurozone. National divergences between France and Germany have widened so far this year to the worst seen since the survey began in 1998. Germany is on course to grow in the first quarter. In contrast, Frances’s downturn is likely to deepen, bringing the euro area’s second-largest member more in line with the periphery than with the now solitary-looking German ‘core’.

Grim outlook for Europe's second largest economy

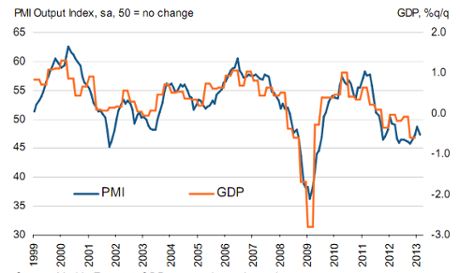

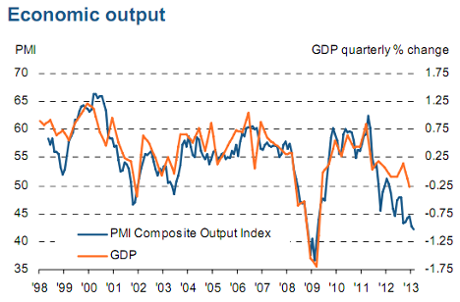

Here's Markit's graph showing just how bad it looks in France. The composite PMI, which usually preempts GDP data fairly accurately, is sliding dramatically.

This morning the French media suggested the EU Commission is expected to cut its already grim forecast for France's economy and budget deficit this year, citing a report due out Friday.

Le Monde and Le Point reported that the commission's economic experts have reduced their forecast for France's economic growth this year to 0.1% from 0.4%.

The country's deficit is now forecast at 3.6% of GDP, up from a prior estimate of 3.5%, which would miss the Maastricht treaty target of 3%.

France is the second largest economy in the eurozone and problems there signal problems right at the very heart of the currency bloc.

Markets hit by Fed split

Over to the markets, which are suffering after minutes released last night showed signs of a split over the US Federal Reserve's stimulus programme.

- UK FTSE 100: down 1.2%, or 80 points, at 6314

- France CAC 40: down 1.2%

- Germany DAX: down 1.2%

- Spain IBEX: down 1.75%

- Italy FTSE MIB: down 2%

German data points to economic rebound

German business activity, meanwhile, increased for a third straight month in February, adding to signs the region's largest economy is rebounding after GDP declined in the fourth quarter.

The data points to a widening gulf between it and the region's second largest economy, France, which continues to flounder.

The German composite PMI, which accounts for more than two thirds of the economy, stood at 52.7 in February. That was down from January's 54.4, but still comfortably above the 50 mark that separates growth from contraction.

The six problems with Italy and how to solve them

While we wait for Germany's PMIs, check out the Guardian's spread on Italy in the paper this morning.

My colleague Lizzie Davies in Rome numbers the six things wrong with Italy and how to solve them, starting with the effects of austerity.

She goes on to highlight the plight of women in the country run for years by Silvio Berlusconi, a man better known for his bunga bunga parties than anything else. She writes:

Held back by ingrained cultural attitudes, inadequate public services and political under-representation, they may have better educational qualifications than their male counterparts but they are significantly less likely to be in paid work.

French services sector shrinks at fastest rate in four years

The French data is predictably bad. The French services sector shrank in February at its fastest rate in nearly four years, suggesting it is far from a turnaround.

The services PMI came in at 42.7 in February, compared with 43.6 last month. The manufacturing index ticked up to 43.6, but remains well below the 50 mark that separates growth from contraction.

The composite PMI, which accounts for roughly two-thirds of French economic output, dropped to 42.3 from 42.7 in January.

Chris Williamson at Markit said:

There is a fairly consistent picture showing that the French business sector is suffering its worst downturn since the height of the financial crisis.

No comments:

Post a Comment