Commentary on the economic , geopolitical and simply fascinating things going on. Served occasionally with a side of snark.

Tuesday, January 8, 2013

Japan , Europe and US reduced to various frauds , beggar thy neighbor schemes and gimmicks rather than sound economic policies to keep their respective ponzi schemes going ..... no other way to put it.

Japan has announced that it will help Europe through its debt crisis by purchasing bonds issued by the eurozone bailout fund.

Speaking in Tokyo this morning the new Japanese finance minister, Taro Aso, announced that Japan plans to "continuously" take part in debt auctions conducted by the European Stability Mechanism, possibly starting today.

Aso refused to say how much Japan would buy, but insisted the plan would support Europe -- and also benefit Japan by helping to weaken the yen.

Aso said:

Stability in Europe's financial situation helps stabilise currencies including the yen.

From this standpoint and based on Europe's further efforts on financial stability, Japan will purchase a portion of ESM bonds continuously by utilising foreign reserves.

Taro Aso. Photograph: KIM KYUNG-HOON/REUTERS

Aso's commitment will be welcomed in the eurozone, as the ESM is holding its first debt auction later today, selling three-month notes worth about €2bn.

The money raised from ESM bond sales is used to fund eurozone bailout programmes.

Masaaki Kanno, chief economist at JPMorgan Securities, told Bloomberg that Aso's pledge would go down well in Europe:

The Europeans would be happy to see Japan buy ESM bonds, so Japan can avoid criticism from abroad and at the same time achieve its objective.

Japan already owns around €7bn of bonds issued by the eurozone's temporary rescue fund, the EFSF.

Just when we thought America would be alone in crossing into the monetary twilight zone where so many Keynesian lunatics have gone before, and where trillion dollar platinum coins fall from the sky right onto the heads of all those who have not even the faintest understanding of money creation, here comes Japan:

ASO: JAPAN TO BUY ESM BONDS

ASO SAYS JAPAN TO BUY ESM BONDS USING FOREIGN EXCHANGE RESERVES

ASO: ESM PURCHASES WILL HELP TO STABILIZE YEN

JAPANESE FINANCE MINISTER ASO SPEAKS TO REPORTERS IN TOKYO

ASO SAYS AMOUNT OF JAPAN’S ESM BOND BUYS UNDECIDED

For those who have forgotten, the E in ESM stands for European (the S for Stability), notJapanese (Stability). Otherwise it would be, er... well, JSM. Keynesian at that. But yes - Japan will now proceed to "stabilize" itself by monetizing European debt. Because its own JPY 1 quadrillion in debt was not enough.

As for a rehash of the old lunacy, which just like the OMT has driven the JPY much lower on nothing but innuendo and speculation, and will end the second the BOJ's plan is formalized, we get:

ASO WANTS STATEMENT ON BOJ, GOVT COOPERATION

AMARI SAYS GOVT, BOJ TO COOPERATE ON PRICE TARGET

Of course, when the latest and greatest "invention" out of the soon to be annexed 4th branch of Japanese government fails, and this time is not different after all, Japan will shock everyone when it unveils to the world...

He says he does think that under current law such coins would allow the Treasury to circumvent the debt ceiling, but that he "couldn't believe" it is gaining traction as a serious proposal.

"I'm not a lawyer, so let me start with that. But the gentleman who is promoting it is the top Democrat on the Judiciary Subcommittee on the Constitution," the Congressman told Business Insider in an interview, referring to the idea that has been floated most prominently by Rep. Jerry Nadler.

"I assume that he has studied the legal ability to do this. But clearly if he chairs the Constitution Subcommittee, he's done his research. He's a smart man. And so therefore, I'm taking it at face value that the authority is there to allow the minting of a trillion-dollar coin, and that shouldn't be allowed."

Walden took interest in proposing legislation to ban the option because he thought the idea of minting a platinum coin to work around the debt ceiling was a particularly absurd idea that exemplified "the problem of people in Washington not understanding the reality" of the national debt. Walden also thought that if the Treasury did mint the coin, it would lead to a "very inflationary" period.

"The notion that we could mint a trillion-dollar coin ... and all of a sudden, your debt issue is gone — it's so absurd and laughable, except people were being serious," Walden said. "This just has to stop. So that's why we're drafting legislation today."

What Walden is suggesting is not quite the issue — Nadler and others in the media have proposed issuing the coin to continue paying the nation's bills in the case that the debt ceiling is not raised. It is not being floated as an option to rid the U.S. of its debt. There's also some debate over whether it would lead to a period of massive hyperinflation.

Walden didn't get too specific when asked what he would demand from President Barack Obama and other Democrats in order to lift the debt ceiling. But he did say he subscribed to the so-called "Boehner rule" that demands one dollar in spending cuts for every dollar increase in the debt ceiling.

One exchange he said he would not accept: banning the trillion-dollar coin in exchange for a permanent elimination of the debt ceiling so that it would be automatically raised.

"It used to be done automatically without a vote, and that's part of why we have the debt level that we have — Congress could just spend and never be held accountable," Walden said. "Now, we're making Congress and the administration take notice of what their spending habits have done to the country, and that's a good thing in terms of turning this thing around."

And US gimmicks - why we will be Greece / Spain sooner than one might think .....

There is a lot of crazy talk out there regarding the minting of a $1 trillion coin to get around the debt ceiling.

Today Paul Krugman hopped on the $1 trillion bandwagon in his New York Times article Be Ready To Mint That Coin.

Should President Obama be willing to print a $1 trillion platinum coin if Republicans try to force America into default? Yes, absolutely. He will, after all, be faced with a choice between two alternatives: one that’s silly but benign, the other that’s equally silly but both vile and disastrous. The decision should be obvious.

For those new to this, here’s the story. First of all, we have the weird and destructive institution of the debt ceiling; this lets Congress approve tax and spending bills that imply a large budget deficit — tax and spending bills the president is legally required to implement — and then lets Congress refuse to grant the president authority to borrow, preventing him from carrying out his legal duties and provoking a possibly catastrophic default.

Enter the platinum coin. There’s a legal loophole allowing the Treasury to mint platinum coins in any denomination the secretary chooses. Yes, it was intended to allow commemorative collector’s items — but that’s not what the letter of the law says. And by minting a $1 trillion coin, then depositing it at the Fed, the Treasury could acquire enough cash to sidestep the debt ceiling — while doing no economic harm at all. So why not?

$1 Trillion Not Enough

Krugman asks "why not?" The answer should be obvious. It's crazy to think $1 trillion would be enough. A year or two from now, the Treasury would have to mint another coin, with the same silly debate we are having right now about whether the process is legal. Question of Legality

I do not accept the idea that the proposed process would be legal. Others side with me as well. Here are a few examples:

Nonetheless Tut! Tut! I say to Krugman detractors.

Does any president care what is legal? Roosevelt didn't. Nixon didn't. Bush didn't. Obama didn't.

We all know presidents are above the law and they do what they want anyway. Kidnapping, torture, wiretapping, holding people without charges in Cuba, data gathering of all sorts with drones and other measures without due cause and in direct violation of the constitution, so clearly the constitution is meaningless already.

No one will possibly do anything if Obama breaks the law as Krugman wants. Krugman's major error is $1 trillion is nowhere near enough.

Let me be first to support the idea of a $1 quadrillion coin.

Krugman's second error is in regards to whose picture should be on the coin. I propose this picture for the front of the coin.

The back of the coin should be equally obvious. Paul Krugman Prays for America.

The only way to finance a big European-style state is to have it paid for by massive taxation of everyone, mostly the middle class. Right now, we are avoiding honest debate on this fact.

The central issue of our time is the debate over the size and scope of government. Two unpleasant but undeniable mathematical truths limit the feasible policy choices. The recent sound and fury of the fiscal cliff follies in the end signified nothing because the resolution was in fact just a denial of both truths.

The first truth is that the current tax rates cannot support the promises made to middle-class Americans. The most unaffordable items in fiscal projections are Social Security for everyone and government-sponsored health care for the middle class. You cannot preserve these even with Draconian slashing of military, infrastructure, welfare, education, and other expenditures.

The second truth is that you cannot pay for the Life of Julia, or any vision of a cradle-to-grave welfare state, without massive and increasingly regressive middle-class taxes. The poor don't have the money to pay for a European-style welfare state, and the rich, rich as they are, don't have anywhere near enough.

Not only that, it's easy to tax middle-class assets and transactions — things like payrolls, sales, and real estate — but soaking the rich means taxing investments. Investments are complicated and can be restructured to minimize taxes. Also, investments are the lifeblood of economic growth. Raising significantly more taxes from the rich also requires higher marginal tax rates — and their rates are already quite high. High marginal rates distort the economy and yield less revenue than anticipated because they increase the rewards for legal and illegal tax avoidance.

That's not to say it's impossible to get more money from the rich, but it's tricky and past attempts have typically been less effective than forecast and often counterproductive. Moreover, even under the most optimistic assumptions, taxes on the rich — or taxes on businesses, financial transactions, or anything else aimed at the rich (and often hitting others) — will still not cover a large fraction of the costs of a European-style welfare state. Ask the Europeans — they’ve tried it all and failed.

To be in our political center today, you have to deny both these truths and pretend that if we sharpen our pencils and make a bunch of wildly optimistic assumptions, we can close a few tax loopholes, cut some waste from spending, and maybe nudge upper-income tax rates up a little, and continue merrily on the same big-and-growing-bigger government path without unfortunate consequences. This is a “balanced approach,” as it ignores both mathematical truths equally, but the denial of clear reality means this approach is doomed to fail.

Surprisingly, many progressive pundits are moving away from their traditional complaint that America’s tax code is too regressive, favoring the rich. They are starting to tell us, albeit only after an election mainly contested on these issues, the truth: to fund the European-style social welfare state which they advocate, we must tax everyone more.

For example, Ezra Klein, blogging for the Washington Post on December 7th, writes,“The need for tax receipts to grow underscores the necessity of finding an efficient way to collect them. Experts say that should include tax reform and new tax sources that take the pressure off the income tax, such as a value added tax or a carbon tax.”

Klein is mild compared to Eduardo Porter, who writes in the New York Times on November 27th, “Many Americans may find this hard to believe, but the United States already has one of the most progressive tax systems in the developed world” and “Taxes on American households do more to redistribute resources and reduce inequality than the tax codes of most other rich nations.” Mr. Porter, it is shocking to see you argue in the New York Times that the United States is a progressive paragon! Those in the Occupy Wall Street movement must be surprised to learn that you, one of their standard-bearers, think the United States already does considerably more redistribution than Western Europe!

These pundits know the math. To achieve anything like the European-style entitlement state they advocate, we need to tax everyone a lot more, not just the 1 percent. Despite all the drum circles protesting the inequitable distribution of resources, the wealthy just don’t have enough. The middle class and even the poor must step up to carry more of the burden if this is our desired endgame.

In his November 27th op-ed, Porter also writes “The experience of many other developed countries suggests that paying for a government that could help the poor and the middle class cope in our brave new globalized world will require more money from the middle class itself,” and “Big-government social democracies, by contrast, rely on flatter taxes to finance their public spending.”

In a similar vein, Jared Bernstein, a senior fellow at the Center on Budget and Policy Priorities and a former economist for Vice President Biden, writes, "It's perfectly reasonable for the White House to begin collecting more revenue from folks who have done by far the best in pretax terms." But wait a moment for it — he then adds, "But ultimately we can't raise the revenue we need only on the top 2 percent."

Note the use of “2 percent,” a number the president himself has begun using more often. It is a small but telling evolution from decrying the “1 percent.” One wonders if the Occupy Wall Street protestors have corrected their signs to read “We are the 98 percent”? Are those in the 98th percentile already saying “They came for the 1 percent and I said nothing…”? According to the more honest progressive pundits above, it will not be long until the 50th percentile is saying it too.

If we take the logic of a Porter or Klein or Bernstein seriously — and we should — their prescription for taxes is nearly the opposite of the president’s public stance.Let’s say what Porter and others are saying but in plain English (or, failing that, let’s just underline a lot).

If we are to redistribute like Europe, we must tax like Europe. The middle class must pay more taxes and they must pay a larger share of the tax burden. The president, in contrast, is vowing to raise taxes on only the rich. One wonders if President Obama would have won the election if he had warned voters that “to pay for Obamacare, stimulus spending, increased regulatory oversight, and the rest of the big government wish list I believe important, we need to raise the level and share of taxes paid by the middle class”? One also wonders why more progressive pundits were not as clear about their goals and the necessities pre-election as they are starting to be now.

The choice the country faces is simple. We can have big government and the Life of Julia (at least for a while, but that is another essay), with everyone paying through the nose and the middle-class share of taxes rising not falling, or we can return to the American tradition of limited government, with everyone paying a smaller burden to the state, with relatively limited services for, and relatively light taxes on, the middle class.What we cannot have is the Life of Julia at no additional burden to 99 out of 100 of us. Nobody, Left or Right, really thinks that math works, no matter what they may say in public.

So what happens if we continue down the current path, with perhaps some small amount of revenue raised from some additional taxes on the rich? Remember, the only way to finance a big European-style state is to have it paid for by massive taxation of everyone, mostly the middle class. Right now we are avoiding honest debate on this fact, perhaps because those desirous of this change know the middle class would rebel if it saw the future bill it will have to pay. Instead, large government benefits are being continued and increased, and still new ones introduced, with little accurate discussion of who will ultimately pay.

What happens historically when benefits are bestowed without a bill also coming due is that we get hooked on them. Then, even when they become disasters not worth their cost, people are terrified to change them, as giving something up is indeed quite frightening.

Of course, as a byproduct of this growth in the state, many of us believe we also suffer a terrific erosion of liberty, free-enterprise, and individual responsibility and initiative.

Finally, after we become fully addicted to the latest increase in big government, the bill will ultimately be presented to everyone including, and in all likelihood over-emphasizing, the middle class and the poor. The people who were promised they would be untouched will see the largest proportional hikes. That’s exactly what has happened in Europe. We have seen this movie before, but this time we don’t need subtitles.

In other words, if we told everyone the ultimate destination right now, the country would likely reject it. But if built up in this piecemeal manner with benefits up front and the bill presented later, it can become reality.

The way to boil the frog of freedom is slowly.

We may, with open eyes, choose the reassuring security of big government with a far larger safety and subsidy net and far higher taxes for all — by no means just the “rich” but in fact more so on the middle class — and likely the sclerotic growth and dependency of Europe. Or we may choose the opposite. But we deserve an honest debate about this critical issue. A debate missing from the last election.

And European gimmicks / back door bailouts by playing games with posted collateral ......

The epic farce that is the opaque balance sheets of European banks, sovereigns, NCBs, and the ECB, continues to occur under our very eyes. Only when one sniffs below the headlines is the truth exposed with no apology or recognition of 'cheating' anywhere. To wit, following November's farcical over-payment on collateral by the ECB to Spanish banks (that was quietly brushed under the carpet by Draghi et al.), Germany'sDie Welt am Sonntag has found that the Bank of France overpaid up to EUR550mm ($720mm) on its short-term paper financing to six French and Italian banks. The reason - incorrect evaluation of the crappy collateral (i.e. the NCB not taking a big enough haircut for risk purposes) on 113 separate occasions. The problem lies in the increasingly poor quality of collateral the CBs are willing to accept (and the illiquidity of the underlying markets) - as higher quality collateral disappears; which leaves the central bankers clearly out of depth when it comes to 'risk management', no matter how many times Draghi tells us this week.

The European Central Bank continues to have problems with its collateral management, according to a German newspaper report Sunday.

The Bank of France, a member of the European System of Central Banks, has granted too much credit compared with collateral to six banks due to insufficient risk valuation discounts, or haircuts, made on the collateral, reports German newspaper Welt am Sonntag. The Bank provided credit in exchange for bonds known as Short-Term European Paper, or STEP, which it accepted as collateral from the banks, the newspaper says.

According to the report, notes worth less than 6.5 billion euros ($8.5 billion) with maturities of up to one year that were issued by the six banks benefited from risk valuation discounts that were too small. As a result, the banks were able to get up to EUR550 million in additional central bank money without having to provide the corresponding collateral, the newspaper calculates. According to the report, the six banks included French Societe Generale SA (GLE.FR) and Italy's UniCredit SpA (UCG.MI).

The banks had, however, provided sufficient other collateral overall so there was no impact on monetary policy operations, the newspaper quotes the ECB as saying.

An ECB spokeswoman, asked to remark on the report by Dow Jones Newswires Sunday, referred to the fact that there was no impact on the monetary policy operations and said she had no further comments.

Spokespeople at the Bank of France and Euroclear France weren't immediately available to comment to Dow Jones Newswires Sunday.

Within the Eurosystem, the Bank of France provides the relevant data--such as volume, coupon or default risk--on short-term European paper to the ECB. The ECB says it has little information about that market segment and refers to the BOF, according to the newspaper.

According to the ECB, in 113 cases the risk valuation discounts for STEP collateral calculated by the BOF were wrong, the newspaper says.

Bank of France said it gets the data exclusively from Euroclear France, the newspaper reports. Euroclear France belongs to Euroclear Group which also owns Euroclear Bank, itself a big player in the European short-term paper market, that could cause substantial conflict of interest, the newspaper writes.

In recent years, the ECB has substantially expanded the list of securities it accepts as collateral in monetary policy refinancing operations.

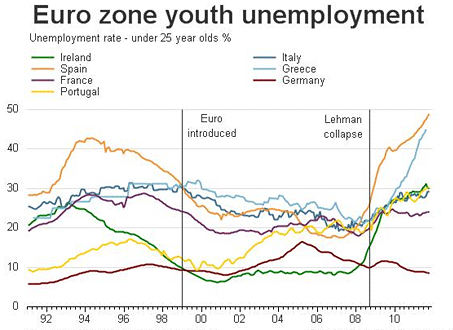

Here is the most important / explosive chart in Europe .......

Submitted by Tyler Durden on 01/07/2013 22:03 -0500

Submitted by Tyler Durden on 01/07/2013 22:03 -0500

No comments:

Post a Comment