http://ransquawk.com/headlines/finnish-finance-minister-says-finland-is-ready-to-extend-greek-loan-maturities-but-no-new-lending-to-greece-through-efsf-esm-23-11-2012

http://www.zerohedge.com/news/2012-11-23/five-little-pigs

Submitted by Tyler Durden on 11/23/2012 08:29 -0500

Submitted by Tyler Durden on 11/23/2012 08:29 -0500

"Oh, sure. Of course, you're entitled. Who doesn't want this, that, and the other?"

-Jerry & Elaine, Seinfeld

So we have the Greek debt crisis, the European Union budget problem and the European bank oversight issue and twenty-seven countries all wanting “this, that and the other” except “the other” is not that much fun unless Ms. Merkel surprises everyone by saying she is a little tired and pulling a Mae West and telling all twenty-seven nations that one will have to leave.“Boys, tell that fellow from Athens that tonight is just not his night.”

The scenario is unlikely of course but then everyone involved is now playing the grand old game of “Work Around” where someone must pay and it is going to be anybody but them. “Not this little piggy,” says the IMFand “not this little piggy” says the ECB and“not this little piggy” says the European Union. This is all because no one wants the political winds to “blow their house down” but there is the grinning big bad old wolf sitting on the mountain of debt and all of the hairs on their “chinny, chin, chins” aren’t going to change that fact. In the classic tale there were three houses with the least stable being the one made of straw and let me tell you; Greece is the straw house. Now you may have thought that the IMF’s contribution was kind of like the Fed or the ECB and that they just created money from some pork barrel but this is not the case. As a matter of fact the United States, as a 16.75% contributor to the International Monetary Fund, is on the hook for $13.4 billion of the money lent to Greece, Ireland and Portugal. Soon, in my estimation, we will have two more pigs in the pen which will be Cyprus and Spain. Change the bed sheets; its “PIGS in a blanket” for everyone!Why did the PIGS cross the road?

“Whether the PIGS crossed the road or the road crossed the PIGS depends upon your frame of reference.”

-Attributed to Albert Einstein

It used to be, in the good old days, that the amounts of money were trivial and the European stockpile was large so that more money could be shoveled into the trough and no one really cared. Every problem was handled by “Mo’ money.” Then one day the wolf trotted back to the Piggly Wiggly and the straw house had grown cavernous and Parthenon Pig had grown from piglet to porker and the credit card bill for the food and the entertainment is sitting on the table of Francois and Angela while they stare at it, try to ignore it as Austria, Finland and the Netherlands declare the offing “Not Kosher” and refuse to partake.

http://www.zerohedge.com/news/2012-11-23/black-friday-fails-bring-budget-deal-europe

Submitted by Tyler Durden on 11/23/2012 07:14 -0500

and how does the EU want to spend its budget and what new powers does Brussels seek - looks like they want in on the war mongering game....

http://rt.com/news/eu-parliament-military-resolution-380/

and....

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_23/11/2012_471344

( Stournaras has his thousand yard stare back , excuse any muttering from his mouth at this point. his Junkeritis must be inflamed as he is back to making uncorroborated statements soon to be proven " premature " , " inaccurate " , " misinterpreted " , etc... )

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_23/11/2012_471312

http://www.ekathimerini.com/4dcgi/_w_articles_wsite2_1_22/11/2012_471261

Finnish finance minister says Finland is ready to extend Greek loan maturities but no new lending to Greece through EFSF, ESM

- Greek debt sustainability, funding main issues.

Update details:

- European governments want to give Greece an extra two years, until 2022, to cut its debt to a sustainable level of 120% of GDP but the IMF does not agree.

http://www.zerohedge.com/news/2012-11-23/five-little-pigs

The Five Little PIGS

- European Central Bank

- European Union

- Finland

- Greece

- International Monetary Fund

- Ireland

- Netherlands

- Portugal

Via Mark J. Grant, author of Out of the Box,

"Oh, sure. Of course, you're entitled. Who doesn't want this, that, and the other?"

-Jerry & Elaine, Seinfeld

So we have the Greek debt crisis, the European Union budget problem and the European bank oversight issue and twenty-seven countries all wanting “this, that and the other” except “the other” is not that much fun unless Ms. Merkel surprises everyone by saying she is a little tired and pulling a Mae West and telling all twenty-seven nations that one will have to leave.“Boys, tell that fellow from Athens that tonight is just not his night.”

The scenario is unlikely of course but then everyone involved is now playing the grand old game of “Work Around” where someone must pay and it is going to be anybody but them. “Not this little piggy,” says the IMFand “not this little piggy” says the ECB and“not this little piggy” says the European Union. This is all because no one wants the political winds to “blow their house down” but there is the grinning big bad old wolf sitting on the mountain of debt and all of the hairs on their “chinny, chin, chins” aren’t going to change that fact. In the classic tale there were three houses with the least stable being the one made of straw and let me tell you; Greece is the straw house. Now you may have thought that the IMF’s contribution was kind of like the Fed or the ECB and that they just created money from some pork barrel but this is not the case. As a matter of fact the United States, as a 16.75% contributor to the International Monetary Fund, is on the hook for $13.4 billion of the money lent to Greece, Ireland and Portugal. Soon, in my estimation, we will have two more pigs in the pen which will be Cyprus and Spain. Change the bed sheets; its “PIGS in a blanket” for everyone!Why did the PIGS cross the road?

“Whether the PIGS crossed the road or the road crossed the PIGS depends upon your frame of reference.”

-Attributed to Albert Einstein

It used to be, in the good old days, that the amounts of money were trivial and the European stockpile was large so that more money could be shoveled into the trough and no one really cared. Every problem was handled by “Mo’ money.” Then one day the wolf trotted back to the Piggly Wiggly and the straw house had grown cavernous and Parthenon Pig had grown from piglet to porker and the credit card bill for the food and the entertainment is sitting on the table of Francois and Angela while they stare at it, try to ignore it as Austria, Finland and the Netherlands declare the offing “Not Kosher” and refuse to partake.

Three PIGS become five PIGS. “Deal or no Deal” results in three no deals. Howie Mandel is nowhere in sight. The wolf bangs at the door and begins to “huff and puff.” Truffles are being replaced with pork and beans. The Euro goes up. The ECB will save the world.

http://www.zerohedge.com/news/2012-11-23/black-friday-fails-bring-budget-deal-europe

Black Friday Fails To Bring A Budget Deal For Europe

- Black Friday

- China

- Consumer Sentiment

- European Central Bank

- Eurozone

- fixed

- France

- Germany

- Greece

- Gross Domestic Product

- headlines

- Italy

- Jim Reid

- Monetary Policy

- North Korea

- SocGen

- Yen

First it was Greece, which Europe couldn't "resolve" on Monday night despite Juncker's vocal promises to the contrary, and was embarrassed into postponing until next Monday when everything will surely be fixed. Now, the time has come to delay the "resolution" of the EU budget, which was supposed to be implement last night, then a decision was delayed until today, and now every European government leader is saying a new meeting will likely be needed to resolve the budget impasse.

As BBG summarizes, "Divisions between rich and poor countries flared over the European Union’s next seven-year budget, leading German Chancellor Angela Merkel to rule out an accord until the new year. France defended farm subsidies, Britain clung to a rebate and Denmark demanded its own refund, while countries in eastern and southern Europe said reduced financing for public-works projects would condemn their economies to lag behind the wealthier north. “Positions remain too far apart,” Merkel told reporters early today after the first session of a summit in Brussels. “Probably there will be no result at the end of this summit. There may be some progress but it is probable that we will need to meet again at a second stage." In other words the same old absolute and total chaos from the European Disunion we have all grown to love, in which the only solution each and every time is to delay reaching a solution, at least until after Merkel is reelected and in the meantime kicking the ever greater ball inventory in Draghi's court, where he too will promise to make everything better as long as he actually dosn't have to do anything.

On the surface this kind of political clowning should be bad for risk: however, in Europe BIS' FX trading team always operates deep below the surface, and while all the news about fixing being interrupted are ignored, what did impact the EURUSD, and thus broad risk, overnight was the reflexive German IFO Confidence release, which printed at 101.4, above expectations of 99.5, and higher than the October print of 100.0 which also happened to be the February 2012 low. Nevermind the ongoing deterioration in German PMIs, of which the service component dropped to 2009 low levels, andthat an IFO economist warned German Q4 GDP may (read "will") come in negative for the first time in years - the jittery headline scanning algos took the news and sent EURUSD higher by 40 pips, making German exports that much more uncompetitive.

In other news, the Greek deal was percolating, with various permutations being contemplated, and now even Goldman's Themistoklis Fiotakis on hope the debt buyback will be greenlighted over objections by the broader Greek society, and all those other European countries who will soon realize their EFSF funding is being used not to bailout Greece, for whom it is not a question of debt stock, but lack of GDP flow, but to generate massive hedge fund profits.

Finally, with the US trading session today at half mast, expect another record low volume half-trading day, which means a risk levitation is practically guaranteed. Headlines scanned for by the few trading algos will be anything promising a "massive", "unprecedented", "record" Thanksgiving retail season, just like last year, when a month later everything was inverted and it was subsequently learned that the bulk of the purchases had been returned to the sellers.

Some more macro previews from SocGen:

The market should be very quiet today, as many US investors are off on Thanksgiving break.All eyes will thus be on the eurozone with the publication of French and German business confidences indices. The French index hit its August 2009 low last month ahead of the publication of the 2013 budget. Thus, a correction is expected, but the index will remain at low levels. German IFO business confidence could continue to deteriorate, although it hit its February 2012 low in October.

We note that lower-than-expected indicators could revive expectations of rate cuts by the ECB on 6 December. The SG scenario does not factor in an interest rate cut as they are already very low (repo rate at 0.75% and deposit rate at 0.0%): the potential disadvantages (money market fund outflows) would outweigh the advantages (could a 25bp cut have a major impact on activity?). We will also be paying close attention to President Draghi's speech today.Overall, the EUR/USD could rapidly hit a ceiling and 2Y Bund yields fall back into negative territory.

And a complete review of what little happened overnight from Jim Reid:

Black Friday actually began on Thursday for many US consumers who cut short their Thanksgiving dinners to be amongst the first through the doors of retailers that opened earlier than usual this year. A number of chain retailers including Walmart and Toys R US were said to have opened at 8pm yesterday in an effort to kick-start sales ahead of the all-important holiday shopping season. Although for those who wish to let the fingers do the walking and shop from the comfort of your homes Cyber Monday also presents an attractive alternative. So watch out for commentary from retailers and industry groups next week for this weekend’s sales performance which should shed some light on consumer sentiment amid the ongoing ‘fiscal cliff’ uncertainty.

With the US markets closed for Thanksgiving, yesterday was a relatively quiet day for markets. In Europe, the Stoxx600 closed at the day’s highs (+0.59%) led by solid gains in the peripheries. Main bourses in Greece, Italy and Spain finished +1.99%, +1.03% and +0.90% higher on the day, respectively. The European market seemingly breathed a collectively sigh of relief that the manufacturing sector PMIs, although still mired in contractionary territory, have showed some signs of improvement. Indeed the flash Eurozone manufacturing PMI for November came at 46.2 (vs 45.6 expected and 45.4 previous) helped by improvements in France (44.7 vs 43.7 prev) and Germany (46.8 vs 46.0 prev). The services PMIs were softer though which took some shine away. The eurozone services PMI fell 0.3pts on the month to 45.7. This was also accompanied by a 0.5pt and 0.4pt drop in France’s and Germany’s services series, respectively.

Assuming no change in the November and December final readings, our European economists noted that the PMIs would point to a euro area GDP contraction of 0.5% qoq in Q4 which is broadly in line with their forecasts (-0.4% qoq). Staying on PMIs for a bit and turning back to yesterday’s flash HSBC manufacturing PMI in China. DB’s Jun Ma thinks that yesterday’s 50.4 print correlates with an official PMI reading (to be reported on Dec 1st) of around 51 which would be a 0.8pt improvement on the October reading. Also in yesterday’s flash PMI report, the sub-indices of new export orders and output rose by 5.7pts and 3.0pts to 52.4 and 51.3, respectively. Jun believes that the rise in output was driven by raw material inventory restocking which is consistent with the recent rally in commodity prices.

The positive risk tone is extending into the overnight session with Asian bourses mostly higher across the region. Gains are led by the Hang Seng (+0.28%) and Shanghai Composite (+0.73) although volumes and news flow are predictably thin given Japan’s Labor Thanksgiving holidays. Sentiment in Korea was initially weighed by reports that North Korea is preparing to test a long-range ballistic missile. Away from geopolitical headlines, Airline Cathay Pacific overnight described the cargo business as a “huge challenge” and added that cargo revenues are down 13% YTD.

In the FX space, USDJPY is trading 0.3% lower this morning (82.2) and is on track for its biggest downward move in two weeks. This follows a WSJ article which cites Japan’s opposition leader Shinzo Abe as saying that he would be reluctant to intervene in the Yen. In a departure from his strong dovish rhetoric of recent weeks, Abe said that past intervention hasn’t been effective, and monetary policy alone isn’t enough to stop deflation.

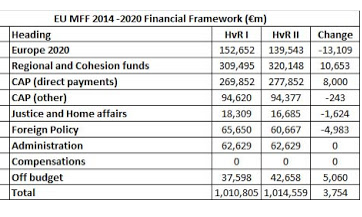

Turing back to Europe, EU President Van Rompuy called an end to the first day of the EU Summit at around 11pm London time last night to allow heads of state some time to study a revised budget proposal that provides for EUR1 Trillion of spending between 2014-2020. The revised proposal allows for EUR80bn in spending cuts which are designed to appease the more hawkish leaders. EU leaders will study the proposals overnight and reconvene at midday today for negotiations. Merkel said that she doubts a budget deal will be reached at this week’s summit and most likely a second summit will be needed early next year.

Moving on to today, there will be very little as far as data flow is concerned. Germany’s IFO survey and Italian retail sales are the two main reports out today. We may get further headlines out of the EU Summit but we should see a relatively quiet end to the week with only a half-day market in the US.

and how does the EU want to spend its budget and what new powers does Brussels seek - looks like they want in on the war mongering game....

http://rt.com/news/eu-parliament-military-resolution-380/

'Direct assault on sovereignty'? EU resolution forces members to beef up security

Published: 23 November, 2012, 08:01

Members of the European Parliament take part in a voting session. (Reuters / Vincent Kessler)

and....

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_23/11/2012_471344

( Stournaras has his thousand yard stare back , excuse any muttering from his mouth at this point. his Junkeritis must be inflamed as he is back to making uncorroborated statements soon to be proven " premature " , " inaccurate " , " misinterpreted " , etc... )

Eurozone teleconference on Saturday to focus on Greece

Initial reports on Friday suggested that the conference call would take place at 5.30 p.m. Greek time on Saturday though subsequent reports said the discussion might be pushed back to the evening. Finance Minister Yannis Stournaras, who will sit join his 16 eurozone peers for the call on Saturday, said late on Thursday that just 10 billion euros are standing in the way of a deal on Greek debt sustainability. He added that eurozone ministers have aleady agreed on measures to reduce Greece's debt to 130 percent of gross domestic product by 2020 and that a gap of between 5 and 6 percent of GDP, or 10 billion euros, remained to be covered. Meanwhile Reuters quoted a ministry source as saying that foreign creditors are considering having the European Central Bank forego 9 billion euros of profits on its Greek debt as part of options to make the country's debt sustainable. The lenders are also mulling cutting the interest rate and extending maturities on loans as well as a 10-billion-euro debt buyback by the government, the source told Reuters. The ministry has already begun preparations for the debt buyback, which could be completed by the end of the year if approved by eurozone finance ministers, the source was quoted as saying. |

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_23/11/2012_471312

Small bondholders demand meeting with gov't officials

Greek small bondholders who suffered losses from the country's debt restructuring in March staged a protest on Friday outside the offices of conservative New Democracy which leads the government's tripartite coalition.

The protesters, who chanted «Thieves, we want our money back,» demanded a meeting with the secretary of the conservative party's political committee, Manolis Kefaloyiannis. Shortly after noon, dozens of protesters entered ND's headquarters.

Bondholders have been insisting that the government offer relief on individual bondholdings up to 100,000 euros, similar to the state guarantee that covers bank deposits.

and....

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_23/11/2012_471293

|

http://www.ekathimerini.com/4dcgi/_w_articles_wsite2_1_22/11/2012_471261

Households see billions of euros of income wiped out

Taxation has increased by 37 pct in 12 months as salaries tank

As a result, households have dramatically curtailed their spending and been forced to resort to dig into their savings, while investment in the country continued to decline over the last 12 months, shrinking by 20 percent year-on-year, second-quarter figures have shown. The disposable income of Greek households amounted to 34.1 billion euros in the April-June period, down from 39.5 billion euros a year earlier. ELSTAT attributes this to the 37.3 percent increase in taxation on incomes and property starting from the second quarter of 2011, along with the 15.1 percent reduction in employees’ salaries and the 9.5 percent drop in social benefits. Consumer spending contracted by 7.3 percent in Q2 compared to the same period in 2011, amounting to 37.1 billion euros, against 40 billion a year earlier. The ELSTAT figures also showed that household savings shrank 8.5 percent, after dropping 1.2 percent in the same quarter a year earlier. Investments declined by 20.6 percent to 3 billion euros, against 3.8 billion in Q2 of 2011. The net borrowing needs of the economy in general amounted to 2.4 billion euros, down from 6.1 billion a year before, thanks to the major reduction in the trade deficit.

and......

Greece and lenders edge towards compromise on debt

Technical experts on the Euro Working Group continued to crunch the numbers in a bid to come up with a strategy for reducing Greek debt that would be acceptable to all members of the eurozone and the International Monetary Fund. Sources said that another 8 to 10 billion euros was needed to meet the target. The IMF has accepted that Greek debt will not meet its target of 120 percent of GDP in 2020 and is willing for this to change to 124 percent in the same year. So far, the technical experts have found ways, including the European Central Bank giving up profits on Greek bonds and Greece embarking on a bond buyback scheme, to reduce debt to 130 percent of GDP by 2020. Greece is also set to save 40 billion euros if its euro partners agree to lower the interest rates on bilateral loans to Athens. “In Greece, we have done our part, now it is our European partners’ and the IMF’s turn to deliver as well,” said Samaras as he headed into a meeting of EU leaders in Brussels that would focus on the 2014-20 Union budget. However, German Finance Minister Wolfgang Schaeuble presented a new potential obstacle to an agreement on Monday when he suggested that Greece could not benefit from a haircut and continue to receive bailout loans as well. “The moment we decide to give Greece a haircut, we cannot give any new guarantees,” he said on Thursday. “That is logical because the budget law rightly says you can only take on guarantees if you believe that the debt will be paid back, so you can’t do both,” he added.

|

No comments:

Post a Comment