http://ransquawk.com/headlines/efsf-might-delay-3y-euro-bond-issue-following-france-downgrade-according-to-leads-20-11-2012

http://ransquawk.com/headlines/moody-s-analyst-says-france-downgrade-will-affect-ratings-of-esm-efsf-20-11-2012

http://www.zerohedge.com/news/2012-11-19/spanish-casa-and-residency-es-su-casa-200000

Submitted by Tyler Durden on 11/19/2012 22:31 -0500

Submitted by Tyler Durden on 11/19/2012 22:31 -0500

http://www.ekathimerini.com/4dcgi/_w_articles_wsite2_1_20/11/2012_470735

European finance ministers will try to plug a 15 billion-euro ($19 billion) hole in Greece’s finances and win over the International Monetary Fund in the latest installment of three years of debt-crisis brinkmanship.

Recycling European Central Bank profits on Greek bonds, charging Greece lower interest rates and extending repayment deadlines are among the options under consideration today for filling the new gap in Greece’s public accounts.

European governments tore open the hole last week, by giving Greece two extra years to cut its budget deficit. The required extra financing provoked a clash with the IMF, since it would add to Greece’s debt load instead of reducing it.

“Greece is in a mess,” James Mirrlees, a Nobel economics laureate, told Bloomberg Television yesterday. Europe won’t solve the problem by “fiddling around with little bits of extra bailout and allowing them to go a bit slower.”

Officials said today’s meeting, starting at 5 p.m. in Brussels, won’t make a final decision to release the next tranche of aid to Greece, partly because parliaments in Germany, the Netherlands and Finland have yet to weigh in.

The “troika” representing creditors also has to certify that Greek Prime Minister Antonis Samaras’s coalition government has delivered economy-boosting steps ranging from improvements to tax collection to the deregulation of closed professions.

The meeting comes a day after France lost its top credit rating with Moody’s Investors Service, increasing pressure on President Francois Hollande to find ways to bolster growth in Europe’s second-largest economy.

and...

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_20/11/2012_470722

http://www.guardian.co.uk/business/2012/nov/20/eurozone-crisis-france-downgraded-greece-eurogroup

French 10-year bond yields in 2012 Photograph: @pawelmorski

French 10-year bond yields in 2012 Photograph: @pawelmorski

French Economy, Finance and Foreign Trade Minister, Pierre Moscovic. Photograph: ERIC FEFERBERG/AFP/Getty Images

French Economy, Finance and Foreign Trade Minister, Pierre Moscovic. Photograph: ERIC FEFERBERG/AFP/Getty Images

http://www.independent.co.uk/news/world/europe/berlusconi-aide-mobsters-held-me-hostage-for-35m-8329587.html

EFSF might delay 3y Euro-bond issue following France downgrade, according to leads

Update details:

- The EFSF was planning to sell new Euro-denominated bonds with a three-year maturity today. Initial price guidance was set in the area of two basis points under the mid-swap rate, a benchmark for bond pricing derived from the cost of swapping fixed and floating-rate interest payments.

11:25 - Fixed Income - Source: Newswires

http://ransquawk.com/headlines/moody-s-analyst-says-france-downgrade-will-affect-ratings-of-esm-efsf-20-11-2012

Moody's analyst says France downgrade will affect ratings of ESM/EFSF

Update details:

- Last night Moody's downgraded France's government bond rating to Aa1 from Aaa and said would downgrade France further if deterioration in economic prospects or there was difficulty in implementing announced reforms.

http://www.zerohedge.com/news/2012-11-19/spanish-casa-and-residency-es-su-casa-200000

A Spanish Casa (And Residency) Es Su Casa For $200,000

- Bad Bank

- China

- European Central Bank

- Greece

- Housing Bubble

- Housing Prices

- Real estate

- Recession

- Reuters

- Unemployment

Unwilling to sacrifice their sovereignty at the altar of the ECB's contingent OMT (and unable to wrench 'help' from their previously colonized friends in Latin America; it seems Rajoy and friends are more than willing to sacrifice their actual land... and citizenship in order to maintain their 'independence'.Reuters reports that Spain is considering offering rich investors from countries such as Russia and China the right to settle in return for them buying up property in the stagnant housing sector. For buying property worth as little as $200,000, wealthy foreigners could be offered a residency permit, the country's commerce secretary said on Monday. This is the same nation with near 11% loan delinquencies,greater-than-50% youth unemployment, and a bad-bank loaded with heavily discounted real-estate assets that are still too expensive to encourage investors, and an ever-present devaluation risk hanging over its paralyzed economy.

We wonder how the other nations of the EU will feel about Spain 'diluting' the citizen-asset pool with this new non-tax-paying, non-labor-utilizing 'wealth'.

And for that matter, not just other mainland-EU countries but New York and London whose real estate markets have risen in the past year in the ultra luxury segment primarily courtesy of BRIC oligarch money.

How long before Greece sells plots on Santorini (w/passport)?

Via Reuters:

(Reuters) - Spain is consideringoffering rich investors from countries such as Russia and China the right to settle in return for them buying up property in the stagnant housing sector.Spain has more than a million empty homes across the country and is setting up a bad bank to clean up toxic assets from a housing bubble which burst in 2008.

Foreigners could be offered a residency permit if they buy a property worth 160,000 euros ($200,000) or more, the country's commerce secretary said on Monday.

"We're looking at markets such as the Russian or Chinese, among which there is already a strong demand for Spanish real estate," Jaime Garcia-Legaz said during a conference.Garcia-Legaz said his ministry was consulting the other departments about the idea andgave no figures about how many foreign individuals might be tempted to buy in Spain in order to get Spanish residency.The government is also trying to drum up interest among foreign investors in participating in its bad bankand will meet with five banks this week, sources told Reuters.

Spain's second largest union, the UGT, criticized the proposal, saying immigration policy should be based on the needs of the labor market.

"It wants to attract foreigners who are obviously rich and able to buy and can supposedly remain in Spain without working with the aim of getting rid of a stock of houses that are largely in the hands of the banks," said the UGT in a statement.Spain's economy has been either in recession or near-paralyzed since 2008 after the decade-long property boom went sour, sending housing prices tumbling more than 30 percent.Real estate prices are expected to fall up to 30 percent more before leveling out, economists say, while there is estimated to be more than a million homes around the country.

Spanish banks' bad loans ratio hit a new high in September, the Bank of Spain said on Monday, with massive unemployment and the economic downturn hitting Spaniards ability to repay their debts.

The other point is that foreigners will simply laugh at this open invitation to invest capital directly knowing that as one after another insolvent country succumbs to the temptations of "wealth redistribution" (there is a reason after all why these uber-rich masters of the universe are seeking to park their capital abroad), that anything that is not airliftable may and will either be nationalized, or simply taxed to death.That and of course, the question of why buy now when they can just wait for one more year and buy at 30% off. Or perhaps Spain hopes that like the ECB, these Chinese and Russian billionaires amassed their wealth by buying high... and holding to maturity.

http://www.ekathimerini.com/4dcgi/_w_articles_wsite2_1_20/11/2012_470735

EU leaders face Greek aid gap in brinkmanship with IMF

|

Recycling European Central Bank profits on Greek bonds, charging Greece lower interest rates and extending repayment deadlines are among the options under consideration today for filling the new gap in Greece’s public accounts.

European governments tore open the hole last week, by giving Greece two extra years to cut its budget deficit. The required extra financing provoked a clash with the IMF, since it would add to Greece’s debt load instead of reducing it.

“Greece is in a mess,” James Mirrlees, a Nobel economics laureate, told Bloomberg Television yesterday. Europe won’t solve the problem by “fiddling around with little bits of extra bailout and allowing them to go a bit slower.”

Officials said today’s meeting, starting at 5 p.m. in Brussels, won’t make a final decision to release the next tranche of aid to Greece, partly because parliaments in Germany, the Netherlands and Finland have yet to weigh in.

The “troika” representing creditors also has to certify that Greek Prime Minister Antonis Samaras’s coalition government has delivered economy-boosting steps ranging from improvements to tax collection to the deregulation of closed professions.

The meeting comes a day after France lost its top credit rating with Moody’s Investors Service, increasing pressure on President Francois Hollande to find ways to bolster growth in Europe’s second-largest economy.

Euro Falls

France was cut to Aa1 from Aaa, the rating company said. The Moody’s downgrade follows one by Standard & Poor’s in January.

The euro slid versus most of its 16 major counterparts after the Moody’s action renewed concern the currency bloc’s debt crisis is deepening. The 17-nation euro dropped 0.2 percent to $1.2783 as of 9:29 a.m. in Tokyo, and lost 0.3 percent to 103.99 yen.

Greek bonds gained for a seventh day yesterday amid expectations that creditors will keep money flowing to the Athens government. The yield on 10-year Greek notes fell 25 basis points to 17.22 percent.

One option is to deliver about 44 billion euros to Greece in December, by bundling 31.5 billion euros on hold since mid- year with two other tranches due before year-end, German Finance Minister Wolfgang Schaeuble said after the ministers failed to finalize the financing last week.

Paris Meeting

Finance officials from Germany, France, Spain and Italy met yesterday in Paris to overcome differences. Spokesmen for the four finance ministries declined to comment on the meeting, which was also attended by European Union Economic and Monetary Commissioner Olli Rehn.

Last week’s decision to grant Greece two extra years, to 2016, to cut its deficit to 2 percent of gross domestic product without offering debt relief stirred tensions with the IMF, provider of about a third of 148.6 billion euros in loans funneled to Greece since 2010.

German Chancellor Angela Merkel, gearing up for a campaign for a third term next year, has ruled out writing off a portion of Greece’s debt. Dutch and Finnish leaders have told their bailout-weary voters the same thing.

IMF Managing Director Christine Lagarde, who began the crisis as French finance minister, sparred publicly with the chairman of the euro meeting, Luxembourg Prime Minister Jean- Claude Juncker, over the European inability or refusal to bring down Greece’s debt burden.

“We clearly have different views,” Lagarde said at a joint briefing with Juncker after the Nov. 12 crisis meeting.

Deadline Extended

The trigger was a decision by the ministers to extend by two years, until 2022, a deadline for paring Greece’s debt to 120 percent of GDP. The debt load is set to peak at 190 percent of GDP in 2014, according to the troika, made up of the IMF, European Central Bank and European Commission.

France was cut to Aa1 from Aaa, the rating company said. The Moody’s downgrade follows one by Standard & Poor’s in January.

The euro slid versus most of its 16 major counterparts after the Moody’s action renewed concern the currency bloc’s debt crisis is deepening. The 17-nation euro dropped 0.2 percent to $1.2783 as of 9:29 a.m. in Tokyo, and lost 0.3 percent to 103.99 yen.

Greek bonds gained for a seventh day yesterday amid expectations that creditors will keep money flowing to the Athens government. The yield on 10-year Greek notes fell 25 basis points to 17.22 percent.

One option is to deliver about 44 billion euros to Greece in December, by bundling 31.5 billion euros on hold since mid- year with two other tranches due before year-end, German Finance Minister Wolfgang Schaeuble said after the ministers failed to finalize the financing last week.

Paris Meeting

Finance officials from Germany, France, Spain and Italy met yesterday in Paris to overcome differences. Spokesmen for the four finance ministries declined to comment on the meeting, which was also attended by European Union Economic and Monetary Commissioner Olli Rehn.

Last week’s decision to grant Greece two extra years, to 2016, to cut its deficit to 2 percent of gross domestic product without offering debt relief stirred tensions with the IMF, provider of about a third of 148.6 billion euros in loans funneled to Greece since 2010.

German Chancellor Angela Merkel, gearing up for a campaign for a third term next year, has ruled out writing off a portion of Greece’s debt. Dutch and Finnish leaders have told their bailout-weary voters the same thing.

IMF Managing Director Christine Lagarde, who began the crisis as French finance minister, sparred publicly with the chairman of the euro meeting, Luxembourg Prime Minister Jean- Claude Juncker, over the European inability or refusal to bring down Greece’s debt burden.

“We clearly have different views,” Lagarde said at a joint briefing with Juncker after the Nov. 12 crisis meeting.

Deadline Extended

The trigger was a decision by the ministers to extend by two years, until 2022, a deadline for paring Greece’s debt to 120 percent of GDP. The debt load is set to peak at 190 percent of GDP in 2014, according to the troika, made up of the IMF, European Central Bank and European Commission.

Lagarde, who cut short a trip to southeast Asia to return to Brussels for today’s talks, declined to say whether the IMF would budge on the debt target. In an interview in Manila, she said the IMF’s credibility is at stake in pursuit of “a solid program for Greece that convinces investors today that it will stand tomorrow.”

Plugging the financing gap through 2014 is easier than demonstrating to the IMF that Greek debt is on a glidepath to “sustainability,” officials said. Greece’s loan rates have been lowered and repayment schedules lengthened twice before, and no one has publicly contested doing so again.

ECB Profits

Finance ministers are also considering how to tap profits made by the ECB and national central banks on Greek bonds, drawing on a February commitment to recycle that money back to Greece. The question of how to treat future ECB profits also has to be addressed.

The central bank is sitting on 208.5 billion euros of bonds of debt-hit governments that it started buying in May 2010 in a controversial program that contributed to the resignation of two Germans from its policy council. While the purchases were halted in March, ECB President Mario Draghi has sketched out a new bond-buying program that would only benefit countries that meet strict conditions.

Asked if unrealized ECB profits on Greek bonds held to maturity could be eventually earmarked for paying off Greek debts, Finnish Finance Minister Jutta Urpilainen said in an interview in Helsinki yesterday: “There are different proposals on the table, of which this is one. We’ll have to see how it looks like as a whole.”

Plugging the financing gap through 2014 is easier than demonstrating to the IMF that Greek debt is on a glidepath to “sustainability,” officials said. Greece’s loan rates have been lowered and repayment schedules lengthened twice before, and no one has publicly contested doing so again.

ECB Profits

Finance ministers are also considering how to tap profits made by the ECB and national central banks on Greek bonds, drawing on a February commitment to recycle that money back to Greece. The question of how to treat future ECB profits also has to be addressed.

The central bank is sitting on 208.5 billion euros of bonds of debt-hit governments that it started buying in May 2010 in a controversial program that contributed to the resignation of two Germans from its policy council. While the purchases were halted in March, ECB President Mario Draghi has sketched out a new bond-buying program that would only benefit countries that meet strict conditions.

Asked if unrealized ECB profits on Greek bonds held to maturity could be eventually earmarked for paying off Greek debts, Finnish Finance Minister Jutta Urpilainen said in an interview in Helsinki yesterday: “There are different proposals on the table, of which this is one. We’ll have to see how it looks like as a whole.”

and...

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_20/11/2012_470722

Finn finmin unsure over Greece decision

|

Finland's finance minister said early on Tuesday she was unsure whether eurozone finance ministers would approve Greece's next loan tranche at a meeting later in the day.

"I'm not at all sure that it will happen. More information is needed before a decision can be made, so the situation is

very much open,» Jutta Urpilainen told reporters after a parliamentary briefing.

Finance ministers had been seen as likely to give tentative approval for the next tranche on Tuesday though the money is

unlikely to be disbursed before December and a deal on debt reduction may require further talks.

Urpilainen repeated that Finland was ready to give Greece more time to reach its financing program targets but said a restructuring of its debt was out of the question.

French downgrade hits EFSF bond sale

Moody's downgrade of France has forced the European Financial Stability Facility (the temporary bailout fund being replaced by the European Stability Fund) to delay a bond sale.

The EFSF had been planning to sell a three-year Aaa/AA+/AAA bond today, but has now halted the plan, Reuters has established.

Legal hitches are to blame -- it appears that the bond can't be described as Aaa/AA+/AAA now that France (one of the bond's guaranters) is only triple-A rated with Fitch.

That's a little embarrassing – and also highlights one of the problems with the eurozone strategy: it's hard for the core to protect the periphery once it has been dragged deeper into the crisis.

For Greece, is 2032 the new 2022?

Sticking with the eurogroup meeting -- there are also reports that the agenda for tonight's meeting has been cut back to simply consider Greece's funding gap to 2014, not to 2016 (even though Athens has been given those two extra years to bring its deficit into line).

That would mean eurozone finance ministers would only need to tackle a smaller funding gap (€15bn not €32bn), making a potential deal easier. However, the IMF might not be satisfied with this piecemeal approach.

Another rumour is that the Troika has considered extending Greece’s repayment terms by another decade, to to 2032.

...by which time many of the participants in this crisis could well be dead.

as Paul Murphy of FT Alphaville points out here (spoiler alert).

Greece: we expect decisions on aid today

Over to Greece where our correspondent Helena Smith says finance ministry officials say they expect “an agreement in principle” to be reached over the release of rescue funds at today’s euro group meeting

Helena writes:

Greek officials say while a full-scale agreement may still be elusive -- with the approval of it next aid tranche unlikely to be finalized -- the debt-stricken country will almost certainly be given a time-frame as to the release of the bumper €44.6bn rescue package.Insiders are confirming reports that the most likely date for the disbursement of the funds is December 5th with the green light finally being given at a euro group meeting already scheduled for December 3rd.“That is going to be the most crucial meeting for final decisions,” said one well-placed source. “At today’s meeting [eurogroup] finance ministers will be briefed by the troika on the commitments the government has made regarding implementation of reforms so an agreement in principle can be reached.”The state-run TV channel NET is also reporting that the “super tranche” will arrive in Athens after the revised bailout accord has been signed between Greece and its creditors at the EU, ECB and IMF on December 4th.Greek finance minister Yiannis Stournaras says he's ready for this afternoon's eurogroup meeting. Photograph: JOHN THYS/AFP/Getty Images

Helena continues:“Today, we are expecting to learn when we will get the money,” one well-placed finance ministry official told me. “Needless to say we want it as soon as possible and also, if at all possible, in one installment.”

Greece’s coalition government has made no secret of the fact that it is hoping a €31.5bn cash injection put on hold since June – mostly because of political paralysis spawned by double elections – will be boosted by two other tranches, amounting to almost €13bn that are also due to be drawn down from bailout funds before the end of the year.Prime minister Antonis Samaras says the extra funds are crucial to re-energising an economy that has shrunk by almost 20 % since the outbreak of the debt crisis in Athens late 2009."We are totally ready for the meeting," says the Greek finance minister Yiannis Stournaras.

Spanish bond auction results

Just in: Spain has held a successful-looking debt auction, raising almost €5bn of debt at lower borrowing costs.

Here are the details:

€4.22bn of 12-month bills sold at an average yield of 2.797%, down from 2.823% in October.

€710m of 28-month bills at an average yield of 3.034%, down from 3.022% in October.

So Spain continues to finance herself - meaning no immediate pressure to seek financial aid.

Belgium's PM: 2013 budget is agreed

Belgium's government has reached a deal on next year's budget, which is likely to contain around €3.7bn of austerity measures.

The country's prime minister, Elio Di Rupo, tweeted this morning that the government has:

an agreement on the 2013 budget and additional measures for competitiveness and employment.

(he tweeted it in French too).

Belgium is aiming to cut its deficit to 2.15% of GDP in 2013, which means a fiscal adjustment of around €3.7bn. Local media have predicted cuts to government spending and social security payments, and tax rises.

Should we care about Moody's?

Moody's downgrade has had virtually no impact on French sovereign debt this morning, with the yield in its 10-year bonds up just a smidgen at 2.09% (as reader IfigEusLannuon has already pointed out in the comments)

Some City experts argue that we shouldn't fret about credit rating agencies at all, with fund manager @pawelmorski providing this graph showing that yields have actually fallen since S&P downgraded France in January:

French 10-year bond yields in 2012 Photograph: @pawelmorski

The downgrade will have some impact, though. For starters, it might affect the credit rating of the European Stability Mechanism (the bailout fund is currently AAA), while pension funds have to consider that France is now officially a riskier bet (as it is now only AAA with Fitch).

Still, as Brasilian points out in the comments below, it's not as bad as losing the 1982 World Cup with Socrates and Zico in your team.

I can't imagine many French throwing their TVs out of the window when they see the news, so it can't be that bad.

Early reaction to Moody's downgrade

Russian economist Constantin Gurdgiev reckons France got off lightly:

Axel Merk, president of Merk Investments in California, told Reuters overnight that the French government had only itself to blame:

France is paying the price for not engaging in reform.

Michael Hewson of CMC Markets said the loss of the triple A rating is "a blow to French prestige", but won't have much impact on its economic outlook – given the wider economic challenges:

Hewson added:

It could however have a trickledown effect down through the French banking system, with potential downgrades for French banks, feeding through into higher borrowing costs, due to the perceived lower credit rating of the sovereign.

Moody's - French growth forecasts too rosy

Another important point in Moody's statement - it reckons that France's predictions of growth of 0.8% in 2013 and 2.0% from 2014 are "overly optimistic"

On top of rising unemployment, France's consumption levels are being weighed down by tax increases, subdued disposable income growth and a correction in the housing market.

That may be unwelcome news to Paris -- but it's worth remembering that the EC predicts growth of just 0.4% in 2013.

French finance minister responds

French Economy, Finance and Foreign Trade Minister, Pierre Moscovic. Photograph: ERIC FEFERBERG/AFP/Getty Images

France's finance minister has defended his government following Moody's downgrade.

Pierre Moscovici insisted that the move did not put the French economy's 'economic fundamentals' into question, saying Hollande's administration was still committed to implementing reforms (such as the €20bn tax boost for businesses announced two weeks ago).

UPDATE: Here's the key quote:

The rating change does not call into question the economic fundamentals of our country, the efforts undertaken by the government or our creditworthiness.

Moscovici added that Moody's was wrong to say that France's banks are vulnerable to a further deepening of the eurozone crisis, because of their exposure to weak members of the currency union.(On that last point – the French financial sector is known to be a big holder of peripheral euro debt. Back in June, France's banks held $40bn of Greek debt, for example, while German lenders' held $5.5bn and U.K. banks owned $5.6bn....)

Why Moody's downgraded France

The full statement from Moody's can be read online, and includes this three-point explanation for downgrading France:

• France's long-term economic growth outlook is negatively affected by multiple structural challenges, including its gradual, sustained loss of competitiveness and the long-standing rigidities of its labour, goods and service markets.

• France's fiscal outlook is uncertain as a result of its deteriorating economic prospects, both in the short term due to subdued domestic and external demand, and in the longer term due to the structural rigidities noted above.

• The predictability of France's resilience to future euro area shocks is diminishing in view of the rising risks to economic growth, fiscal performance and cost of funding. France's exposure to peripheral Europe through its trade linkages and its banking system is disproportionately large, and its contingent obligations to support other euro area members have been increasing. Moreover, unlike other non-euro area sovereigns that carry similarly high ratings, France does not have access to a national central bank for the financing of its debt in the event of a market disruption.

Moody's adds though, that France still has its strengths - including a large, diverse economy and a government committed to reforms (even if it may struggle to implement them).

The big news overnight is that France has lost its Triple-A rating with Moody's.

Late last night the credit rating agency announced that it has downgraded France by one notch to AA1, with a negative outlook. Moody's warned that the French government's fiscal position is worsening as its economy weakens, with significant 'structural challenges' hindering Paris as it tries to implement reforms.

Moody's also shrugged at the government's economic reform plans, pointing out that:

The track record of successive French governments in effecting such measures over the past two decades has been poor.

Although France had already lost its AAA rating with Standard & Poor's in January, Moody's decision is still a blow to Francois Hollande. As our Paris correspondent Kim Willsher writes:

Moody's said it was not confident Hollande's government could – or would – introduce the necessary structural reforms and spending cuts to improved its rating in the medium term and expressed concern over France's exposure to risks from other ailing eurozone countries.

Kim adds that France was already smarting over this week's edition of The Economist:

Its special report warned that the parlous state of the French economy, its rising unemployment, lack of competitiveness, dwindling industry and high public spending, could overshadow the problems of Greece or Spain, and sparked angry reactions from French ministers.

Moody's decision comes as eurozone finance ministers head to Brussels for another meeting on Greece – this could be the day that they decide to advance its long-awaited aid tranche, and agree how to finance the two-year extension to its financial reform programme.

and the UK reminds one of Caltalonia....

http://www.guardian.co.uk/politics/2012/nov/17/eu-referendum-poll

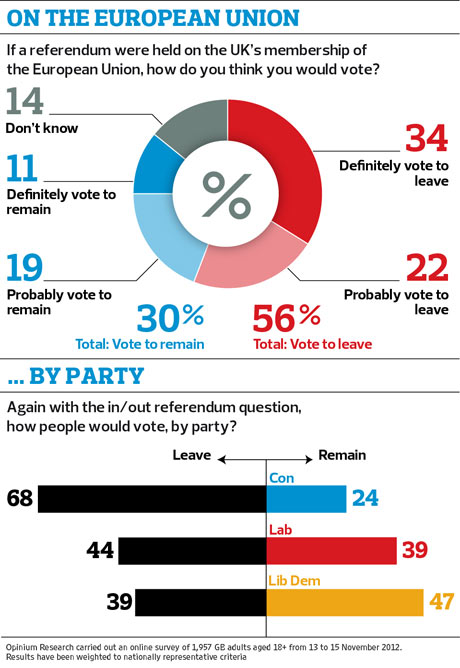

56% of Britons would vote to quit EU in referendum, poll finds

Results of survey will make sobering reading for leaders of three major parties, as PM prepares for crucial meeting on EU budget

NIgel Farage's anti-Brussels Ukip is improving in the polls as voters become increasingly eurosceptic. Photograph: Antonio Olmos for the Observer

Well over half of British voters now want to leave the European Union, according to an opinion poll that shows anti-EU sentiment is sweeping through all three main political parties.

The Opinium/Observer survey finds that 56% of people would probably or definitely vote for the UK to go it alone if they were offered the choice in a referendum. About 68% of Conservative voters want to leave the EU, against 24% who want to remain; 44% of Labour voters would probably choose to get out, against 39% who would back staying in, while some 39% of Liberal Democrats would probably or definitely vote to get out, compared with 47% who would prefer to remain in the EU.

The findings will make sobering reading for all three major parties, which are at risk of losing support to the buoyant anti-EU party Ukip – now two points ahead of the Lib Dems on 10%.

Credit: Observer graphics

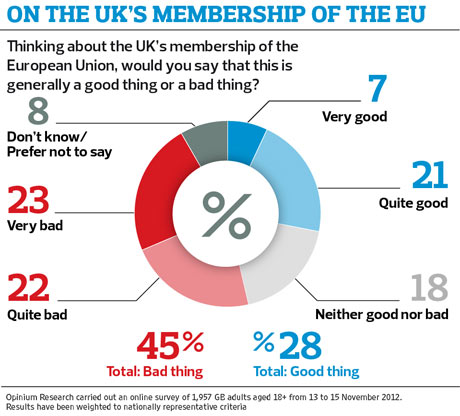

Overall just 28% of likely voters think the EU is a "good thing" while 45% think it is a "bad thing". The 18-34 age group is the only one in which there is a clear majority backing the EU, with 44% saying membership is good, against 25%.

The poll will pile yet more pressure on David Cameron to negotiate a tough deal on the EU budget as he prepares for a Brussels summit, beginning on Thursday, at which EU leaders will attempt to hammer out a financial deal for the union for the seven years from 2014.

The prime minister's problems deepened on Saturday when one of the ringleaders of a recent Commons rebellion on EU financing, the Eurosceptic MP Mark Reckless, predicted an even bigger revolt if Cameron returned from Brussels without having negotiated a real-terms cut in EU spending, or wielded a veto.

Credit: Observer graphics

He added that if Labour, which joined the rebels in calling for an actual cut in the budget, stood firm then Cameron would be defeated. "He is between a rock and a hard place," said Reckless.

Cameron had wanted to go to Brussels arguing for a freeze in EU spending – a negotiating position he believed would attract support from other net contributing nations including Germany and the Netherlands. But having had his hand forced, he is now under pressure to go for an actual reduction – a position that no other EU nation is likely to support.

On Monday Ed Miliband will make a keynote speech to the CBI in which he will argue that every effort should be made to prevent the Tories leading the country towards the EU exit door. He will also say that under the Tories, Britain is "sleepwalking towards exit" from the EU. Labour pro-Europeans accused Cameron of lurching further to the right as it was confirmed Boris Johnson's former election guru, the Australian Lynton Crosby, has become the prime minister's general election strategist.

Credit: Observer graphics

The poll, which showed Labour's lead over the Tories has dropped from 11% two weeks ago to 7% now, with the Lib Dems on 8% and Ukip on 10%, found that voters over 55 were the most critical of the EU, with 59% saying it was a bad thing and 20% a good thing.

and.....

http://www.guardian.co.uk/world/2012/nov/19/david-cameron-eu-picking-pockets?intcmp=239

David Cameron tells EU to stop 'picking pockets' of its citizens

Prime minister to push for budgetary restraint at Brussels talks as Tory divisions exposed over EU membership

David Cameron told the CBI conference: 'I don’t think it makes you a bad European because you want a tough budget settlement in Europe.' Photograph: Rex Features

David Cameron has told the European commission it should stop "picking the pockets" of European citizens as it seeks to push through an above-inflation increase in the EU budget.

As he prepares for a crucial European summit in Brussels on Thursday and Friday, the prime minister said pressing for budgetary restraint in such a difficult economic climate made him a good European.

But Cameron was given a taste of the divisions within the Conservative party when the pro-European Kenneth Clarke confirmed he had sought an assurance from the prime minister that he did not intend to leave the EU.

The former chancellor told the Today programme on BBC Radio 4: "David Cameron assures the public, he has always assured me, that he believes, as I do, that Britain's place in the modern world has got to be in the EU."

Clarke, who warned it would be a "disaster" for Britain to leave the EU, spoke shortly before the former shadow home secretary, David Davis, said that "radical, out-of-Europe options" were becoming more attractive.

Davis said the prospect of British withdrawal should concentrate the minds of EU partners under his plans for two referendums – one to agree a negotiating mandate in which Britain would opt out of key EU laws, and a second to approve a deal negotiated with the rest of the EU.

The prime minister did not dwell in detail on his own plans to repatriate powers from the EU after 2015. In his remarks on the EU during his speech to the CBI annual conference in London, Cameron instead focused on this week's budget negotiations in which Britain will be demanding an inflation freeze.

He said: "I don't think it makes you a bad European because you want a tough budget settlement in Europe. I think it makes you a good European.

"I think I have got the people of Europe on my side in arguing that we should stop picking their pockets and spending more and more money through the EU budget, particularly when so many parts of the European budget are not well spent. One of the interesting things about the proposals so far in this debate about the EU budget is how little attention there has been on the central costs of the EU, the commission budget, what people get paid."

But Davis showed that many Tory MPs, who voted in favour of a below-inflation cut in the budget, have their eyes on an immediate recasting of Britain's relations with the EU as he set out his plans for a double referendum.

The former Europe minister said: "One of my colleagues described this idea to me as a Ukip-killer. That is not the purpose of the strategy, but it will give the Conservative party a proper platform to fight that European election [in 2014]. To make this work we have also to be clear what our position would be if the European Union did not deliver a package that appealed to the British people."

Davis added: "Paradoxically, the fact that the radical, out-of-Europe options are growing more attractive as the years pass, means that the deal that we can strike with Europe is likely to be much stronger. Tony Blair recently called for a "grand bargain" to save the eurozone. But as ever his words were not backed by serious plans. Now is the time for big action, not just big rhetoric."

Clarke believes Davis's plans are unrealistic and designed to provoke a reaction from Britain's EU partners that could see Britain forced out of the EU.

Speaking on the Today programme a few hours before Davis's speech, Clarke said: "It would be a disaster for our influence in global political events, it would be a disaster for the British economy if we were to leave the European Union. It damages our influence in these great critical events at the moment if we keep casting doubt on our continued membership."

In his speech, Miliband warned that the prime minister was in danger of forcing the UK out of the EU by accident. He said: "Many of our traditional allies in Europe clearly think Britain is heading to the exit door. Those of us, like me, who passionately believe that Britain is stronger in the EU cannot be silent in a situation like this. I will not allow our country to sleepwalk towards exit because it would be a betrayal of our national interest."

But the Labour leader said the EU must reform as he acknowledged that Eurosceptics have often been right in their criticisms of the EU. He said pro-Europeans too often "turned a blind eye" to the EU's failings and that Britain needed to build alliances to achieve reform.

No comments:

Post a Comment