http://globaleconomicanalysis.blogspot.com/2012/11/garbage-piles-up-in-spain-as-unpaid.html

Wednesday, November 21, 2012 7:39 PM

Garbage Piles Up in Spain as Unpaid Municipal Bills Mount; Green Shoot of the Day: Cement Consumption Falls 34%

As Spain attempts austerity by cutting back payments to regions, those regions run out of funds to pay bills.

For an interesting case-in-point, please consider (via Google translate from El Economista) Municipalities Owed €2,000 Million, Companies Refuse Collection and Cleaning

For an interesting case-in-point, please consider (via Google translate from El Economista) Municipalities Owed €2,000 Million, Companies Refuse Collection and Cleaning

Defaults on local councils put back on the ropes to urban sanitation companies. No respite worth. If the final plan provider payment partially interrupted the problem, the situation again becomes serious. "Since the beginning of the year delinquencies has skyrocketed. In just eight months to August, the accumulated debt of the sessions with cleaning companies was around 1,680 million.

This rise is worrisome for a sector in Spain employs over 120,000 people, "said the president of Aselip (Association of Public Cleaning), Francisco Jardón.

The result is that today the municipalities pending bills with these companies together account for nearly 2,000 million euros. As also in the pharmaceutical sector, the debt problem is that, far from disappearing, is regenerated by now.That is quite a choppy translation but I believe you get the gist.

"When the government launched the provider payment plan in April the problem was corrected by 90 percent. Then consistories debt with sanitation companies was nearly 3,000 million euros and around 300 million were left payable "adds Jardón. Why? "For the Royal Decree which implemented that plan did not, do not know why, consortia or associations, which also have hired urban sanitation".

Strike in Jerez

Urbaser stars in these days one of the main problems related to the debts. The ERE submitted by the company, which includes 125 layoffs and pay cuts, has meant that employees call for a strike in garbage collection that has lasted 19 days.

According to the City, more than 3,000 tons of garbage piled in the streets of the city of Cadiz, which last night had its second day of riots and burning container. Sources Provincial Fire Consortium reported traffic costs due to the garbage thrown by neighbors to the street as a barricade, and clashes with the police and firefighters who came to put out the flames.

Green Shoot of the Day

While reflecting on garbage, also consider via Google translate The green shoot of the day. Cement consumption falls by 34% through October.

Cement consumption fell by 33.8% in the first ten months of the year, reaching 11.74 million tons, thus scoring one of the biggest percentage declines since the beginning of the crisis.

The association warns that if this fall in consumption is not stopped "using government" not ruled out further adjustments in business capacity of a sector that has already lost one third (33%) of their jobs since the onset of the crisis.

The Spanish cement industry currently employs 5,158 workers in Spain, compared to 7730 it had in 2007, pre-crisis period.

With these settings, the industry is adapting its production volumes to the current demand for cement, affected by the housing slowdown builder and civil works. According to his data, registered until October consumption accounts for less than 40% of the sector's production capacity.

Thus, in the first ten months of the year were made in Spain 13.84 million tons of cement, resulting in a decrease of 28.6%.No Good Economic Outcome Possible

Regarding last October, production fell by 33% compared to the same month in 2011, after consumption fell by 24.7% to 1.14 million tonnes.

There is no possible economic outcome that Europe will be happy with. There is a roughly a 10 percent chance the eurozone does not break up.

Moreover, should the eurozone not break apart, it will mean prolonged economic depression for Spain, Greece, and Portugal, and that depression in turn will hammer Germany and France.

Can-kicking exercises hoping to hold the eurozone intact are a huge part of the problem.

Mike "Mish" Shedlock

and...

Fitch downgrades Cyprus to BB-

Elsewhere in the struggling eurozone, Fitch has just downgraded Cyprus, another country struggling with the prospect of a bailout.

The ratings agency has cut Cyprus from BB+ to BB-, pushing it further into junk territory, with the long term outlook remaining negative. Fitch cited a "materially weaker macroeconomic outlook for Cyprus."

The country is currently trying to negotiate a bailout with the troika, and has even apparently been sounding out Russia for help.

http://www.zerohedge.com/news/2012-11-21/latest-greek-bailout-nutshell-aaa-rated-euro-countries-fund-massive-hedge-fund-profi

The Latest Greek "Bailout" In A Nutshell: AAA-Rated Euro Countries To Fund Massive Hedge Fund Profits

- Bond

- Cramdown

- Creditors

- European Central Bank

- Finland

- Fresh Start

- Fund Flows

- Germany

- Greece

- Gross Domestic Product

- Netherlands

- Real estate

With constantly changing variables in what will be the fourth and not final Greek bailout, it has been relatively difficult to pinpoint just what the "fulcrum security" is in the ongoing restructuring that is not really a cramdown bankruptcy but kinda, sorta is, and more importantly where the money will come from. A big issue that Europe has discovered with a two and a half year delay (pointed out here first, but anyone with capacity for rational thought could have grasped it at the time), is that Greece has hit the inflection point where without more, and substantial, debt forgiveness it is unviable entity, and will certainly not hike the Troika's hard line target of 120% debt/GDP by 2020. In other words, Greece can no longer layer more debt to pay down debt.

The problem is that both Germany and the ECB have decreed they will not agree to Official Sector impairments (recall the private sector was already crammed down with original Greek debt collapsing into New GGBs at about 20 cents on the dollar, which in turn then proceed to trade immediately down to 20 cents of Fresh Start par, implying there is absolutely no value in this most subordinate debt), and as Germany made clear last night, it refuses to permit a largely meaningless cut in interest rates of Greek bilateral loans from 150 bps to a token 25 bps, an adjustment it classified as "illegal."

So what is the latest state of play that has the biggest support from all parties?

It appears that the plan which is now back in play, is one which Greece had previously nixed, namely a partial Greek bond buyback of the private bonds at a discount to par: with numbers currently rumored anywhere between 25 cents and 50 cents on the euro.

On the surface this appears a reasonable deal, however there is a reason why Greece killed this proposal one month ago. As Kathimerini reported back then:

The Finance Ministry is ditching banks’ plan for a bond swap that would have eased their recapitalization requirements.According to sources, Minister Yannis Stournaras has rejected the proposal that local banks presented to him, suggesting that this would be a move that would benefit bank shareholders disproportionately. Ministry sources added that such a move would generate accusations about favorable treatment of banks in comparison with other holders of Greek bonds.

That is also the view by the troika – i.e. the representatives of Greece’s creditors – who had earlier rejected a similar plan.

This is correct: because the only beneficiaries would be those financial players who either bought the bonds in the open market, or held on to the original "pre-petition" bonds.

But even if Greece agrees with this proposal, there is a question of where Greece will get the money for this distressed debt buyback? After all Greece is completely broke, and any new cash would have to be in the form of loans, as not even the most nebulous interpretation of the Maastricht treaty would allow an equity investment, or to use the proper nomenclature, "a fiscal investment" into Greece.

Moments ago, the FT gave us the answer:

An alternative proposal involves offering €10bn of extra loans to Athens from the European Financial Stability Fund, the eurozone’s temporary bailout pot. The option is seen as a leading contender for a compromise deal.This extra lending would support a more ambitious scheme to purchase Greek bonds held by private investors, part of a package of debt relief measures to bring down Athen’s debt to significantly below 120 per cent of economic output by 2022.Sanctioning a new €10bn of bailout loans would pose a considerable political challenge to several countries and require the backing of restless parliaments in Germany, Finland and the Netherlands.

In other words, the money is now supposed to come from the EFSF, funded realistically by Europe's AAA governments, all of which have said not one more penny will go to Greece. However, the EFSF already has prefunded and committed capital so it is a convenient loophole.

The problem will arise when the parliaments of said AAA countries are asked to explain to their people why they all have to pay billions in order to repay between €20 and €40 billion (assuming a 50 or 25 cent repurchase price) of Greek debt, just so Greece has a theoretical chance of hitting 120% debt/GDP by 2020, a number which has virtually no chance of being hit when one accounts for the the denominator: the collapsing Greek GDP which last quarter tumbled at a 7% rate.

But the kicker is when one traces the use of funds. Because what is will happening is a payment not to Greece, obviously, but to its creditors: entities which for the most part are hedge funds, and which have bought up GGB2s in the mid teen levels as recently as 4 months ago (recall Dan Loeb's major position in Greek bonds).

So to simplify the flow of funds:

- Source of Funds: EFSF, using European cash primarily originating at places such as Germany, Finland and Netherlands

- Use of Funds: Hedge funds holders, with a cost basis in the 10-20 cent range.

- Summary: European governments, already struggling with day to day cash procurement and finding new and inventive ways of keeping the ponzi going day to day, will pay... Hedge Funds and their billionaire PMs.

And what do they get in return:

In part to address the inevitable political concerns, officials are

drawing up options to back the new loans with collateral from Greece’s

privatisation programme, which aims to raise €50bn.

So do not fret dear AAA-rated (if not for long) European countries: the money you will spend to generate between 100% and 400% returns for creditor hedge fund in a few brief months, will not be lost - in exchange you will have "collateral" from the Greek privatization program. Which may or may not work: perhaps if Dan Loeb, Elliott and the other creditors who are about to make a huge profit by flipping Greek bonds will "privatize" Greek real estate, and the funds will go back to the European countries who made the payment to the hedge funds a possibility in the first place.

The only real loser here? The Greek people, who will have just sold off up to €50 billion in national assets (and this is uncertain - there may very well not be any buyers for Greek "assets"). The same Greek people who will get not one penny from any of the convoluted fund flows explained above.

And now you know what the current state of the latest Greek bailout process is.

http://www.reuters.com/article/2012/11/21/eurogroup-greece-document-idUSL5E8ML01A20121121?feedType=RSS&feedName=financialsSector

( Eurozone Countries will have to face up to taking losses ( despite lying to their Parliaments that this would never happen ) AND Greece will have to be given additional financing which we be more then the 33 billion discussed presently for the period up to 2016 AND Private Investors will be forced to take another haircut meaning thier losses will be 96 - 97 percent en toto or so . which is why we see no deal announced today. )

Greek debt can only become sustainable by 2022 if all steps taken - document

BRUSSELS |

Nov 21 (Reuters) - Greek debt can fall to below 120 percent of output by 2020 only if euro zone countries accept losses on their loans to Athens, provide additional financing or force private creditors into selling Greek debt at a discount, according to a document prepared for a meeting of finance ministers on Tuesday.

The 15-page document shows that without a package of debt-reducing measures Greek debt will fall to 144 percent of GDP in 2020, 133 percent in 2022 and 111 percent of GDP in 2030, from a current level of around 170 percent.

"The package of options will not make it possible to arrive at a debt-to-GDP ratio of close to 120 percent in 2020 without taking recourse to measures that would entail capital losses or budgetary implications for euro area member states or envisage a more comprehensive DBB entailing the activation of collective action clauses," the document said.

"It may therefore be considered to postpone the benchmark for debt sustainability to 2022 by when Greece's debt-to-GDP ratio can be expected to fall below 120 percent, through the joint application of the ... measures," it said.

The document said a reduction of interest rates on bilateral loans to Greece by 70 basis points from the current 150 basis points above financing costs would cut debt by 1.4 percent by 2020. A much deeper cut to 25 basis points would result in debt falling by 5.1 percent of GDP by 2020.

Deferring interest payments by 10 years to 2022 on loans made through the euro zone's temporary rescue fund would cut Greek debt by 43.8 billion euros, or 16.9 percent of GDP.

If the European Central Bank (ECB) returned the profits it made on its Greek bond portfolio, Greece's debt would be fall by a further 4.6 percent in 2020, the document showed.

Buying back 10 billion euros worth of Greek bonds from private investors at 50 cents per euro would result in debt falling by 2.4 percent of GDP by 2020.

But the combined elements would still fail to reduce the overall debt-to-GDP ratio to 120 percent by 2020, the level the IMF has deemed as "sustainable". If that target cannot be reached, the IMF may withdraw from the Greek bailout programmes.

http://www.ekathimerini.com/4dcgi/_w_articles_wsite1_1_21/11/2012_470908

Eurogroup fails to reach agreement on Greek debt after lengthy talks

|

In a statement issued on Wednesday morning, the Eurogroup acknowledged the steps taken by Greece to meet its program targets but said it would have to debate further what action to take next.

“The Eurogroup noted with satisfaction that all prior actions required ahead of this meeting

have been met in a satisfactory manner,” the ministers said in their statement. “This reflects a wide ranging set of reforms, as well as the budget for 2013 and an ambitious medium term fiscal strategy for 2013-16. These efforts demonstrate the authorities' strong commitment to the adjustment program.

“Against this background, the Eurogroup has had an extensive discussion and made progress in identifying a consistent package of credible initiatives aimed at making a further substantial contribution to the sustainability of Greek government debt. The Eurogroup interrupted its meeting to allow for further technical work on some elements of this package. The Eurogroup will reconvene on Monday, 26 November.”

The delay in reaching a conclusion means that Greece is to be kept waiting for news on the disbursal of up to 44 billion euros in bailout instalments, some of which it was hoping to receive at the beginning of next month as the government is running out of cash to cover its basic needs.

Despite reports of the eurozone failing to bridge its differences with the IMF over how to make Greek debt sustainable and rumors of splits among finance minister, Eurogroup chief Jean-Claude Juncker insisted there were no irreparable differences.

"We are close to an agreement but technical verifications have to be undertaken, financial calculations have to be made and it's really for technical reasons that at this hour of the day it was not possible to do it in a proper way and so we are interrupting the meeting and reconvening next Monday,» Juncker told reporters.

"There are no major political disagreements,» he said.

A document prepared for the meeting and seen by Reuters declared that Greece's debt cannot be cut to 120 percent of GDP by 2020, the level deemed sustainable by the IMF, unless euro zone member states write off a portion of their loans to Greece.

The 15-page document, circulated among ministers, set out in black-and-white how far off-track Greece is in reducing its debt to the IMF-imposed target, from a level of around 170 percent of GDP now.

The document set out various ways Greece's debt could be reduced between now and 2020, but concluded they would not be enough without euro zone creditors taking a hit on their own holdings -- something Germany and others have said would be illegal.

The document did say Greek debt could fall to 120 percent of GDP two years later -- in 2022 -- without having to impose any losses on euro zone member states or forcing through a buy-back of Greek debt from private-sector bondholders.

Without any corrective measures the document said Greek debt would be 144 percent in 2020 and 133 percent in 2022, figures first reported exclusively by Reuters last week.

"To bring the debt ratio down further, one needs to take recourse to measures that would entail capital losses or budgetary implications for euro area member states,» the document says.

"Capital losses do not appear to be politically feasible and would jeopardize, at least in a number of member states, the political and public support for providing financial assistance."

Among the main measures under consideration to bring Greece's debt burden down as rapidly as possible is a debt buy-back under which Greece would offer to purchase bonds from private investors at a discount to their nominal value.

Several options are under consideration, officials have said and the document makes clear, including using about 10 billion euros to buy back bonds at between 30 and 35 cents in the euro.

There are also proposals to reduce the interest rate on loans already extended by euro zone countries to Greece, to impose a moratorium on interest payments and lengthen the maturities on loans, all of which would cut the debt burden.

[Kathimerini English Edition & Reuters]

and....

Chart Of The Day: The Greek Bailouts In Context... Or To Debt Reduction Via Debt Increase

The simple Bloomberg chart below summarizes the running insanity that is the ongoing Greek bailout. To date, the existing bailouts - already completely wasted - amount to well over 100% of Greek GDP.

Keep in mind this is a simplistic, superficial read of the components involved in the three Greek bailouts to date. We show this to present the context for the Fourth Grek bailout which was a failure last night as virtually everyone knows that Greece, in its current iteration, is finished, and that with each passing day the economy collapses ever tighter into a singularity of its own, as nobody works, everyone is on strike, no taxes are collected, yet more government spending is curtailed, and the circle keeps on turning.

All of this is also quite well known to our regular readers. From April:

|

- BARROSO SAYS TOTAL GREEK AID EQUAL TO 177% OF GREEK GDP - BLOOMBERG

This is SECURED debt, or debt which foreigners have funded with a lien on all Greek assets.Including gold! Translated, the Greek Debtor in Possession loan has a 177% Loan to Value.Recall that according to the IMF Greek Debt/GDP will somehow be 120% in 2020. This means that 57% of the incremental debt will somehow have to be paid down. Or, as is 100% more likely, liquidated, with even more super-senior DIP debt. In other words, the Troika itself admitted that the Troika itself will be haircut before all is said and done.

And yet another aspect of the ongoing Greek insanity. As per Bloomberg:

European governments tore open the hole last week, by giving Greece two extra years to cut its budget deficit. The required extra financing provoked a clash with the IMF, since it would add to Greece’s debt load instead of reducing it.

Or, as we predicted the day the first Greek bailout was announced in May 2010, "Greece Bailed Out To Get In Even More Debt."

The absolute idiocy continues.In summary: to debt reduction, via debt increase comrades! Forward!

and......

http://www.guardian.co.uk/business/2012/nov/21/eurozone-crisis-greece-aid-bailout-fail

Greece's Kouvelis adds to Eurogroup criticism

Fotis Kouvelis, the leader of Greece's Democratic Left party (the junior member of the coalition), has joined the ranks of Greeks criticising the eurogroup's performance at yesterday's meeting.

Kouvelis declared that Greece's lenders and fellow eurozone countries should:

immediately live up to their commitments.

adding:

Greece has taken all necessary measures

One should point out that this occurred despite Kouvelis's party abstaining on the parliamentary vote on Greece's austerity plans.

Wolfgang Schäuble is giving more details about Berlin's position on Greece.

In the past few minutes the German finance minister has indicated that a programme to buy back some Greek bonds (thus cutting its total debts) could be worth €10bn. He also told reporters that the Bundestag could vote on the Greek programme on November 30 – four days after the Eurogroup is due to reconvene.

In other words - Greece certainly won't get its aid tranche until December (it was originally due in September!)

Schäuble is also discussing the idea of lowering the interest payments on Greek debt. However, as Reuters' Luke Baker (who endured the overnight talks in Brussels) points out -- he is not embracing the idea of 'Official Sector Involvement' - ie, losses on Greek bonds.

And as Marc Ostwald argued this morning (see 10.06am) without a default, Greece's debts will never be sustainable.

Sherry town’s streets are burning

View of a street covered in litter in Jerez de la Frontera, Cadiz. Photograph: ROMAN RIOS/EPA

View of a street covered in litter in Jerez de la Frontera, Cadiz. Photograph: ROMAN RIOS/EPA

Over in Spain, angry residents have begun burning piles of rubbish in the streets as a long-running row over austerity cutbacks threatens public health.

From Madrid, Martin Roberts explains how a strike by refuse collectors has left around 3,000 tonnes of detritus in the streets.

Angry residents of Jerez de la Frontera, which is world-famous for making sherry wine, have taken to the streets and faced riot police for two nights in a row to burn some of the estimated 3,000 tonnes rubbish which has piled up in the last three weeks since dustbin men went on strike to reject proposals to lay off 30% of them due to spending cuts by the town hall.

Residents have also complained about nasty smells and rats running through the ordure-strewn streets, but officials have denied there is a health risk in the southwestern town.“Rubbish by itself doesn’t lead to illnesses,” Andrés Rabadán, health service chief for the province of Cádiz, told local media. “There may well be a proliferation of rats, but rodents do not enter homes while there is rubbish around. Under normal conditions there are six or seven rats per person, but you don’t see them. They run away.”

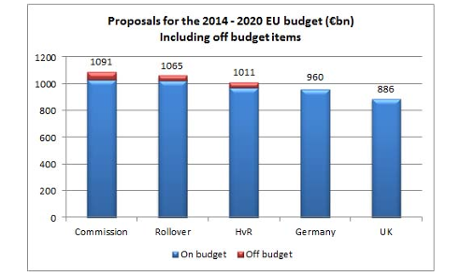

Pressure building over EU Budget

The other looming crisis in Europe is the row over the EU budget, which will really kick off tomorrow when leaders gather for a two-day summit.

UK prime minister David Cameron has already vowed to reject any real terms increase in the budget – but he won't be the only leader playing hardball.

As Open Europe points out, another six countries have explicitly vowed to use their veto if they don't get their way. The Netherlands also wants the budget frozen, while Denmark wants its own veto - and France is unhappy about swathes of the proposals.

This graph shows the divisions between Brussels and the UK (and also Germany).

Photograph: Open Europe

The two-day Summit begins on Thursday evening, but Brussels officials have already said it could run into Saturday if needed.

Why Germany really fears a Greek haircut

Norbert Barthle, a senior member of Angela Merkel's party, gave a clear insight into Berlin's fears over the eurocrisis this morning.

Barthle, the CDU spokesman on budgetary affairs, told Deutschlandfunk radio that fresh debt reduction for Greece would be a terrible example to other struggling members of the eurozone - who would want to copy it!

Barthle said a haircut would be:

a fatal signal to Portugal, to Ireland and possibly to Spain.They would ask themselves straightaway, why should we ... push through tough measures that might lead to the government being voted out if our debts can be written off?"

And that, of course, would mean even higher losses for German taxpayers (as well as commercial lenders).

Economist Intelligence Unit: Still a 40% danger of Grexit

Martin Koehring of the Economist Intelligence Unit has also argued this morning that eurozone leaders need to confront the unpalatable truth that Greece needs further debt relief to stand any chance of cutting its national debt to 120% of GDP by 2020.

Koehring writes:

Euro zone leaders continue to resist accepting a write-down on their loans to Greece, although it looks increasingly likely that this is the only way to reduce Greek debt to the 120% debt target that the IMF deems "sustainable"

He adds that euro zone leaders will probably eventually agree on a deal to cut Greek debt substantially, to avoid Greece leaving the euro zone through mere 'technical disagreements'. But....

A much more likely cause for a Greek disorderly default and euro exit would be domestic political developments in Greece (highlighted by rising political instability and social unrest). However, our assessment remains that there is a 40% probability that Greece leaves the euro zone within the next five years.”

Merkel: Greek aid tranche is no miracle solution

More developments in the political arena – Angela Merkel has told the Bundestag this morning that there is 'a chance' of a deal on Greece next Monday (yup, just a chance), and also warned that the eurozone crisis will rumble on for many more years.

Merkel said:

I believe there are chances, one doesn't know for sure, but there are chances to get a solution on Monday.But the longing for one act, one miracle solution, one truth that means all our problems are gone tomorrow ... this will not be fulfilled.What was neglected over years, over decades, cannot be taken care of overnight and therefore we will need to continue to move step by step.

Merkel was taking part in a debate on the 2013 German budget, after opposition leader Peer Steinbrück called for a delay while the immediate Greek deadlock was solved (see 10.57am).

Tsipras blasts Samaras over latest aid delays

Greece's opposition leader, Alexis Tsipras, has been lambasting prime minister Antonis Samaras in the Athens parliament in the last few minutes.

Tsipras, head of the Syriza party, told MPs that Samaras had failed to fight Greece's corner.

Nick Malkoutzis of Kathimerini was watching the action, and reports:

Peer Steinbrück: Greece in worse shape than Merkel admits

Peer Steinbrück, head of Germany's opposition Social Democrats, has urged Angela Merkel to delay Germany's next budget until the uncertainty over Greece has been resolved.

Steinbrück (who could potentially form a grand coalition with Merkel after next autumn's elections) added that Greece will require assistance until the end of this decade.

He also warned that German taxpayers will ultimately pay the price.

Reuters has the news snaps, and now you do too:

• GERMANY'S STEINBRUECK SAYS CLEAR THAT GREECE WILL NOT BE ABLE TO RETURN TO CAPITAL MARKETS IN THIS DECADE

• GERMANY'S STEINBRUECK SAYS MERKEL'S GOVERNMENT SHOULD PUSH BACK VOTE ON GERMAN BUDGET UNTIL THERE IS CLARITY ON GREECE

• GERMANY'S STEINBRUECK SAYS CANNOT FILL GREEK FINANCING HOLE WITH MIX OF PIECEMEAL MEASURES

Marc Ostwald: Greece must default

Analyst Marc Ostwald of Monument Securities is on blunt form this morning, aghast at the eurogroup's failure to grasp the situation in Greece.

Ostwald says:

Once again one is stunned by the inability of all involved parties to face some key facts:a) Greece's problems are not related in any shape or form to its debt servicing costs, so any measures on this front are a case of 'fiddling while Athens burns';b) Greece's problems are about its debt mountain, which is de facto not sustainable without a huge write-off that will have to include all Official Sector holdings and, preferably reduce the CURRENT outstanding debt to GDP ratio to 60% or at worst 80% - there are no other solutions other than outright default.This will not change today, on the November 26th or any other date, though the longer the various parties involved fail to face up to this reality, the higher the probability of a very disorderly default.

Merkel: deal still possible

Back to the Greek deadlock, and Angela Merkel has been attempting to reassure German MPs in a closed-door meeting.

Dow Jones Newswires has a source on the inside, who reports that Merkel told lawmakers that a deal on a Greek debt buy-back and cuts to the interest rates on its loans was still possible.

She also, apparently, said Germany could be willing to help boost the capital held by the European Financial Stability Facility by €10bn – to help fund a Greek bond-buyback.

Greece postpones fund-raising trip to Qatar

Antonis Samaras has now postponed a trip to Qatar, scheduled for next Monday, because the Eurogroup will be holding another meeting on Greece on that day.

Spokesman Simos Kedikoglou told Reuters that:

The prime minister will stay in Athens to coordinate things.

The irony here is that Samaras had been planning to drum up investment from the Qataris, which could have helped the country return to growth (and meet the privatisation targets imposed by the Troika).

In Athens, bank shares slide

Greek bank shares have fallen sharply in early trading, following the disappointment of the eurogroup meeting.

Athens journalist Efthimia Efthimiou has the details:

Schäuble: no deal on debt target or funding black hole

German finance minister Wolfgang Schäuble has raced back from the eurogroup meeting to speak to German MPs at the Bundestag.

He's explaining the situation with Greece, and making it clear that there is still no consensus on two key issues.

According to Schäuble, eurogroup finance ministers and the IMF could not agree how to fill the €14bn shortfall in Athens' finances over the next two years. There was also disagreement on whether Greece had to achieve debt sustainability by 2020 or 2022.

Greek PM: No justification for Eurogroup failure

Greek prime minister Antonis Samaras has blasted eurozone finance ministers for failing to agree a deal on the country's bailout at last night's talks.

In the face of public disappointment and criticism from opposition MPs (see 7.20am), Samaras there was no justification for the latest delay.

In a punchy statement, Samaras said:

Greece did what it had committed it would do . Our partners, together with the IMF, also have to do what they have taken on to do.Any technical difficulties in finding a technical solution do not justify any negligence or delays.

(quotes via Reuters)

Samaras must hope that the Greek public blame the eurogroup for the deadlock, rather than him.

And the early reaction from Greece suggests that's how the citizens are reacting:

Why the talks failed

While finance ministers were arguing last night, Reuters got their hands on a document prepared for the meeting.

It showed that Greece's debts can only be cut to a sustainable level if eurozone countries accept losses on their loans to Athens, provide additional financing or force private creditors into selling Greek debt at a discount.

The document outlined that other measures (such as cutting the interest rates on Greece's loans or buying debt from private investors) would not have enough impact on the country's debt pile.

It said that either member states accept "capital losses or budgetary implications", or push back the target date for Greece's debts to fall to 120% of GDP by two years, to 2022.

Eurozone countries are not, yet, prepared to accept the first option, while the second option is unacceptable to the IMF. Thus deadlock.

Greek MP: We are being humiliated

A Greek opposition MP has hit out at the humiliation being heaped on the Athens government, following the Eurogroup's failure to agree a deal overnight.

Dimitris Papadimoulis of the left-wing Syriza party declared:

A new postponement. On Monday, they will a band aid until the German elections.The government is doing all their favors and is being humiliated in return.

That's via Kathimerini, the Greek newspaper. It's deputy editor, Nick Malkoutzis, also questions whether Athens should change course.

Schäuble: Greek questions are so complicated

Germany's finance minister Wolfgang Schäuble also spoke to the press after the eurogroup meeting, saying:

the questions are so complicated we didn't find a conclusive solution.

No comments:

Post a Comment