http://www.zerohedge.com/news/not-so-fast-finland-and-holland-will-block-esm-bond-buying

Submitted by Tyler Durden on 07/02/2012 06:45 -0400

Submitted by Tyler Durden on 07/02/2012 06:45 -0400

How many beans will Motormouth spill?

How many beans will Motormouth spill?

http://www.guardian.co.uk/business/2012/jul/02/eurozone-crisis-optimism-eu-summit

Not So Fast: Finland And Holland Will Block ESM Bond Buying

While the bailout ball is in the German constitutional court, which has 8 days to decide, and potentially put the entire timeline of Europe's bailout in limbo should it cogitate longer than July 9 without handing over the ESM law to the president, in effect forcing the country into a Euro bailout referendum, it is easy to forget that there are other AAA-rated countries in Europe, which also have a say as to who gets bailed out. As of this morning, it appears that Germany may increasingly be the only one left footing the insolvency bill as both Finland and Holland said "Ei" and "Nee" respectively.

From Reuters:

and following LIE-Bor lies and scandals.......Finland and the Netherlands will block the euro zone's permanent bailout fund from buying bonds in secondary markets, the Finnish government said on Monday, despite European leaders' decision last week that rescue funds be available to stabilise markets.Euro zone leaders agreed at the summit on steps to shore up their monetary union and bring down borrowing costs for Spain and Italy, but they had given few details on the use of the temporary EFSF and permanent ESM rescue funds.

ESM bond buying from secondary markets would require unanimity and that seems unlikely because Finland and the Netherlands are against it, the Finnish government said a report to a parliamentary committee.And more, also from Reuters:Finland will block the euro zone's permanent bailout fund from buying government bonds in the open market, the Finnish government said on Monday, while The Netherlands also indicated opposition to the bond-buying idea.Comments suggesting a rough time ahead for the idea followed euro zone leaders' agreement at a summit last week to take steps to shore up their monetary union and bring down Spanish and Italian borrowing costs.

They gave few details on how they might use the temporary EFSF and permanent ESM rescue funds to buy bonds.A Dutch finance ministry spokesman said on Monday his government did not like the bond-buying idea but did not explicitly say the Netherlands would block the plan, saying only that it would evaluate purchases on a case-by-case basis."The prime minister said on Friday he is not in favour of buying up bonds," said Niels Redeker, spokesman for the Dutch finance ministry. "Using the existing instruments to buy up bonds will be expensive and can only be done if there is unanimity (between member states). That means the Netherlands would need to vote in favour."

On the insistence of Spain and Italy, now in the eye of the euro debt storm, euro zone leaders decided last week to soften slightly the terms on which countries that observe EU rules and recommendations can get euro zone help to lower market premiums.So while Germany is indeed left all alone to preserve the European dream, we wonder: just what is the reason to keep calling Europe a "Union" when this is rapidly becoming the biggest misnomer of all time?

http://hat4uk.wordpress.com/2012/07/02/libor-bbcs-peston-confirms-slog-central-bank-prediction/

LIBOR: BBC’s Peston confirms Slog central bank prediction

DIAMOND’S SELECT COMMITTEE TESTIMONY TO BE CRUCIAL

How many beans will Motormouth spill?

How many beans will Motormouth spill?Slog’s investment bank contacts call LIBOR ‘a joke’

Last Thursday, The Slog asserted as follows in relation to the LIBOR scam, under the sub-head ‘Is Bob Diamond being forced to apologise for something hatched way above his level?’:

‘…..much as I would love to lump every last kilo of smelly silage on the Diamond Geezer for this, it looks like even he was, on this occasion, merely a cog in a much bigger wheel. By time 2011 got under way, the LIBOR manipulation scam was being investigated by every major bourse regulatory body on the planet. And it may well be that the Treasury was willingly providing Barcap with the data it craved as a means of survival…..In short, must have been a concerted effort involving several central banks.‘

Yesterday at around 11.55 am (the ultimate dead period for website visits – Sunday lunchtime) Robert Peston wrote this on the BBCNews site:

‘In making false submissions about their borrowing costs, managers at Barclays believed they were operating under an instruction from Paul Tucker, deputy governor of the Bank of England, I have learned. This belief was fostered after a telephone conversation in the autumn of 2008 between Mr Tucker and Bob Diamond, who at the time ran Barclays’ investment bank, Barclays Capital, and is today chief executive of Barclays.

Mr Tucker did not issue this instruction. But he and Mr Diamond have different recollections of their conversation. So what Mr Diamond recalls about this telephone conversation may turn out to be the most explosive and important part of his testimony to MPs on the Treasury Select Committee, which will take place on Wednesday.when providing data to the committees that set the Libor rate. [While] Barclays managers were very worried that the appearance of the bank paying more to borrow than other banks was damaging confidence in its health….a central question is why Barclays’ managers came to believe, after the conversation between Mr Diamond and Mr Tucker, that the Bank of England had sanctioned them to lie about what they were paying to borrow.

But this is the key observation: (my emphasis)

‘So Barclays so-called “submitters”, the managers who gave borrowing data to the British Bankers Association’s Libor-setting committees, consistently told these committees that Barclays was paying a lower interest rate to borrow than was actually the case….what is striking is that even the artificially suppressed quotes for Barclays’ borrowing costs provided to the BBA committee were higher than other banks’ quotes….’

Or put more succinctly, they were all at it. And this is an observation confirmed by Slog sources in the investment banking sector. For obvious reasons, the following informant email descriptions have to remain anonymous:

“The idea that LIBOR as generated by banks reporting estimate rates on a ‘best guess’ basis to the BBA, has been a standing joke in the industry since about mid-2007. As the, now old, joke runs, “LIBOR is the rate at which banks used to pretend they’d lend to each other”. I remember working on transactions in 2008 where some of the smaller UK banks or building societies would borrow on a SECURED basis at rates of around LIBOR+2% or 3%, which is obviously absurd if LIBOR is the rate that banks are supposed to lend to each other on an unsecured basis.”

Quite so. Also this startling assertion: (Again, my emphasis)

“After mid/late 2007, banks largely stopped really lending to each other on an unsecured basis. In the terminology of the industry, the ‘interbank market froze up’. It remains largely frozen across Europe to this day. In this context the banks and the BBA had a challenge on how to report LIBOR. To admit that this freeze up had happened would risk a credibility crisis, bank runs, etc. as the media caught on the the scale of the crisis which, at this point, everyone was trying to ignore. So the banks and the BBA chose (or were told, maybe) to keep reporting LIBOR as if everything was alright, business as usual, even though it was essentially un-anchored from the real world.”

I refer you back to my opinion of last week:

“….the British Bankers’ Association (BBA) denied any [manipulation], stating that the BBA ‘observes rigorous standards in our scrutiny and governance of the Libor mechanism, and works with the industry to ensure their continued full confidence in one of its most accurate and reliable benchmarks.’ But in the four years since, the world at large has grown up bigtime about this kind of denial bollocks…”

Indeed. Or again put another way, the BBA release was a catalogue of lies from start to finish.

My conviction remains the same as it was from the outset: key politicians must have known what was going on – as indeed one assumes did large and somewhatclose to the wind donors to the Tory Party – and Labour Prime Ministers trying to get re-elected despite never once hand on heart ever considering the idea of having an election.

But for the time being, while aptly named Barclays Chairman Marcus Agius prepares to fall on his praetorian sword, hard-as-Diamond Black Bob stays in his job….and may be about to blow the lid completely off this Teapot Dome when he faces the Select Committee this week.

Stay tuned: as I predicted last week, this is a developing and potentially explosive story.

http://www.guardian.co.uk/business/2012/jul/02/eurozone-crisis-optimism-eu-summit

Finland is sticking to its hardline position that Eurozone bailout funds should not be used to buy government bonds. It's not clear, though, that it can block the idea.

The Finnish government told a parliamentary committee this morning that it, and the Netherlands, would both block the European Stability Mechanism (ESM) from buying sovereign debt in the secondary bond market (to, for example, drive down the bond yields of Spain or Italy).

At the EU Summit last Friday, German chancellor Angela Merkel has indicated that leaders had agreed "precise conditions" under which bonds could be bought. This was reported as one of the Summit breakthroughs.

So has Finland just derailed the plan? Not necessarily. Any decision to start a bond-buying programme ought to be taken unanimously, but in an 'emergency situation', it could be agreed with 85% shareholder support (based on the contributions made by each country). Finland and the Netherlands don't have the muscle to block it (as the WSJ's Charles Forelle explains):

As feared, eurozone unemployment has hit a new record high, and the youth jobless crisis has worsened again.

The unemployment rate across the single currency region rose to 11.1% in May, up from 11.0% in April. That's the highest figure since the creation of the euro.

The rate across the wider Europan Union also rose, to 10.3% in May from 10.2% in April.

The rate across the wider Europan Union also rose, to 10.3% in May from 10.2% in April.

Youth unemployment also rose again, with another 282,000 young people (under 25) out of work across the EU compared with a year ago, including 254,000 within the eurozone. That pushed the youth unemployment figure up to 22.6% in the eurozone and 22.7% across the EU.

There are now 5.517 million young persons unemployed in the European Union, of whom 3.412 million were in the euro area.

Once again, the youth jobless data showed the deep divergences between the countries which make up the eurozone. Germany can boast the lowest youth jobless rate at just 7.9%, followed by Austria at 8.3% and the Netherlands with 9.2%.

The situation is bleakest in Spain and Greece, with 52.1% each (although Greece's data is from March).

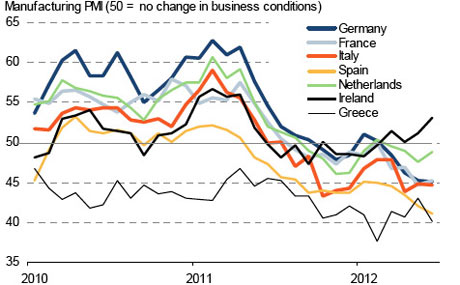

This graph from Markit shows how manufacturing output across the eurozone has been steadily sliding since early 2011, culminating in the three-year low recorded this morning (see 9.12am).

While Greece remains the weakest performer by far, other peripheral countries have been sliding towards it in recent months....

Update: here are the details of the eurozone PMIs:

Ireland: 53.1 14-month high

Austria: 50.1 6-month low

Netherlands: 48.9 2-month high

France: 45.2 2-month high

Germany: 45.0 36-month low

Italy: 44.6 2-month low

Spain: 41.1 37-month low

Greece: 40.1 4-month low

Austria: 50.1 6-month low

Netherlands: 48.9 2-month high

France: 45.2 2-month high

Germany: 45.0 36-month low

Italy: 44.6 2-month low

Spain: 41.1 37-month low

Greece: 40.1 4-month low

The youth employment crisis in Italy has deepened.

Data just released showed that the Italian youth unemployment rate rose to 36.2% in May, which is its highest level since 1992.

The overall Italian jobless rate dropped back slightly though, to 10.1% (from 10.2% in April).

Spain's manufacturing sector has suffered its worst month since May 2009.

June's Spanish PMI came in at just 41.1 for June, showing that output fell sharply, and at a faster rate than May (when the PMI was 42, also well below the 50-point mark that shows whether the sector expanded or contracted).

Economists had expected a weak figure, but this is even worse than they forecast. It underlines the steady deterioration in Spain's economy, which is already in recession. Interesting early developments in Athens, where Jörg Asmussen, executive board member of the European Central Bank, has urged Greece to stick with its economic programme.

Speaking at a conference organised by The Economist, Asmussen warned that the upheaval caused by the second Greek election means the country is now behind schedule, and Antonis Samaras's government must now fix this urgently.

Asmussen said that implementation has "virtually stalled" since the second bailout was agreed three months ago, adding:

The first priority for the new Greek government has to be getting the programme back on track.

There is strong pressure in Greece for the terms of its bailout plan to be eased, but Asmussen argued that this would be "risky", as any changes would mean Greece would miss its target of cutting its national debt to 'just' 120% of GDP by 2020.

The speech comes at (another) important time for Greece, with its Troika of lenders arriving tomorrow to start discussions on its reform plans. Samaras himself is expected to resume work today after the recent eye operation that prevented him attending last week's summit.

No comments:

Post a Comment